A SWOT analysis is a look at a company’s strengths, weaknesses, opportunities, and threats, and is a tremendous way to gain a detailed and thorough perspective on a company and its future. As 2013 begins, I would like to focus on a global trailblazer in the discount retail industry: Wal-Mart Stores, Inc. (NYSE:WMT).

The Business:

Warren Buffett once said, “Never invest in a business you can’t understand.” This not only allows the investor to purchase a company with conviction, however also allows them to spot trends blind to unfamiliar eyes. With this in mind, investors in any company should fully understand the business model of the company. Wal-Mart is a global operator of retail stores under the company’s primary brand, Wal-Mart, and their membership retail format brand, Sam’s Club. Currently, there are about 3,960 Wal-Mart stores in the United States, 6,450 Wal-Mart stores internationally, and 622 Sam’s Clubs locations. Based on market capitalization, the company is valued at $231.82 billion. Because of the extremely competitive nature of the discount retail industry, Wal-Mart possesses a profit margin of 3.19%.

1). Steady Revenue Growth: In 2007, Wal-Mart reported revenue of $344.99 billion; in 2012, the company announced revenue of $446.95 billion, representing year over year annual growth of 5.32%, a strong trend that is highly anticipated to continue into the future, with projections placing 2017 revenue at $587.10 billion. This growth has been a direct result of substantial growth in store count and further adoption of their low price platform because of rough economic conditions.

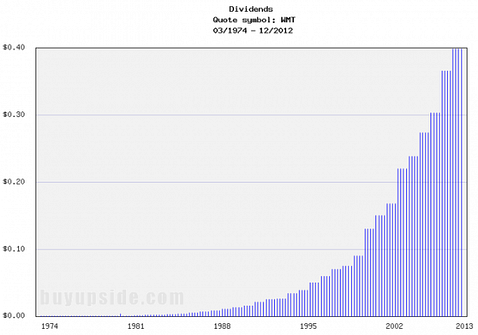

2). Dividend: Currently, Wal-Mart pays out quarterly dividends of $0.40, which when annualized puts the dividend as yielding 2.29%

3). Basement Valuation: Presently, the company carries a price to earnings ratio of 14.26, a price to book ratio of 3.32, and a price to sales ratio of 0.52, all of which indicate a company trading with a basement valuation

4). Relatively Low Volatility: At the moment, Wal-Mart possesses a beta ratio of 0.36, representing a company trading with considerably less volatility than the overall market, a major advantage for long-term investors

5). Positive Free Cash Flow Position: In 2013, the company is projected to generate $14 billion in free cash flow, allowing the company to reward shareholders or reinvest in their own business

6). Strong Total Asset Growth: Total assets of the company have grown from $163.20 billion in 2008 to $193.41 billion in 2012, and this trend of strong asset growth is extremely advantageous

7). Recession Proof Business: The great majority of Wal-Mart’s core business is concentrated in the sale of necessity products, such as toilet paper and toothpaste, and with this characteristic comes a near recession proof business, one that has not suffered as greatly as others in times of economic downfall

Weaknesses:

1). Lack of Movement Over the Past Decade: Over the past decade, the company’s stock has only increased 41%, not taking into account dividends, which have underperformed the broader market by nearly 40 percentage points, despite record revenues and earnings–a weakness as fundamentals have not been driving the stock’s performance

2). Net Debt: Despite possessing $8.6 billion of cash and cash equivalents on their balance sheets, the company’s debt load of $77 billion results in a rather substantial net debt, a major weakness for investors

Opportunities:

1). Dividend Growth: Since implementing their dividend program in 1973, Wal-Mart has consistently raised their dividend payouts, a trend that is widely anticipated to continue into the future

2). Store Count Growth: The number of the United States Wal-Mart stores has increased from 3,660 in 2008 to 3,960 currently, with international store count growing from 3,600 in 2008 to 6,450 currently, and further growth in store count is anticipated in both of these segments, providing opportunity for the company

3). Increasing Revenue per Square Foot: Utilizing every square foot of every location the company possesses more efficiently is a very real opportunity for the company to streamline their business and improve margins

4). Market Share: Wal-Mart operates in an extremely competitive industry, and any gain in market share the company is able to obtain could fuel sales growth

Threats:

1). Rising Input Prices: Wal-Mart prides itself on offering products for the lowest price, however when input prices rise, the company must choose to sacrifice margins or potentially lose customers

Competitors:

Major publicly traded competitors of Wal-Mart include Target Corporation (NYSE:TGT), Costco Wholesale Corporation (NASDAQ:COST), Dollar General Corp. (NYSE:DG), and Dollar Tree, Inc. (NASDAQ:DLTR). All of these companies operate in the discount retail industry and compete directly with Wal-Mart. Target is valued at $40.16 billion, pays out a dividend yielding 2.33%, and carries a price to earnings ratio of 13.67. Costco is valued at $44.51 billion, pays out a dividend yielding 1.08%, and carries a price to earnings ratio of 25.36. Dollar General is valued at $14.58 billion, does not pay out a dividend, and carries a price earnings ratio of 16.20. Dollar Tree is valued at $9.34 billion, does not pay out a dividend, and carries a price to earnings ratio of 16.54.

The Foolish Bottom Line:

Financially, Wal-Mart is an incredible company. The company possesses solid and steady revenue growth in all economic cycles, a rapidly expanding dividend, and a basement valuation. The only true weakness of the business is its debt load. Looking forward, Wal-Mart’s future is filled with fast-paced international expansion, and steady growth in the United States. All in all, Wal-Mart shares currently trade at a rock-bottom valuation, the company is of the finest caliber in terms of reliable revenue and dividend growth, and in the end is a tremendous investment for any long-term investor that will trounce the overall market for decades to come.

The article 50 Years of Stability, Dividends, and Growth originally appeared on Fool.com and is written by Ryan Guenette.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.