How cheap is it?

First, just how low is the market valuing Apple Inc. (NASDAQ:AAPL)? It’s pretty incredible.

During the last twelve months Apple generated $44 billion in free cash flow. Assuming that remains constant, you could buy the entire business today for $400 billion, pocket the $150 billion in cash on its balance sheet ,and own the company free and clear within six years (I’m excluding obvious tax issues for simplicity)!

Apple Inc. (NASDAQ:AAPL) is even cheaper on conventional metrics. Today, the stock trades at 10 times trailing earnings. Excluding cash, the company is valued at around 7 times last year’s income.

Apple also looks spectacularly inexpensive against its peers. The market is willing to pay 20 times for Google Inc (NASDAQ:GOOG)‘s trailing profits. Even boring old Microsoft Corporation (NASDAQ:MSFT) trades at over 18 times last year’s earnings.

What’s going on? Clearly the market doesn’t think the E in Apple Inc. (NASDAQ:AAPL)’s P/E is sustainable.

Is that rational?

In order for Apple’s valuation to make any sense, the market must be assuming Apple Inc. (NASDAQ:AAPL) will enter a period of steadily declining profitability. That’s actually a reasonable assumption.

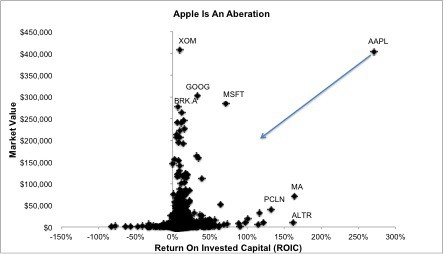

First, consider how outstandingly profitable Apple has been in the past. Equity research firm New Constructs illustrates this well in a chart comparing Apple Inc. (NASDAQ:AAPL)’s return on invested capital and market value versus all of the other publicly traded companies in the United States. Apple is so profitable that it stands out like Richard Nixon at Woodstock.

But this isn’t a good thing. Fat margins attract competitors who want to get a piece of the action and this will inevitably lead to declining profitability for Apple Inc. (NASDAQ:AAPL). Already, the top-end of the smartphone market is looking saturated with Samsung, HTC, Nokia Corporation (ADR) (NYSE:NOK), and Research In Motion Ltd (NASDAQ:BBRY) all trying to get into (or back into) the game.

Of course, businesses can continue to earn excess returns if they have a sustainable competitive advantage. But Apple bulls should rationally reconsider just how strong the company’s moat is. Today, the difference in quality between hardware manufacturers is becoming slimmer by the day, so is the premium Apple Inc. (NASDAQ:AAPL) can charge for its product.

Now I’m not saying Apply doesn’t have some brand strength. As an example, the company’s app ecosystem has proven difficult for rivals (Google excluded) to replicate. But ask yourself this: In every business in which Apple currently competes, will the company’s margins be higher or lower five to ten years in the future? The entire history of the technology industry says lower.

The market is also assuming Apple Inc. (NASDAQ:AAPL) is running into the law of large numbers. In 2012, Apple earned $42 billion in profit. To repeat this feat, Apple Inc. (NASDAQ:AAPL) has to replace declining margins in its other businesses — every single year forever. It’s like the company is on a treadmill where the bigger it grows the faster it must run to stay in place. Even to maintain its current profitability, Apple must create revolutionary hits on par with the iPod, iPad, and iPhone every few years.

This is in total contrast to Google Inc (NASDAQ:GOOG). Google doesn’t have to reinvent entire industries every year (though it might). The company’s search business is consistently profitable and will crank out cash flow year after year, barring no catastrophic changes in the technology landscape. Google Inc (NASDAQ:GOOG)’s earnings are visible three to five (dare I say 10) years out. I’m willing to pay a premium for that visibility.

Can I say the same about Apple Inc. (NASDAQ:AAPL)? Maybe iTV will reinvent the living room? Maybe iWatch will be a hit? But at the moment, we don’t even know for sure if the company is even working on these projects let alone if they will reshape the world. CEO Tim Cook has yet to deliver a blockbuster product and the market isn’t willing to pay a premium to say he will.

Foolish bottom line

So to the Apple bulls, what the market is assuming here sounds perfectly acceptable. Apple isn’t cheap but rather reasonably priced.

The article Why Is Apple so Cheap? originally appeared on Fool.com.

Robert Baillieul has no position in any stocks mentioned. The Motley Fool recommends Apple Inc. (NASDAQ:AAPL) and Google. The Motley Fool owns shares of Apple and Google Inc (NASDAQ:GOOG). Robert is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.

{kind=link}