An article came out toward the end of 2012 highlighting 10 of the fastest growing industries in America. What are some of the industries, and who is poised to cash in on this growth? Read on.

3D printing

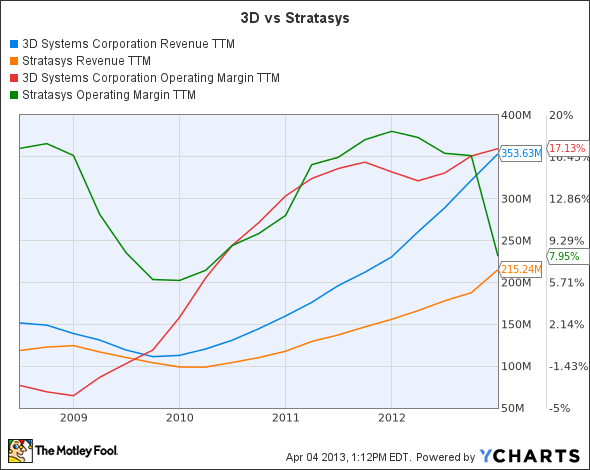

You may already know it, but 3D printing is kind of a big deal. The industry has been growing almost 9% a year since 2002. But that is a little misleading, because the growth is still gaining momentum. 2012 was a huge year. This year, estimates call for around 20% industry growth.

Trying to take advantage of this growth is 3D Systems Corporation (NYSE:DDD) and competitor Stratasys, Ltd. (NASDAQ:SSYS).

DDD Revenue TTM data by YCharts

Not all companies are created equal. Just because a company is doing business in a growing sector does not ensure that they will be a winner. Stratasys, Ltd. (NASDAQ:SSYS) has been facing some headwinds – things like a falling operating margin. The stock is facing some negative feelings from hedge funds, and has even been downgraded by TheStreet. However, to be clear, while there is some negative sentiment, the general sentiment was positive in regards to the the most recent earnings report. Net income was up 40%. When the company released the quarterly report, shares went soaring.

What is the future of 3D printing? From now until 2017, the industry is expected to keep growing at the break-neck speed of 14% a year. That’s some growth I want to be around.

Online education

Getting your higher educational needs taken care of on the internet used to be something that seemed a little shady. Not so anymore. Since 2002, online education has been growing over 13% per year. This past year growth slowed a bit, but many still believe that online education is the direction higher education is going to continue to move. Consider that the University of Wisconsin is now one of several physical colleges that offer a 100% legit degree without ever having need to step in a classroom.

Apollo Group Inc (NASDAQ:APOL) is one of the better known players in this sector, specifically with its brand the University of Phoenix.

APOL Net Income TTM data by YCharts

Despite its size and brand recognition, it appears that Apollo Group has lost their way financially speaking. Despite an industry that is growing 13% a year, during the past five years Apollo has seen revenue barely creep forward, and income has actually gone backwards. Some will attribute these losses to the number of colleges now offering MOOC: Massive Open Online Courses. This slew of new competitors certainly has hit Apollo Group Inc (NASDAQ:APOL).

But not everyone in the for-profit education business has been struggling. While Apollo’s numbers are all heading the wrong way, Grand Canyon Education Inc (NASDAQ:LOPE) has been hitting its stride.

LOPE Net Income TTM data by YCharts

Net income is up over 1,000% over the past five years. And their valuation has come way down. You can get into this investment at a price just around 15 times earnings. Based on performance for the last five years, and based on offering 2013 guidance above Wall Street’s hopes and dreams, it seems like Grand Canyon Education Inc (NASDAQ:LOPE) could be poised to take advantage of the growing industry.

Social gaming

This one was hard for me to believe, but social network gaming is one of the big growth trends in our world right now. Zynga Inc (NASDAQ:ZNGA) is perhaps the best known player in this industry right now.

And people are actually getting really excited about Zynga. Shares went sailing over 15% with word that they are getting into online gambling in the UK.

ZNGA Revenue TTM data by YCharts

You can see why some investors are beside themselves like a dog in a fire hydrant museum. Revenue has largely plateaued for the company. Net income and free cash flow are going the wrong way. Something has to give for this company. They didn’t turn a profit last year, and it’s not expected this year either. This online gambling provides a glimmer of hope for investors.

The industry is expected to grow 22% annually until 2017. That is some big time growth potential. I’m just not sure that Zynga Inc (NASDAQ:ZNGA) is going to be the one to capitalize on it.

Final thoughts

These industries are high growth both now and for the next few years at least. Within these industries there will be some big time winners. If you’re are looking for a home run opportunity, looking inside these industries for the best company may be your best chance.

The article Investing in Major Growth originally appeared on Fool.com and is written by Jon Quast.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.