Royal Caribbean Cruises Ltd (NYSE:RCL) has been pummeled by the market downturn resulting from the coronavirus scare. The stock is down over 30% in the past month and roughly 40% year-to-date. Simultaneously, the valuation has gone down to ~8.6X based on earnings and yield has shot up to almost 4%. As Baron Rothschild famously said, “buy when there is blood on the streets”, which means pretty much going against the crowd and when the fear factor is very high. For income investors, it may be possible to get a company with leading market share and a low valuation and high dividend yield. But with that said, dividend safety is of concern since it was cut during the Great Recession and was not reinstated until 2012.

Q4 2019 hedge fund letters, conferences and more

Overview of Royal Caribbean

Royal Caribbean is a cruise company that was founded in 1968. It operates under the Royal Caribbean International, Celebrity Cruises, Azamara Club Cruises, and Silversea Cruises brands. These brands operate either globally or regionally depending on their focus. Currently, the company has approximately 61 ships with another 15 on order. In 2019, the company carried ~6.5 million passengers. The company is one of the few large players in the industry. Major competitors include Carnival Corporation (CCL) and Norwegian Cruise Line Holdings (NWL).

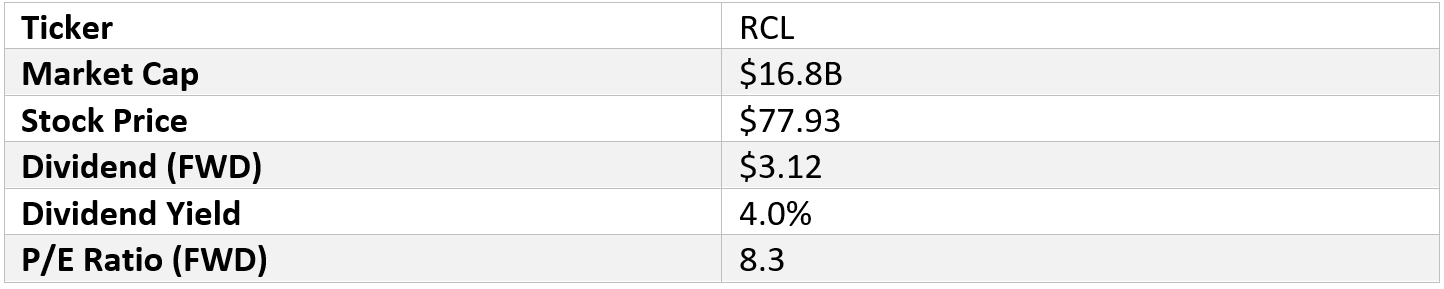

Selected Data for Royal Caribbean (NYSE)

Source: Data from Seeking Alpha

Dividend and Safety

Royal Caribbean’s forward dividend is now $3.12 giving a forward dividend yield of about 4.0%. This is double the S&P 500’s average yield of ~2.0%, which seems to make it a good option for those seeking a high yield stock for income. The dividend has been raised for seven consecutive years making the stock a Dividend Challenger. But the full impact of the coronavirus is probably not known at this point but certainly it will affect the bottom line. Hence, one should take a closer look at dividend safety metrics.

From an earnings perspective the dividend is reasonably safe. The current payout ratio is roughly 33.3% based on the forward dividend and consensus 2020 earnings per share of $9.37. This is well below my threshold of 65% and suggests that the dividend is safe. The dividend has been growing a double-digit rate for the past several years although the growth rate is slowing. The low payout ratio means that the dividend can be maintained even if earnings take a hit from an economic slowdown.

However, the dividend is not as well covered by free cash flow due to high capital expenditures from investing in ships. In fiscal 2019, operating cash flow was $3,716M and capital expenditures were $3,025M giving free cash flow of $691M. The dividend required $603M giving a dividend-to-FCF ratio of ~87%. This is above my threshold of 70%. If free cash flow is too high the company will need to use cash on hand, credit line, or debt to pay the dividend. The main risk is that cruising slows down due to the coronavirus leading to a drop in operating income. This would push the cash flow dividend safety metric over 100%. If cash flow does not cover the dividend for too long, then the dividend could possibly be cut.

Debt has also trended up over the past decade. Short-term debt now stands at $2,587 and long-term debt is $8,282M. This is offset by only $244M in cash, equivalents, and marketable securities, which is not much. The leverage ratio is higher than desired at a little over 3X. Royal Caribbean can meet its obligations though, since interest coverage is about 5X.

The dividend safety metrics are not completely encouraging, despite the high yield. In my opinion one should be wary due to the lack of coverage from free cash flow and high leverage.

Royal Caribbean’s Competitive Advantages, Risks, and Moat

As one of the larger players in the cruising industry, one would think that Royal Caribbean would have a wide moat. But the industry is cyclical and there are numerous smaller players, which probably limits the moat. However, Royal Caribbean’s scale combined with high capital investment requirements probably gives a narrow moat. The main short-term risk for Royal Caribbean is the coronavirus impact. Over a longer-term the main risk is that economic slowdowns tend to be amplified due to the discretionary nature of cruising. In addition, there are about 89 new ships coming online in the next few years that could lead to overcapacity and lower prices.

Final Thoughts

Despite the high yield and the potential as an income stock or dividend growth stock, I am not a big fan of Royal Caribbean. The main issue for me is the poor dividend safety metric from the context of free cash flow.

Disclosure: None