Active versus Passive Investing

Some of the readers of this blog are in the active investing business and I apologize in advance for raising questions about your choice of profession. After all, any discussion of active versus passive investing that comes down on the side of the latter implicitly is a judgment of whether you are adding value by trying to pick stocks or time markets. Consequently, these discussions quickly turn rancid and personal, and I hope this one does not.

The Difference

In passive investing, as an investor, you allocate your wealth across asset classes (equities, bonds, real assets) based upon your risk aversion, liquidity needs and time horizon, and within each class, rather than pick individual stocks, bonds or real assets, you invest in index funds or exchange traded funds (ETFs) to cover the spectrum of choices. In active investing, you try to time markets (by allocating more money to asset classes that you believe are under valued and less to those that you think are over valued) or pick individual assets that you believe offer the potential for higher returns. Active investing covers a whole range of different philosophies from day trading to buying entire companies and holding them for the long term.

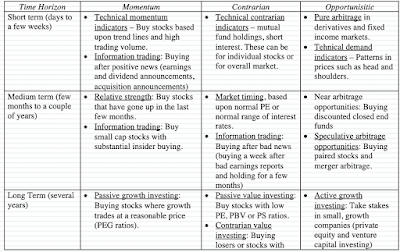

Put simply, active investing covers a range of philosophies with different time horizons, different and often contradictory views about how markets make mistakes and correct them,

The Lead In

Until the 1970s, active investing dominated passive investing for two simple reasons. The first was the presumption that institutional investors were smarter, and had access to more information than the rest of us, and should thus do better with our money. The second was that there were no passive investing vehicles available for average investors. Both delusions came crashing down in the late sixties and early seventies.

– First, the pioneering studies of mutual fund performance, including this famous one that introduced Jensen’s alpha, came to the surprising conclusion that rather than outperform markets, mutual funds under performed by non-trivial amounts. In the years since, there have been literally hundreds of studies that have asked the same question about mutual funds, hedge funds and private equity, using far richer data sets and more sophisticated risk adjustment models to arrive at the same result. You can see Morningstar’s 10-year excess return distribution for all active large-blend mutual funds, from 2010-2019, below (with similar graphs for other classes of active mutual funds):

If the counter is that it is hedge and private equity funds where the smart money resides today, the evidence with those funds, once you adjust for reporting and survivor bias, mirrors the mutual fund results. Put bluntly, “smart” money is not that smart, and the advantages that it possesses (bright people, more data, powerful models) don’t translate into returns for its investors. Ironically, over the same period, there were hundreds of other studies that claimed to find market inefficiencies, at least on paper, suggesting that there is no internal inconsistency in believing that markets are inefficient and also believing that bearing these markets is really, really difficult to do.

– Second, Jack Bogle upended investment management in 1976 with the Vanguard 500 Index fund, the most disruptive change in the history of the investment business. Over the next three decades, the index fund concept expanded to cover geographies and asset classes, allowing investors unhappy with their investment advisors and mutual funds to switch to low-cost alternatives that delivered higher returns. The entry of ETFs tilted the game even further in favor of passive investing, while also offering active investors new ways of playing sectors and markets.