How cheap is it?

First, just how low is the market valuing Apple Inc. (NASDAQ:AAPL)? It’s pretty incredible.

During the last twelve months Apple generated $44 billion in free cash flow. Assuming that remains constant, you could buy the entire business today for $400 billion, pocket the $150 billion in cash on its balance sheet ,and own the company free and clear within six years (I’m excluding obvious tax issues for simplicity)!

Apple Inc. (NASDAQ:AAPL) is even cheaper on conventional metrics. Today, the stock trades at 10 times trailing earnings. Excluding cash, the company is valued at around 7 times last year’s income.

Apple also looks spectacularly inexpensive against its peers. The market is willing to pay 20 times for Google Inc (NASDAQ:GOOG)‘s trailing profits. Even boring old Microsoft Corporation (NASDAQ:MSFT) trades at over 18 times last year’s earnings.

What’s going on? Clearly the market doesn’t think the E in Apple Inc. (NASDAQ:AAPL)’s P/E is sustainable.

Is that rational?

In order for Apple’s valuation to make any sense, the market must be assuming Apple Inc. (NASDAQ:AAPL) will enter a period of steadily declining profitability. That’s actually a reasonable assumption.

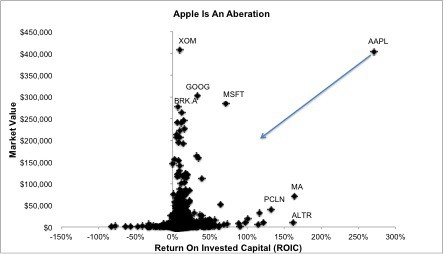

First, consider how outstandingly profitable Apple has been in the past. Equity research firm New Constructs illustrates this well in a chart comparing Apple Inc. (NASDAQ:AAPL)’s return on invested capital and market value versus all of the other publicly traded companies in the United States. Apple is so profitable that it stands out like Richard Nixon at Woodstock.

But this isn’t a good thing. Fat margins attract competitors who want to get a piece of the action and this will inevitably lead to declining profitability for Apple Inc. (NASDAQ:AAPL). Already, the top-end of the smartphone market is looking saturated with Samsung, HTC, Nokia Corporation (ADR) (NYSE:NOK), and Research In Motion Ltd (NASDAQ:BBRY) all trying to get into (or back into) the game.

Of course, businesses can continue to earn excess returns if they have a sustainable competitive advantage. But Apple bulls should rationally reconsider just how strong the company’s moat is. Today, the difference in quality between hardware manufacturers is becoming slimmer by the day, so is the premium Apple Inc. (NASDAQ:AAPL) can charge for its product.

Now I’m not saying Apply doesn’t have some brand strength. As an example, the company’s app ecosystem has proven difficult for rivals (Google excluded) to replicate. But ask yourself this: In every business in which Apple currently competes, will the company’s margins be higher or lower five to ten years in the future? The entire history of the technology industry says lower.

{kind=link}