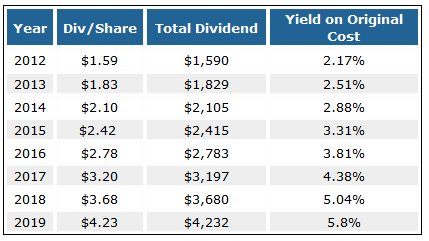

Consider the example of Wal-Mart Stores, Inc. (NYSE:WMT), which has been growing its dividend roughly 15% a year. Today, the stock pays a dividend of $1.59 a share and yields roughly 2%. But if the dividend continues to grow at 15% rate, then the yield (on the original investment) climbs to almost 4% by year five and reaches almost 6% by year seven — nearly triple the initial yield. (My example assumes 1,000shares purchased today for $73, a total initial investment of $73,000.)

The key to successful dividend-growth investing is finding stocks that have a high likelihood of continuously raising dividends over time. To uncover these steady growers, I ran a screen for stocks that have 1) accelerating rates of earnings and/or cash flow growth; 2) modest dividend payout, which leaves room for more growth; and 3) strong cash positions and little debt.

Here are three high-quality stocks that met my criteria. Since all three of these companies only recently began paying cash dividends, they may be flying under the radar of some income investors. All are worthy to join the ranks of stocks like Verizon Communications Inc. (NYSE:VZ) and Apple Inc. (NASDAQ:AAPL) as part of a new generation of dividend-growth stocks.

1. Amgen, Inc. (NASDAQ:AMGN)

Yield: 2%

Amgen is a pioneer in genetic engineering and has grown to become the world’s largest biotechnology company. Amgen launched the biotechnology industry’s first blockbuster medicines, including two of the most successful drugs in history — Epogen, for treating anemia, and Neupogen, which helps cancer patients receiving chemotherapy avoid infections. Other blockbuster drugs include Enbrel for rheumatoid arthritis, Prolia for osteoporosis and Sensipar, for complications common in patients with kidney disease.

Amgen has a potent new drug pipeline and may be first to market with a powerful new cholesterol-lowering medicine for patients who can’t take standard medicines such as Lipitor (marketed by Pfizer Inc. (NYSE:PFE).) Amgen’s new cholesterol drug has true blockbuster potential and addresses a $10-plus billion market. In addition, the company has new drugs for psoriasis, malignant melanoma, and gastric and ovarian cancer in its late-stage pipeline.

Based on the strength of its pipeline, analysts forecast 10% earnings growth for Amgen in each of the next five years, which is a big improvement from 6% yearly growth in the prior five. Amgen’s profit marginof almost 34% is the envy of the biotech industry. In addition, the company has a cash stockpile exceeding $19.4 billion, or $25 a share. Although Amgen isn’t debt-free, debt is manageable at 50% of capitalization and well covered by the company’s $5 billion annual cash flow.

Amgen initiated quarterly dividends at 28 cents a share in August 2011 and raised payout 29% in February 2012 to a quarterly rate of 36 cents a share ($1.44 annualized) yielding nearly 2%. With apayout ratio at just 24%, Amgen could readily support another big dividend hike.

2. Cisco Systems, Inc. (NASDAQ:CSCO)

Yield: 3%

Cisco, best known for its switches and other networking devices, has a 65% worldwide market share in Ethernet switches that crushes the next largest competitor — Hewlett-Packard Company (NYSE:HPQ), which has a 8% market share. The global market for switches and routers is continuing to grow at high single-digit rates and Cisco has been expanding its footprint in higher growth niches such as data-center virtualization and cloud computing. As a result, analysts expect Cisco’s earnings growth rate to rise from 7% in each of the past five years to 9%-10% in the next five.

Cisco has an attractive 22% operating margin, $49 billion of cash and only $16 billion of debt. The company began paying dividends in March 2011 at an annual rate of 24 cents per share, and doubled the dividend in 18 months to

a current rate of 56 cents per share. Even at the new higher rate, payout is conservative at 37% of 12-month earnings per share.

3. WellPoint, Inc. (NYSE:WLP)

Yield: 2%

Wellpoint provides health care coverage to 34 million patients in 14 states and is the second-largest U.S. health insurer, behind UnitedHealth Group Inc. (NYSE:UNH). The scope of its network gives Wellpoint impressive pricing power and the company’s position as the exclusive licensee of the trusted Blue Cross Blue Shield name makes it appealing to its target market of small businesses.

Wellpoint plans to acquire Amerigroup, the nation’s fifth largest health insurer, for $4.9 billion cash. This deal will bring the company 2 million new customers and add at least a $1 to earnings per share in the next two years. Wellpoint and United Healthcare should be major beneficiaries of Obamacare, which is set to provide the health insurance industry with 35 million new customers when it goes into effect in 2014.

Analysts forecast Wellpoint’s earnings growth rate will accelerate from 8% currently to 10% in the next five years. Even after paying cash for Amerigroup, Wellpoint should have plenty left. The company’s June quarter balance sheetshowed cash totaling $20.3 billion, or $62 a share, exceeding debt of only $11.9 billion. The company began paying an annual dividend of $1 per share in March 2011 and raised the amount 15% this year to an annual rate of $1.15 per share yielding 2%. Payout is just 16% of earnings and leaves plenty of cash flow for additional acquisitions, share repurchases and dividend growth.

Risks to Consider: Amgen’s patent on Neupogen expires in December 2013. This drug contributes roughly $5 billion of Amgen’s $16.8 billion of annualized sales so the company is heavily dependent on the success of its new drug pipeline. Cisco may be facing challenges to future growth from new technologies such as software defined networking (SDN) that allow companies to use lower-cost generic routers.

Action to Take –> All three of these companies enjoy leadership positions in their respective markets and each has solid growth prospects and strong fundamentals. Wellpoint is my top pick for conservative investors because the company has no sales outside the United States and hence no currency risk. For investors willing to accept a bit more risk in return for faster growth, Amgen and Cisco are also great choices.

This article was originally written by Lisa Springer, and posted on StreetAuthority.