II. Gold and Bitcoin (Millennial Gold)

The other asset class that always attracts attention and money during crisis is gold, and for good measure, I will also look at Bitcoin, which some have suggested is the millennial equivalent of gold:

It is perhaps a little unfair to draw a conclusion from just contest, but the fact that Bitcoin has behaved more like stocks than like gold suggests that millennials who have held on to it, as their asset of refuge, may want to rethink their positions.

3. Oil and Commodities

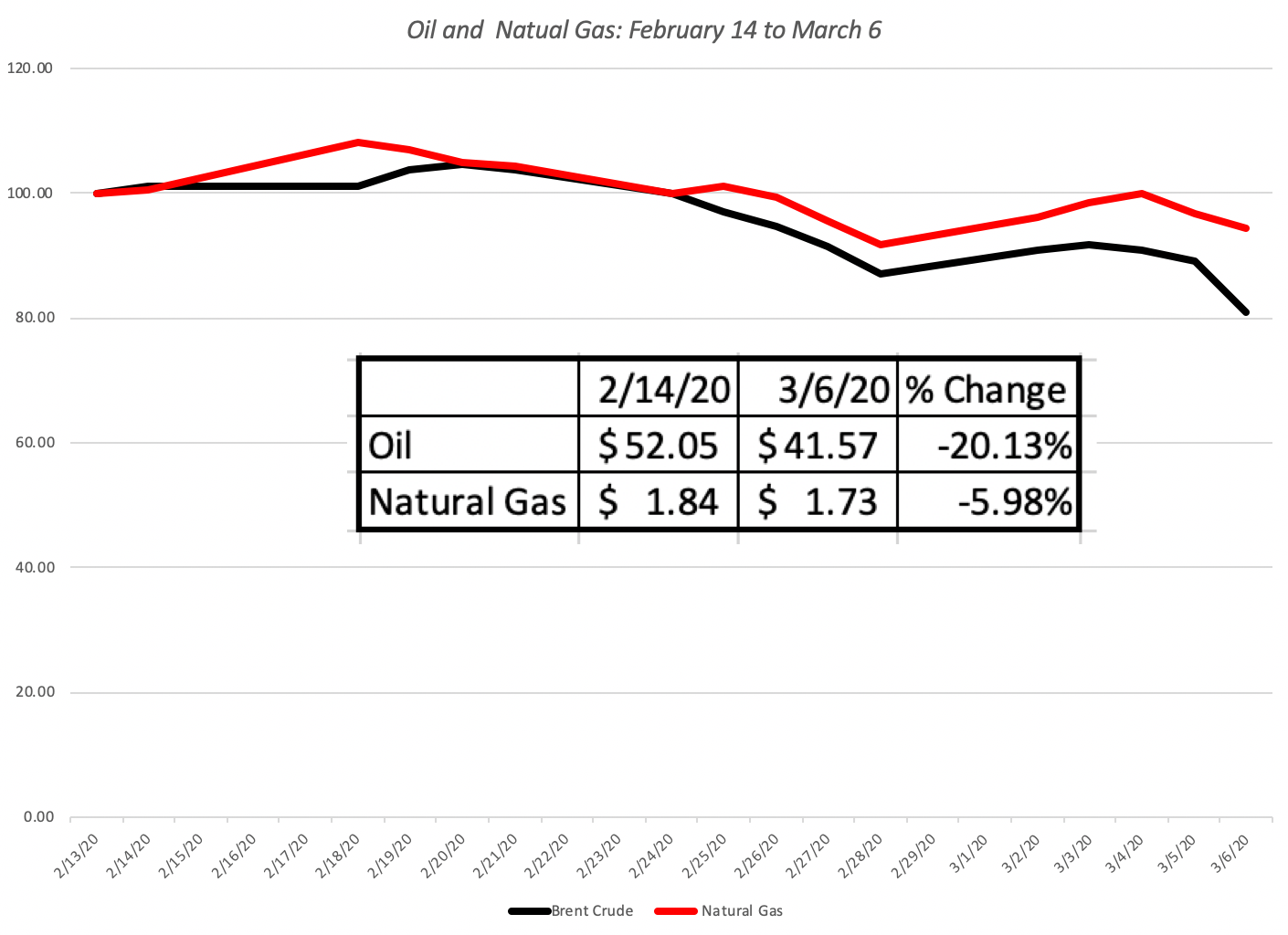

The final piece of the market puzzle comes from the commodity markets, with oil as its front runner. In the three weeks which have taken equity markets on a ride and caused US treasuries to hit new lows, oil prices have been on a journey of their own:

