The COVID Crisis

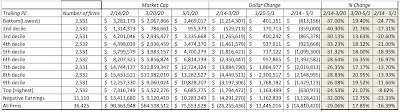

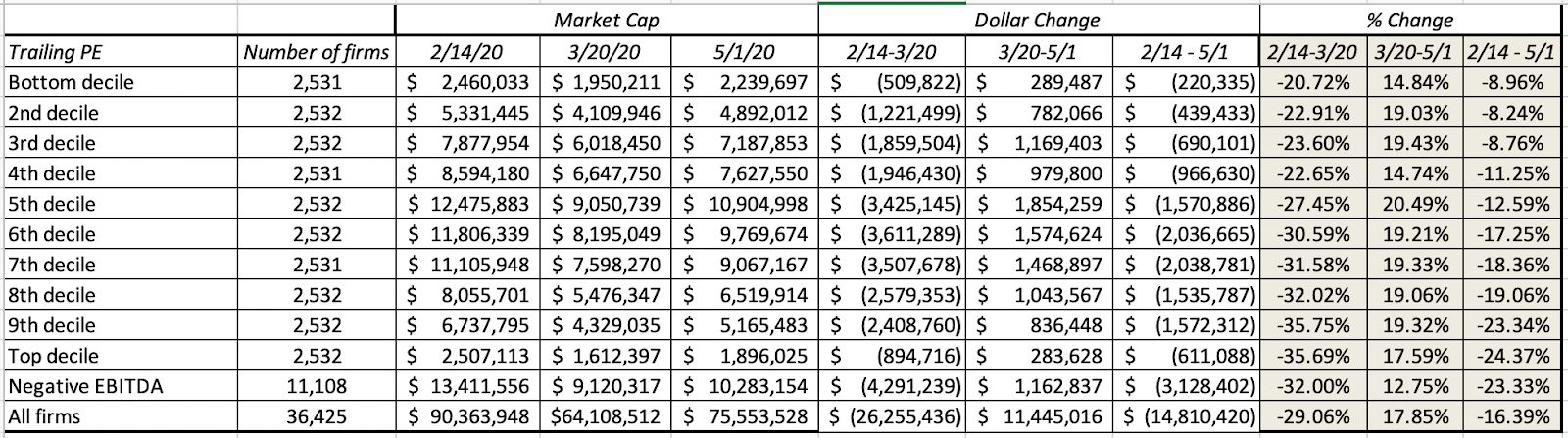

In the early days of the crisis, there were many value investors who viewed at least some of the market correction as punishment for investor overreach on growth and momentum stocks in the past decade. As the weeks have progressed, that argument has been quelled by the cumulating evidence that the market punishment perversely has been far worse for value stocks, i.e., stocks with low PE ratios and high dividend yields than for momentum or growth stocks. To illustrate this, I first look at how the market effects have varied across stocks in different PE ratio classes:

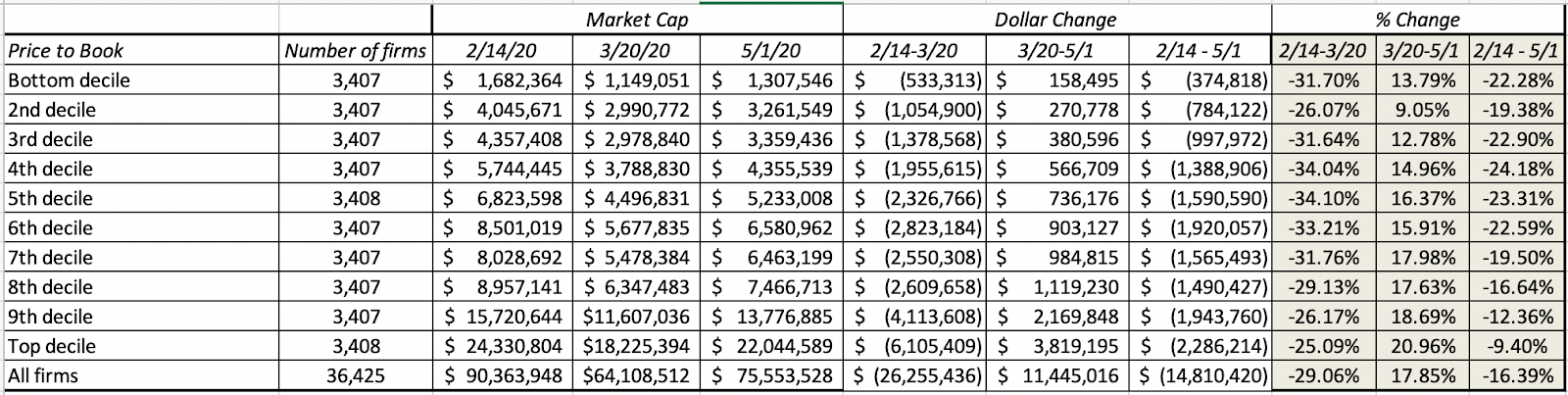

Note that it is the lowest PE stocks that have lost the most market capitalization (almost 25%) between February 14 and May 1, whereas the highest PE stocks have lost only 8.62%, and to add insult to injury, even money losing companies have done better than the lowest PE stocks. I follow up by looking at stocks broken down by price to book ratios:

