In the first part of the chemicals-agriculture fertilizer industry analysis, I will provide a life cycle analysis of the industry, introduce the key players in the industry and provide a geographic breakdown of sales for these companies. The second part of the industry analysis will discuss demographics affecting the industry, key inputs used in the industry, and will assess the valuation of the various players in the industry. To conclude the industry analysis, the third section will include Porter’s Five Forces.

Life Cycle Analysis

The agriculture chemical fertilizer industry is in the introductory, growth, and mature phase in its life cycle depending on the location. The fertilizer industry in the U.S. and other wealthy countries has matured, while there’s still room for growth in developing nations. Demand for fertilizer has more than doubled between 1970 and 2012 in the developing world, while in rich countries, farmers have been growing more food with less fertilizer from about 1990 on.

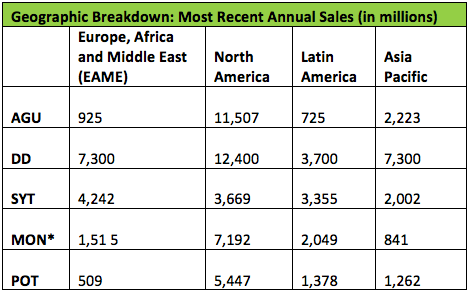

Geographic Breakdown

The leading companies in the crop protection industry are mainly agribusinesses or large chemical companies based in Western Europe and North America. Companies compete on the basis of strength and breadth of product range, product development and differentiation, geographical coverage, price and customer service. Today, Asian and Indian farmers are the major users of fertilizer. One-third of the increase in cereal production (grain used for food) worldwide, and half of the increase in India’s grain production during the 1970s and 1980s has been attributed to increased fertilizer consumption. Looking at the table below, DuPont’s sales are much higher than the other comparables because their product diversity. Agriculture is the company’s largest segment, accounting for roughly 24% of 2011 sales (click here to see why DuPont is one of Barton Bigg’s top picks). The remaining companies’ operations are in one way or another derived from agriculture.

Syngenta AG (NYSE:SYT) is geographically diversified and employs an estimated 26,000 people in over 90 countries. Syngenta sells seed products that are developed using advanced genetics and related technologies in all major territories. Syngenta has more sales from EAME than any other comparable, and even with poor economies in Europe, Syngenta managed to grow sales in the continent at 9% year-over-year. North America is Syngenta’s second largest market and accounted for 28% of Syngenta’s sales in 2011 (U.S. 24%, other 4%). Total N. American sales in 2011 grew 9%, recovering from the 8% decrease in sales in 2010. In Latin America, Syngenta has focused on developments in breeding and transformation activities on corn and sugar cane. Latin America is Syngenta’s third largest market. The region contributed to 25% of total sales in 2011. From 2009 to 2011, sales in this region have grown annually by 20%. The Asia Pacific accounts for 15% of Syngenta’s total sales, and Syngenta expects this market to grow in the future due to various emerging markets such as China, Malaysia, the Philippines, South Korea, Vietnam, and Bangladesh.

*Net sales and long-lived assets are attributed to the geographic areas of the relevant Monsanto legal entities. For example, a sale from the United States to a customer in Brazil is reported as a U.S. export sale.

Monsanto Company (NYSE:MON) specializes in everything from seeds to crop protections. The company had over $1.5 billion in sales from EAME, or roughly 13% of their 2011 sales. EAME was Monsanto’s third largest region in terms of sales, and they had more sales than both Agrium and Potash. North America makes up more of Monsanto’s sales than any other region. Monsanto had more North America sales than every comparable other than Agrium and DuPont, and in 2011 the region account for over 60% of their total sales. Looking at Latin America, Brazil is extremely important for global agriculture, and therefore has been a major priority for Monsanto. Only behind the United States, Brazil is the second-largest exporter of soybeans, and there are vast opportunities for increasing yields through fertilizers. Latin America was Monsanto’s third largest geographic segment, accounting for over 17% of 2011 sales.

With over 750 farm stores across the United States, Agrium Inc. (NYSE:AGU) is the largest agricultural retail operator in the United States. Their services expand outside of retail. Agrium also produces and distributes nitrogen, potash and phosphates. In 2011, Agrium had North American sales over $11.5 billion, the second among the comparables, behind only DuPont. North America accounted for nearly 75% of Agrium’s 2011 sales. The Asia Pacific is Agrium’s second largest region in terms of sales, accounting for nearly 15% of sales in 2011. Both Latin America and the EAME were miniscule in comparison to North America and Asia Pacific.

E I Du Pont De Nemours And Co (NYSE:DD) has a moderately diversified line of products and services. DuPont did not break down their geographic sales by product/service, but they did state that 24% of their 2011 sales came from their agriculture segment. They have focused a large amount of their attention toward becoming a global seed provider. Analysts expect their seed segment to be a major growth contributor in both North America and emerging markets. DuPont had the largest sales among comparables in every region. The largest percentage of their revenues stems from North America, where they had $12.4 billion in sales in 2011. DuPont has increased their North American corn and soybean market share at the expense of Monsanto.