Not only have oil prices dropped 20% during the three weeks, they are plumbing depths seldom seen in this century. The decline in oil prices not only reflect an expectation of global economic slowdown but also how dependent oil and other commodity prices have become on China’s continued growth and prosperity. The smaller decline in natural gas prices, much less tied to the Chinese market, reinforces this argument.

Revisiting the Viral Value

With this long lead in, you might have lost interest already, but if you are still reading, it is time to turn to specifics and look at how what I have learned in the last 12 days has or has not changed my views on the market.

Recapping the Drivers

Very quickly recapping what I argued were the drivers of the value of stocks, I argued that there were three components to value:

- Earnings Growth: In my 2/26/20 valuation of the S&P 500 index, I argued that the corona virus is now almost certain to cause earnings effects for companies, and estimated the drop to be 5% (a significant revision down from the 5.52% growth that had been predicted in the index. In the last few days, analysts have started adjusting earnings expectations down for companies, and this snapshot from Zacks today captures some of the adjustment:

Note that the expected earnings on the index for 2021 has dropped from 172 for next year, two weeks ago, to 163 this week, matching the earnings generated in 2019. That is still better than the 5% drop that I was projecting, but my guess is that I am still undershooting the actual earnings decline and I have increased the expected earnings drop in 2020 to 10%. To complete the assessment of growth, I also need to estimate how much of the earnings drop in 2020 will be recouped in future years. In my valuation on February 26, I had estimated that half of the earnings drop in 2020 would be recouped but that the rest would be lost for the long term. I will continue to hold on to that assumption In addition, since my long term growth rate converges on the US T.Bond rate, the precipitous drop in that rate has lowered my growth rate in perpetuity to 0.74% (to match the T. Bond rate).

Note that the expected earnings on the index for 2021 has dropped from 172 for next year, two weeks ago, to 163 this week, matching the earnings generated in 2019. That is still better than the 5% drop that I was projecting, but my guess is that I am still undershooting the actual earnings decline and I have increased the expected earnings drop in 2020 to 10%. To complete the assessment of growth, I also need to estimate how much of the earnings drop in 2020 will be recouped in future years. In my valuation on February 26, I had estimated that half of the earnings drop in 2020 would be recouped but that the rest would be lost for the long term. I will continue to hold on to that assumption In addition, since my long term growth rate converges on the US T.Bond rate, the precipitous drop in that rate has lowered my growth rate in perpetuity to 0.74% (to match the T. Bond rate). - Cash flow Payout: The second component of value is the cash that companies can return, in dividends and buybacks. I assumed that companies, driven by uncertainty, would scale the percent of the earnings that they return to stockholders from the 92.33% that they were returning prior to the crisis to 85%, more in line with the ten-year average. In the days since, there have been no announcements of dividend cuts or scaling back of already announced buybacks, but I would not be surprised to see that change in the next few weeks.

- Discount Rate Dynamics: The discount rate dynamics are the trickiest. On the one hand, the lower T.Bond rate will create a lower base from which to build up, but the increase in volatility (actual and expected, as captured in the rise in the VIX over the last three weeks) has pushed equity risk premiums up. I will scale up my ERP to 5.69% to match my implied premium at the start of March 2020.

With that combination of assumptions (10% drop in earnings, 50% recoupment between 2022-25, 85% cash return and a 5.69% premium), the value that I derive fo the index Is 2889, and much of the reason for the drop from the value that I estimated on February 26, 2020, can be attributed to the the lower growth rate that I am estimating in the near term and in the long term.