For every stock, there are always two sides of investment argument. For Herbalife, I am sure readers will be familiar with both bullish and bearish side of the story. So, I won’t rehash them again here. Instead, I will directly address why Ackman’s key argument is flawed.

Distributing rewards > Retail profit does not imply organization is a pyramid scheme

Ackman’s key argument is “if participants make more money from recruiting rewards rather than retail sales, the organization is deemed to be a pyramid scheme”. He devoted the first half of his 334 slide presentation just to prove that Herbalife’s distributors make more money from recruiting rewards rather than retail sales. More recently in Harbors Conference, he said that an organization in which participants makes more money by recruiting other distributors as compared to retail sales is deemed to collapse as eventually the organization would run out of interested distributors.

In this article, I will be showing why this argument is flawed with the help of an example.

Consider an MLM Company which produces and sells product X through its distributors. The average cost of production of X is $15. The company sells this product at $30 to distributors who in turn sell this product at $35 to Retail clients. For simplicity, let us assume 100% of sales are outside the network and there is zero self-consumption among distributors. Also, for this example let’s assume recruiting rewards are limited only to the one level directly hired by the participant. (You may of course assume multiple levels of recruiting or upline rewards, but that would unnecessarily complicate things. Hence, I am avoiding it to keep things simple in this illustration).

Here are the incentives for distributors:

1). $5 profits for retail sales

2). $10 reward for hiring a new distributors

Other important conditions:

1). Zero self-consumption

2). Zero upfront cost for participation

3). At least 1 sale to be classified as distributor

4). No commission on sales made by down line distributors (for simplicity)

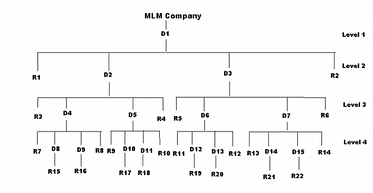

Suppose the MLM organization develops in a symmetric way where each distributor does two retail sales and hires two new distributors, until the final level “n” when the organization runs out of prospective distributors. In final level, since there are no willing new hires for distributors, existing distributors will do just a single retail sale each to qualify as distributor and will not hire anyone. The following diagram illustrates this MLM scheme when there are just four levels of distributors. (Please note that I have to assume organization develops in a symmetrical way to avoid unnecessary complication in developing model. In reality, it may be a different, more complicated structure but the outcome will be the same.)

Let’s see how much do the participants in above scheme earn from retail sales and recruiting rewards if the scheme goes up to four levels.