Potash Corp./Saskatchewan (NYSE:POT), the largest independent potash producer, has an oligopolistic position in the market. With only a few major players in the industry, Potash is comfortably positioned to sustain their competitive advantage. The potash producer has focused their marketing efforts toward North America, which explains why the largest amount of sales came from the region. In 2011, Potash received nearly $5.5 billion in sales from North America, or over 60% of their total sales. Relative to their comparables, Potash has the smallest exposure to EAME.

Demographics

The Food and Agriculture Organization (FAO), stated that even though growth rates have been slowing since the late 1970s, the world’s population has nevertheless doubled since that time to 6.9 billion, and is projected to increase considerably over the next few decades. In many developing countries, a combination of declining mortality rates, prolonged life expectancy, youthful age structures and high fertility warrant considerable population increases that are likely to continue until the end of the twenty-first century.

The FAO revealed in The Resource Outlook to 2050, that at this time, more than 1.5 billion hectares of the globe’s land surface (about 12 percent) is used for crop production (arable land and land under permanent crops). There is little scope for further expansion of agricultural land. Although nearly 5 billion hectares of land potentially suitable for agriculture, much of it is covered by forests, protected for environmental reasons, or employed for urban settlements. Arable land per person has decreased 1.5% from 1970 to 2009.

Key Inputs

Nutrient inputs in crop production have been the driving factor behind increased crop yields, but this system of farming has come under increased scrutiny because of the potential for environmental impacts from inputs such as nitrogen (N), potassium (K) and phosphorous (P). Potential risks are often widely publicized while the associated benefits of an abundant, affordable, and healthful food supply can be overlooked or understated. On average, fertilizers attribute up to 60% of crop yields. N, P, and K make up the majority of nutrient inputs necessary to sustain current crop yields. Using these inputs efficiently and in concert is essential in today’s agriculture and will be even more important in years to come. In order to meet the food supply needs of a growing world population, effective use of fertilizers is imperative.

It’s no mystery among the farm community that nitrogen is used by plants to synthesize proteins, nucleic acids and hormones, and phosphorus and potassium act as raw materials for nucleic acids and other proteins. These are the ties that hold together the most important nutrients in modern fertilizers. P and K come from mines and such resources are limited. Atmospheric nitrogen is effectively unlimited, but this is not in a form useful to plants. Ammonia is the most important source of nitrogen in fertilizers and this has made it one of the most important chemicals in the United States. In the past 70 years, the use of fertilizers has more than quadrupled. Farmers are using more and more fertilizer in attempt to boost yields and offset lost fertility that stems from erosion.

Because of increased demand and increased population, the demand for nitrogen based fertilizers will continue to be high. The fertilizer industry is considered a mature industry but a growing and changing one. This is displayed by many fertilizer companies devoting their R&D to finding levers to improve techniques and production methods to lower costs rather than attempting to develop new and different ways of producing fertilizer.

Valuing the Key Players

Syngenta AG (NYSE:SYT) has a market cap of about $34 billion, and is the largest agrochemical business in the world. Their $10.1 billion crop protection division is number one in the world, while its $3.1 billion seed and genomics business is number three in the world. The agrochemical business is trading at 20.53 times their earnings. Syngenta is the only company among the comparables whose current P/E is higher than their five year average P/E. In terms of EV/EBITDA and P/E, Syngenta is more expensive than every company other than Monsanto. The high valuation stems Syngenta’s strong presence in emerging markets and better profit margins than their competitors. Looking at ROA and ROE, Syngenta’s ROA only beats Du Pont, while their ROE only beat Monsanto. Taking a look at SYT’s five year revenue CAGR, the company ranks in the middle of their comparables, growing revenues on average at 10.50%.

Monsanto Company (NYSE:MON) is the largest company among the comparables with a market cap of over 48B. In 1996, Monsanto was the first company to introduce genetically modified crop seeds, and they remain the market leader today. Looking at the valuation, Monsanto has the highest P/E and EV/EBITDA, making it the most expensive among its comparables (click here to see Monsanto’s earnings analysis). Moving the ROA and ROE, Monsanto’s ROA ranks in the middle of their comparable, but they have the worst ROE at 18.17%. The agricultural giant has grown revenues on average at 10% in the last five years, only better than Du Pont.

Agrium Inc. (NYSE:AGU) is the largest agricultural retailer in the United States. With over 1,250 retail centers the Canada based company sells everything from fertilizers to seeds. The retailer is the cheapest among the comparables trading at 10.18 times their earnings with an EV/EBITDA of 6.12. Looking at their ROA and ROE, Agrium has the second highest ROA among the comparables at 10.74%, and the third highest ROE at 24.30%. The company has grown their revenues at a five year CAGR faster than any comparable at 29.80%.

