Toronto-Dominion Bank (USA) (NYSE:TD), a.k.a. TD Bank, is Canada’s second largest financial institution, with over 14 million customers. TD Bank is one of the few financial institutions that are actually doing better than it was before the crisis of 2008-09 due to the good credit quality of its loan portfolio and good strategic acquisitions. In my opinion, TD Bank is one of the best ways to gain exposure to the financial sector in your portfolio without exposing yourself to unnecessary risks.

One of the most noteworthy aspects of TD Bank is its frequent acquisitions, which is what I think separates it from some of its Canadian peers. Among the notable moves is the company’s large stake in TD Ameritrade Holding Corp. (NYSE:AMTD), hence the name. The company bought a 32.5% stake in Ameritrade years ago and subsequently renamed it, then upped their stake to 44.5% in 2009.

Perhaps my favorite of TD Bank’s acquisitions is their $7.1 billion takeover of Commerce Bancorp in 2008. Most people have not heard of this bank, as it only operated in New Jersey and its immediate surrounding areas, but this acquisition greatly influenced TD Bank’s culture for the better. Having grown up in New Jersey and getting my first savings account with Commerce when I was 14, I have a very strong knowledge of the company.

Commerce referred to itself as “America’s Most Convenient Bank,” a slogan which TD still uses somewhat, and it truly was. Commerce refused to operate on traditional banker’s hours, and kept their drive-thru banking open until 8 or 9 most nights (midnight on Fridays) and stayed open on Saturdays and Sundays as well. As a result, the company grew from one branch in South Jersey to a $7 billion + company in about 20 years. TD Bank locations that used to be Commerce locations still keep these hours for the most part, making them the most popular banks in the area.

Most recently TD acquired the credit card portfolio of MBNA Canada, which is a subsidiary of Bank of America Corp (NYSE:BAC). Speaking of Bank of America, and the other U.S. financial institutions like it, they are still not worthy of long-term investment consideration. Until credit quality loosens significantly and more importantly, until the foreclosure backlogs are truly a thing of the past, these banks, while they may return to their former glory, are far too risky for long-term investors. Stick to the Canadian banks for now. If the American banks have any sense, they will take a lesson from TD Bank on how a loan portfolio should look.

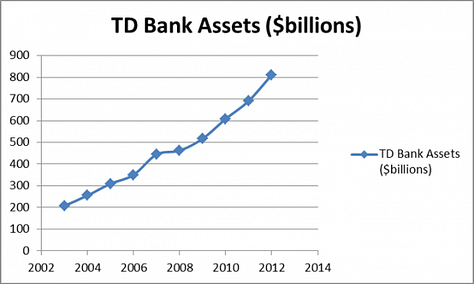

As a result of its convenient nature and responsible practices, TD Bank has thrived. As shown in the chart below, the amount of TD’s total assets has quadrupled in the last decade alone.

Shareholders have been handsomely rewarded as well. Since 2003, shares have risen from $20.50 to the current share price of around $82. The company also pays an excellent dividend of over 3.7%, one of the best among large banks, and has a nice history of raising it.

I wholeheartedly believe the trend above will continue, which makes the stock seem extremely cheap at the moment. TD Bank trades for just 12.2 times earnings, with an 11% projected forward growth rate. These numbers sound good enough, but looking at the history of TD’s performance and the chart above, these estimates sound pretty conservative indeed.

The article This Is The Bank That U.S. Banks Should Try To Be Like originally appeared on Fool.com and is written by Matthew Frankel.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.