Value versus Growth Investing

In the tussle between value and growth investing, value investors have held the upper hand for a long time. In addition to laying claim to being the custodians of value, they also seemed to have all the numbers on their side of the argument, as they pointed to decades of outperformance by value stocks, at least in the United States. The last decades, though, have delivered numbers that are more favorable to growth investors, and this crisis is perhaps as good a time as any to reexamine the debate.

The Difference

For decades, we have accepted a lazy categorization of stocks on the value versus growth dimension. Stocks that trade at low PE or low price to book ratios are considered value stocks, and stocks that trade at high multiples of earnings and book value are growth stocks. In fact, the value factor in investing is built around price to book ratios. If you are a value investor, your reaction to this categorization is that this is no way to describe value and that true value investing incorporates many other dimensions including management quality, sustainable moats and low leverage. Conceding all those points, I would argue that the key difference between value and growth investing can be captured by looking at a financial balance sheet:

Thus, the real difference between value and growth investors lies not in whether they care about value (sensible investors in both groups do), but where they believe the investing payoff is greater. Value investors believe that it is assets in place that markets get wrong, and that their best opportunities for finding “under valued” stocks is in mature companies with mispriced assets in place. Growth investors, on the other hand, assert that they are more likely to find mispricing in high growth companies, where the market is either missing or misestimating key elements of growth.

The Lead In

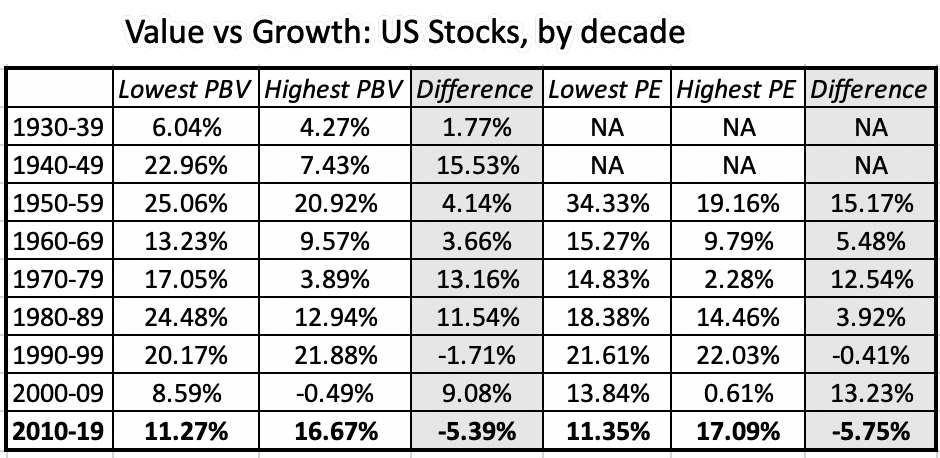

Until the last decade, it was conventional wisdom that value investing beat growth investing, especially over longer time horizon, and the backing for this statement took the form of either anecdotal evidence (with the list of illustrious value investors much longer than the list of legendary growth investors) or historical data showing that low price to book stocks have delivered higher returns than high price to book stocks:

|

| Source: Raw Data from Ken French |

Looking across the entire period (1927-2019), low price to book stocks have clearly won this battle, delivering 5.22% more than high price to book stocks, and this excess return is almost impervious to risk and transaction cost adjustments. Value investors entered the last decade, convinced of the superiority of their philosophy, and in the table below, I look at the difference in returns between low and high PE and PBV stocks, each decade going back to the 1920s.

It is quite clear that 2010-2019 looks very different from prior decades, as high PE and high PBV stocks outperformed low PE and low PBV stocks by substantial margins. The under performance of value has played out not only in the mutual fund business, with value funds lagging growth funds, but has also brought many legendary value investors down to earth. Pushed to explain why, the defense that value investors offered was that the 2008 crisis, Fed interventions and the rise of the FAANG stocks created a perfect storm that rewarded momentum and growth investing, at the expense of value. Implicit in this argument is the belief that this phase would pass and that value investing would regain its rightful place.