What is more worrying is that the company’s guidance is way too high:

So for the fiscal fourth quarter of 2013, we expect revenue of approximately $110 million. Gross margin is expected to be at the high end of our target range of 56% to 58% given anticipated customer mix. We expect a loss in the quarter of approximately $5 million, and we expect diluted shares outstanding to be approximately 98 million shares.

For the full fiscal year 2013, we expect revenue of approximately $435 million We expect gross margin to be in the range of 59% to 60%. Operating margin is expected to be in the range of 7% to 8%, and we expect diluted shares outstanding to be approximately 109 million shares.

They are promising a 26% q/q increase in revenue. However, the prior quarters have seen much more conservative rates in sales growth. On an annual basis, the revenue growth of Fusion-IO, Inc. (NYSE:FIO) also shows a decreasing trend: 256.81% (2010-12), 445%, and 82%. Between 2011 and 2012, the growth rate of revenue decreased almost 80%. In this context, the 45%-50% guided for this year might prove to be a tall task.

The most recent figures clearly show that sales acceleration is not happening. Furthermore, as I will explain in detail in the next case, this is an industry with low barriers to entry, and competition is increasingly fierce. On top of that, the company only has two main customers: Apple Inc. (NASDAQ:AAPL) and Facebook Inc (NASDAQ:FB). The necessity for diversifying the customer base is urgent.

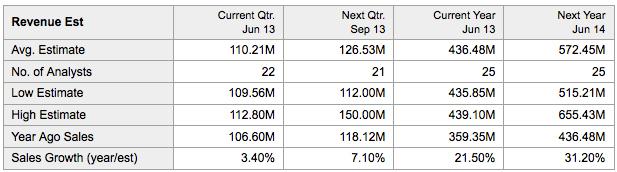

The unexpected high guidance caused the Street consensus estimate to increase. In the words of Brent Bracelin, from Pacific Crest Securities:

And then obviously on the guidance, $110 million, clearly above kind of where we’re at and where the Street was at, do you expect growth to come from the core customers?

According to Yahoo! Finance, the current average forecast for the next quarter revenue is very close to the official number given in the latest call: $110.21 million. Therefore, if Fusion-IO, Inc. (NYSE:FIO) fails to deliver this number in the next quarter (and unless they close some really big sales, most likely they will, even after taking into consideration that by acquiring NextGen they could obtain an additional $5 million -$10 million of sales), we could see a massive decrease in stock price.

At this point, you might be wondering what is causing the decrease in revenue growth. There is fierce competition!

This could be hard to believe. After all, at first glance, the business of Fusion-io looks unique and they were first-movers, once upon a time. The situation is completely different now. More and more competitors are joining the game.

One example is EMC Corporation (NYSE:EMC). Historically, EMC has occupied a leading position in the network storage industry. However, by leveraging its existing assets, the firm is also active in launching new products and entering into different market segments. An example is EMC’s PCIe flash card, VFCache, which can be deployed in the server to “dramatically improve application performance by reducing latency and accelerating throughput.”

According to EMC Corporation (NYSE:EMC), its new VFCache may be faster than Fusion-io alternatives, because VFCache handles flash management and wear leveling, while Fusion-io cards offload this to the server CPU. Fusion-io has refuted these claims, but only time will tell which option will prevail. However, having a big corporation like EMC as a competitor could damage Fusion-io’s margins by limiting its pricing power.

Another example is LSI Corp (NASDAQ:LSI). Since 2010, the company has been aggressively marketing its flash storage products, making some impressive sales in the process. Furthermore, LSI acquired SandForce in January 2012 to further strengthen its storage PCIe flash adapter product portfolio. Now, LSI offers both custom and standard flash storage processors for ultrabook, notebook, enterprise SSD, and flash solutions.

It seems that LSI Corp (NASDAQ:LSI) has no plans to give up its position in this market, and a new generation of SandForce products could give LSI the leading position going forward. Furthermore, LSI goes beyond PCIe accelerator solutions: it can provide integrated solutions to companies that involve both networking and storage alternatives.

Coming soon

The Bear Case For Fusion-Io (Part 2): 2 bear cases and 1 variant view.

Adrian Campos has no position in any stocks mentioned. The Motley Fool owns shares of EMC. Adrian is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

The article The Bear Case for Fusion-io: Part 1 originally appeared on Fool.com and is written by Adrian Campos.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.