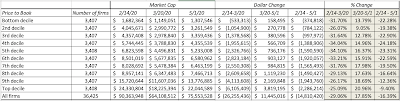

The results mirror what we saw with PE stocks, with low price to book stocks losing far more value than the highest price to book stocks. I then break down stocks based upon dividend yields:

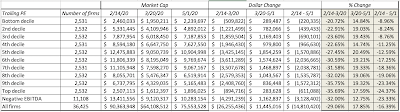

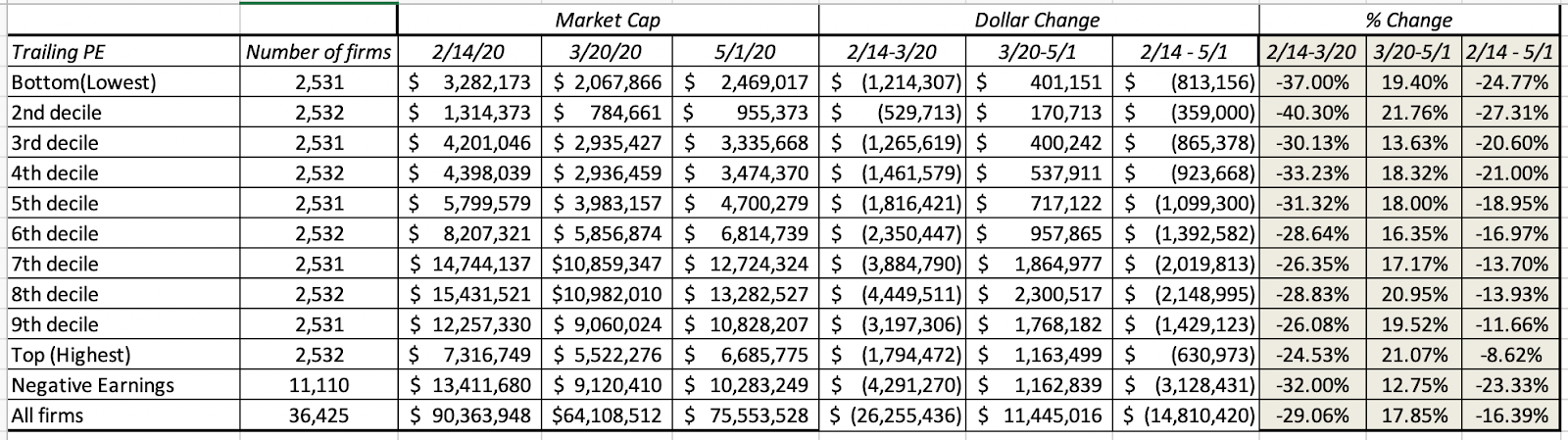

Low dividend yield stocks and even non-dividend paying stocks have fared far better than high dividend yield stocks. Finally I look at companies, based upon net debt ratios:

Put simply, here is what I see in the data. If I had followed old-time value investing rules and had bought stocks with low PE ratios and high dividends in pre-COVID times, I would have lost far more than if I bought high PE stocks or stocks that trade at high multiples of book value, paying little or no dividends. The only fundamental that has worked in favor of value investors is avoiding companies with high leverage.

A Personal Viewpoint

I believe that value investing has lost its way, a point of view I espoused to portfolio managers in Omaha a few years ago, in a talk, and in a paper on value investing, titled Value Investing: Investing for Grown Ups?In the talk and in the paper, I argued that much of value investing had become rigid (with meaningless rules and static metrics), ritualistic (worshiping at the altar of Buffett and Munger, and paying lip service to Ben Graham) and righteous (with finger wagging and worse reserved for anyone who invested in growth or tech companies). I also presented evidence that it was bringing less to the table than active growth investing, by noting that the average active value investor underperformed a value index fund by more than the average growth investor lagged growth index funds.

I also think that fundamental shifts in the economy, and in corporate behavior, have rendered book value, still a key tool in the value investor’s tool kit, almost worthless in sectors other than financial services, and accounting inconsistencies have made cross company comparisons much more difficult to make. On a hopeful note, I think that value investing can recover, but only if it is open to more flexible thinking about value, less hero worship and less of a sense of entitlement (to rewards). If you are a value investor, you will be better served accepting the reality that you can do everything right on the valuation front, and still make less money than your neighbor who picks stocks based upon astrological signs, and that luck trumps skill and hard work, even over long time periods.