A look at reserve valuations in the larger cap independent oil & gas universe paints a widely varied picture. Barrels can be had for prices ranging from less than $9 to almost $30. The wide spread has a rational reason. No two companies’ reserves are easily comparable and simple value metrics ignore that fact. When a valuation looks out of whack with reality, it’s a good idea to try to find a rational reason. You often gain insight into the underlying story that’s driving the stock.

These ratios are useful and can help identify mispriced stocks, but some qualifiers are warranted. Mr. Market’s not always as dumb as he’s made out to be. Getting under the hood to understand why an apparent mispricing might be rational is necessary.

Apples aren’t oranges

Price per barrel of oil equivalent (BOE) is a useful metric, but it’s a blunt instrument. By its very nature, the BOE convention lumps apples in with oranges, so that companies with distinct reserve portfolios can be compared to each other. Like many things in life, the simple approach is useful and simultaneously, inadequate.

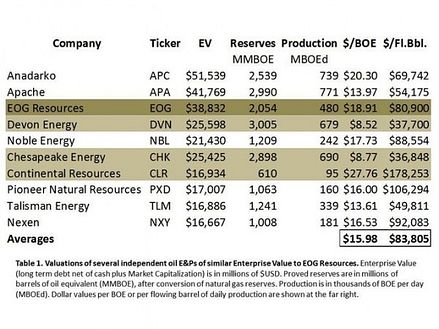

It’s difficult to lump companies like Apache Corporation (NYSE:APA) and Anadarko Petroleum Corporation (NYSE:APC) that have diverse portfolios, in with dedicated North American shale drillers like Devon Energy Corporation (NYSE:DVN), EOG Resources, Inc. (NYSE:EOG) or Chesapeake Energy Corporation (NYSE:CHK). Smaller independents like Noble Energy, Inc. (NYSE:NBL) and Nexen Inc. (USA) (NYSE:NXY) with sizeable international holdings and offshore operations arguably deserve yet another bushel for comparison. Pure offshore operators, provide yet another bushel.

Anadarko has considerable international and offshore drilling opportunities. The company will operate nine Deepwater drilling rigs in FY 2013. A quarter of its production comes from the Gulf or overseas. Devon is tethered to its North American shale plays. These are very different companies. With North American gas and mid-continent oil prices low, you can begin to understand Anadarko’s premium. Anadarko holds the acreage diversity of a Major in the wrapper of an Independent.

What’s in that barrel?

The brightest line separating companies right now is their oil/gas mix. Reserve reports normalize oil and gas reserves based on the energy they contain. When burned, 6 mcf (thousand cubic feet) of natural gas yields about the same amount of energy as 1 barrel (42 US gallons) of oil.

Natural gas reserves are mathematically converted into their equivalent amount of oil, totaled with liquid reserves and reported as BOE. The same can be done in reverse, converting barrels of oil to mcf, adding gas and reporting the sum as cubic feet equivalent (CFE). In either case, the goal is to quote reserves based on the energy they contain.

Since there’s no accounting for the disparate economic value of gas and oil, one BOE of Devon Energy Corporation (NYSE:DVN)’s gas-rich reserves simply aren’t equal in value to one BOE of EOG’s oil-rich reserves. At $3.50 per mcf, one BOE of natural gas fetches about $21 compared to roughly $100 for the barrel of oil. Given that wide spread, oil-rich portfolios warrant considerably higher valuations right now.

Nor is all oil equal. Oil quality differs considerably source by source. Devon’s heavy Canadian crude and syncrude fetch lower prices than EOG or Continental Resources, Inc. (NYSE:CLR)’s Bakken light sweet crude, because light sweet has more refining value. EOG has the industry leading acreage position in the oil-window of the Eagle Ford, and holds substantial Bakken acreage. Continental leads the red-hot Bakken. These high value oil-rich acreage positions account for their premium valuation.

Supply and demand trumps all

In the US, producers delivering at Cushing, OK (West Texas Intermediate) net back less in cash than those that can deliver crude to the Gulf Coast (Louisiana Light Sweet). The spread between WTI and LLS reflects supply and demand differences. With more delivery options to the coastal US markets, LLS prices higher.

The same can be said for gas. We’re used to cheap gas in the US, but that’s not the case everywhere. Oil is shipped all over the globe, but natural gas remains a regionalized market. It needs to be liquefied to ship it and until North America has the capacity to export LNG, our oversupply won’t affect global pricing one bit.

Diversified international operations compensate for regional pricing problems. Apache’s international operations account for 45% of total production. In 2011, its average international gas pricing exceeded domestic gas by 20%, and 70% of its oil production priced at a premium to WTI. Geographical diversification helps protect Apache from the effects of regionally depressed prices, changing its risk profile.

Make sure of your numbers

This is a numbers-driven industry that’s overflowing with jargon. Make sure that your reserve numbers are what you think they are when comparing a company to its peers.

Reserves come in three flavors: proved, probable and possible in descending probability of their recovery (90%, 50% and 10%, respectively). Proven reserves are split between ‘proved developed’ and ‘proved undeveloped’. Proven developed reserves are all behind pipe on properties with existing infrastructure. It’s ready to come out of the ground.

You’ll also see the terms 1P, 2P and 3P. In this case, reserve totals are additive. 1P reserves are proved. 2P are proved plus probable, and 3P are proved, probable and possible. Don’t accidentally comp 2P from one company to probable reserves from another. Scrounging up numbers can be headache, and errors are easy to make because of the heavy use of jargon. Be careful. It’s easy to get crossed up when combing through presentations and SEC documents.

The numbers don’t lie, but they can fib a little…

Be careful with the numbers. Comparisons require that companies you’re looking at have similar assets. Global supply, regional market conditions, swinging commodity prices, and the political environment, can all significantly impact the value of those reserves. Layer on technical and geological differences and comparing reserves can be daunting.

Simple valuations are useful as a screen, but I think that the first thing to ask when you see a low valuation is always, “Why?” Someone’s mispricing it. Either it’s you or the market. You can often find a rational reason behind that price. Finding that ‘story’ behind the stock goes a long way towards helping you identify a company’s strengths and weaknesses. Identifying these helps identify catalysts and make smart buy/sell decisions. This is a commodity business and product price swings can rapidly translate into share price swings. Knowing what exactly what you’re buying and why you’re buying it is essential.

The article When Is a Barrel Not a Barrel? originally appeared on Fool.com and is written by Peter Horn.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.