Is newspaper publishing dying? Definitely not for Gannett Co., Inc. (NYSE:GCI), which is betting big with its “All-Access Content Subscription Model” or “paywall” roll-out. Gannett Co., Inc. (NYSE:GCI) publishes 82 daily newspapers, including USA TODAY, which is the nation’s largest-selling daily newspaper. Smart investors may find value in the newspaper business for its solid free cash flow and steady returns. By taking a bold move to initiate the new paywall model, Gannett is moving forward with new growth drivers from digital publishing and circulations.

Recent development

For Q1, Gannett Co., Inc. (NYSE:GCI) reported earnings of $0.44 per diluted share on a GAAP basis as compared to $0.28 last year. Operating income increased $15 million as compared to the same quarter in 2012 due to a strong increase in the Broadcasting and Digital segments, offset by a decline in the Publishing segment. Digital segment continued its strong growth with 45% increase in operating income, whereas the Publishing segment witnessed a 3% decline in operating income due to advertising softness.

The Publishing segment had 9% growth in circulation and 5% decline in advertising as compared to the same quarter in the previous year. The decline of advertising revenue was mainly due to slow economic growth. Management continues to reduce the expense on the newsprint end by restricting workforce and consolidating facility. On the other hand, Gannett Co., Inc. (NYSE:GCI) continues to benefit from the new paywall model adopted last year for its digital newspaper products, as a result of which digital revenue jumped more than 75% at its publishing segments. More people paid to access news online and through apps for mobile devices.

Looking forward, the company is expecting lower revenue from the Broadcasting segment due to the absence of Olympics and lower political advertising. However, retransmission revenue should help offset the overall decline for Broadcasting segment with a 40%-45% revenue increase. On the digital end, the growth rate will be slower than 2012 due to the cyclic effect of the All-Access Content Subscription Model, which was rolled out and implemented throughout 2012.

What now?

All-Access Content Subscription Model is critical for Gannett’s long-term success. Eventually, Gannett Co., Inc. (NYSE:GCI) will develop a standardized platform or mobile app which would allow all newspapers to be distributed via a standardized, effective channel, where each local newspaper will be branded and marketed locally. The new platform/model will also help Gannett gather more data from readers, which will help the company plan an optimized strategy for each newspaper.

The advertisement revenue for printing newspapers will continue to decrease, but the rate of declining will eventually level off. At the same time, with the successful implementation of this new paywall model, circulation and digital revenue will continue to grow at a faster rate. With strong cash flow support, Gannett Co., Inc. (NYSE:GCI)’s outlook looks much more brighter than a few years ago.

Competition

Gannett’s key stats will be compared to its peers, including The New York Times Company (NYSE:NYT) and The Washington Post Company (NYSE:WPO).

The New York Times Company (NYSE:NYT) continues to suffer from reduced advertising revenue. However, the company managed to achieve operating profit increase by carefully managing costs and increasing circulation revenue, led by continued strength in digital subscription initiatives. The company continues to re-position itself for the evolving media environment, and is working on re-branding, as well as leveraging The Times brand to create new products and services. Unlike Gannett, New York Times is working on a different approach to enhance its brand value.

Unlike Gannett and New York Times, The Washington Post Company (NYSE:WPO) has evolved from a traditional newspaper company to a diversified holding company, where majority of operating profit is now contributed from its education division and cable and television broadcasting operations.However, in the most recent quarter, only broadcasting segment witnessed growth while the newspaper publishing segment continued to decline, and the education division also suffered from decreasing revenue and increasing restructuring cost. The near-term view for Washington Post remains neutral.

These three companies will be reviewed for their revenue growth, profit margins, ROE, and free cash flows.

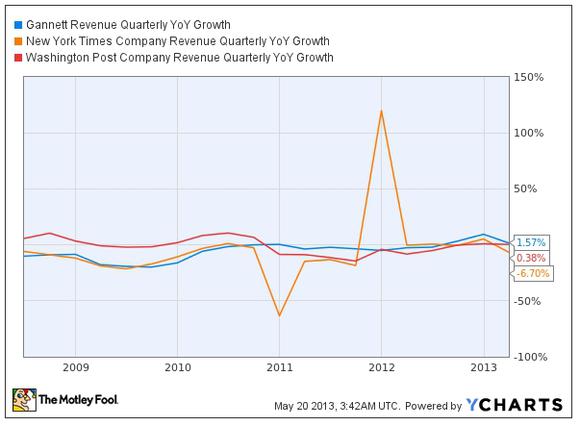

Compared to New York Times, the revenue growth rate for Gannett and Washington Post had been relatively stable throughout mid-2010 to early 2013. Currently, Gannett has the highest revenue growth rate in Q1 2013 as compared to the other two.

Although Gannett has the lowest profit margin among the three, it has a relatively consistent profit margin since 2010. On the other hand, New York Times and Washington Post’s profit margins have been declining gradually since early 2010.

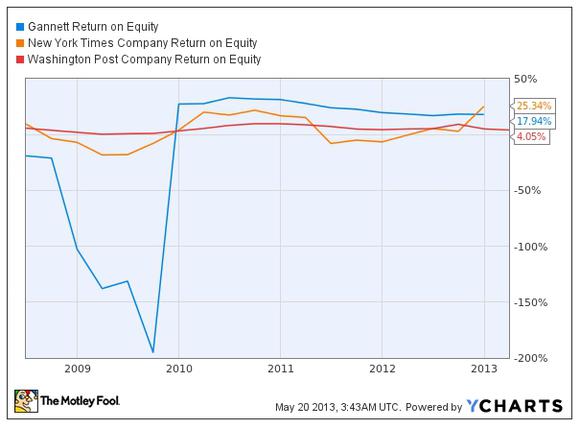

By taking out the wide swing in 2009, Gannett had the highest ROE among the three companies since early 2010 to late 2012. However, New York Times’ ROE has been increasing since mid-2011 and surpassed Gannett’s in late 2012.

Gannett continues to have the most solid free cash flow as compared to the other two companies. At the end of 2012, Gannett’s free cash flow was almost twice of Washington Post’s while Times had a negative cash flow.

Bottom line

While the media business continues to be dragged by secular decline of the newspaper printing business, Gannett’s overall revenue was helped by the improving digital segment and continuous cost reduction, as well as the new paywall model. However, investors should not expect much revenue growth for 2013 due to the absence of Olympics and reduced political spending after the 2012 election. Overall, Gannett remains a strong pick in the newspaper printing/media business with its stabilized revenue, consistent ROE, and solid free cash flow.

The article This Newspaper Company Is Still Solid originally appeared on Fool.com and is written by Nick Chiu.

Nick is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.