Potash Corp./Saskatchewan (NYSE:POT) is the world’s largest independent potash producer. With a P/E of 14.53 and an EV/EBITDA of 9.72, Potash is more expensive than both Agrium and Du Pont. Looking at ROA and ROE, Potash has the highest ROA at 13.36%, and have the second highest ROE at 30.32%. The independent potash producer has grown revenues at a five year CAGR of 18.30%

E I Du Pont De Menours And Co (NYSE:DD) is a diversified chemical company with products ranging from agriculture to electronics. With a P/E of 13.44 and an EV/EBITDA of 8.46, Du Pont is cheaper than every comparable other than Agrium. Moving to ROA and ROE, Du Pont has the worst ROA among their comparable at 6.52%, but they have the highest ROE at 30.46%. The diversified chemical company has grown revenues the slowest among comparables. Du Pont has a five year revenue CAGR of only 6%.

Hedge Fund Sentiment

Lone Pine Capital is the largest hedge fund holder of Monsanto Company (NYSE:MON). From the first to the second quarter of 2012, Stephen Mandel, hedge fund manager for Lone Pine Capital, increased his interest in Monsanto by 24%. Monsanto is Mandel’s fourth largest holding, accounting for 3.93% of his portfolio. Fisher Asset Management is the largest fund holding Syngenta AG (NYSE:SYT). Through the second quarter of 2012, the fund has increased their shares held by 8%. Jana Partners is the largest hedge fund holder of Agrium Inc. (NYSE:AGU). Barry Rosenstein, the hedge fund’s manager, bought 6.5 million shares of Agrium during the second quarter of 2012. Agrium now makes up 23.51% of Jana Partners’ portfolio.

Adage Capital Management is the largest hedge fund holder of Potash Corp./Saskatchewan (NYSE:POT). Phill Gross and Robert Atchinson, hedge fund managers for Adage, are the largest holders of Potash. The fund has increased their holding in Potash by over 30% year-to-date, and now own 6.4 million shares. Carlson Capital is the largest hedge fund holder of E I Du Pont De Menours And Co (NYSE:DD). Clint Carlson, hedge fund manager for Carlson Capital, has decreased his shares in Du Pont by 16% during the second quarter of 2012.

Porter’s 5 Forces

Competitive Rivalry

The chemical agriculture fertilizer industry is internationally diverse with various competitors located in different areas of the world. Different countries demand different chemicals used for fertilizing their crops. Larger companies in the industry operate in many countries and focus their internal growth efforts in countries that are expanding their agriculture production. The supply-demand balance in the industry, and therefore also the fertilizer prices, cannot be influenced by any single producer. The fertilizer industry operates in a global market, where only companies that manage to increase productivity can prosper in the face of global competition.

Threat of New Entrants

Changing consumption patterns opens opportunities for structural changes in the markets. Our analysis suggests that relatively smaller firms can now better compete with the giants in the fertilizer market. Nearly half the fertilizer production comes from smaller companies; this shows that the door is always open for new entrants to come into the market and snag market share from the larger fish, so to speak.

Bargaining Power of Buyers

Farmers are the primary buyers of products that come from this industry. Many analysts believe that whenever there are significant rises in grain prices, the fertilizer companies raise prices in order to get a larger share of the farmers’ profits. In 2008, corn prices rose to more than $6 per bushel due to an increased demand for corn in ethanol production. Subsequently, fertilizer prices rose to all-time highs before dropping back to normal levels by the summer of 2009 once corn prices readjusted. Farmers do not have buying power, because fertilizers companies hold the valuable ingredient necessary to improve crop yields.

Bargaining Power of Suppliers

The chemical agriculture industry is labeled in the “perfect” category of competition. Theoretically, perfectly competitive industries are known as price takers, and cannot influence the price that is paid for their product. Therefore, firms in a competitive environment are more hard-pressed to reduce costs and become more efficient. A firm that makes inefficient decisions incurs losses because it cannot transmit its extra costs to the consumers.

Threat of Substitutes

Advances in agricultural technology—including, but not limited to, the genetic modification of food crops—have made fields more productive than ever. Farmers grow more crops and feed more people using less land. They are able to use fewer pesticides and to reduce the amount of tilling that leads to erosion. Scientists are attempting to introduce advanced crops that are designed to survive heat waves and droughts, resilient characteristics that will become increasingly important in a world marked by a changing climate. Genetically modified (GM) agriculture has various benefits, but is still in the product acceptance stage. It’s important for companies in the chemical and agriculture fertilizer industry to be aware of the situation, and understand that if GM crops become safe and cost effective, demand for fertilizer could diminish.

Related tickers: Syngenta AG (NYSE:SYT), Monsanto Company (NYSE:MON), Agrium Inc. (NYSE:AGU), Potash Corp./Saskatchewan (NYSE:POT), E I Du Pont De Menours And Co (NYSE:DD), Ceres Inc (NASDAQ:CERE), FMC Corporation (NYSE:FMC), Devgen NV (EBR:DEVG), Scotts Miracle-Gro Co (NYSE:SMG), American Vanguard Corp (NYSE:AVD), Origin Agritech Ltd. (NASDAQ:SEED), TyraTech, Inc. (LON:TYR), Mosaic Co (NYSE:MOS), CF Industries Holdings, Inc. (NYSE:CF), Rentech, Inc. (NYSEAMEX:RTK), Terra Nitrogen Company, L.P. (NYSE:TNH), CVR Partners LP (NYSE:UAN), Rentech Nitrogen Partners LP (NYSE:RNF).