In a clever and useful analysis, Ronen Israel, Kristoffer Laursen, and Scott Richardson of AQR use the residual income approach to break down how the value of a company’s stock depends on three components: its book value, the value of its predictable earnings, and the value of its speculative earnings. The first component, the book value, can be read off the balance sheet. The second component, the value of predictable earnings, is based on the assumption that the company meets analyst forecasts for the current year and the following year. In all future years beyond year two, the earnings are assumed to be equal to year two earnings. The final component, the speculative value, equals everything else. The speculative value is calculated by starting with the stock price and subtracting the book value and the value of predictable earnings. The speculative value incorporates all the growth in earnings that the market expects beyond the first two years. To summarize,

Stock price = Book value + Predictable earnings value + Speculative value.

Breaking Down Book Value

To illustrate the breakdown, the AQR authors use the examples of Starbucks (SBUX) and Chipotle (CMG). At the time of their calculation, the share price of Starbucks was $87.92. The authors show that this breaks down into a book value of ($5.26) per share – the book value is negative because the large number of buybacks – plus a predictable earnings value of $84.28, plus a speculative value $8.90. In comparison, Chipotle’s stock price of $837.11 breaks down into a book value of $52.10, a predictable earning value of $327.85, and a speculative value of $457.22.

What we were interested in at Cornell Capital Group was how the sharp run-up in stock prices that began on March 19, 2020 was related to speculative value. Did the market favor companies with predictable earnings over those with high speculative value or vice-versa? To answer that question, we started with all US and Canadian listed stocks with market capitalizations over $30 billion (as of May 11th, 2020) that had available earnings estimates. Our final sample consists of 204 companies.

Speculative Earnings: Tesla vs General Motors

Using the AQR model, we breakdown the share price of each sample company into the three components, book value, predictable earnings value, and speculative earnings value, each expressed as a percent of the stock price. It is interesting to note that the value of the speculative component ranges for a high of 167% for Uber (due to forecast losses for this year and next) to a low of -184% for GM (which has a particularly high book value and high predictable earnings value compared to the current stock price.) A comparison between General Motors (GM) and Tesla (TSLA), which has a speculative value of 85%, is particularly provocative. The market places a huge value on Tesla’s speculative earnings while assuming that GM’s are markedly negative.

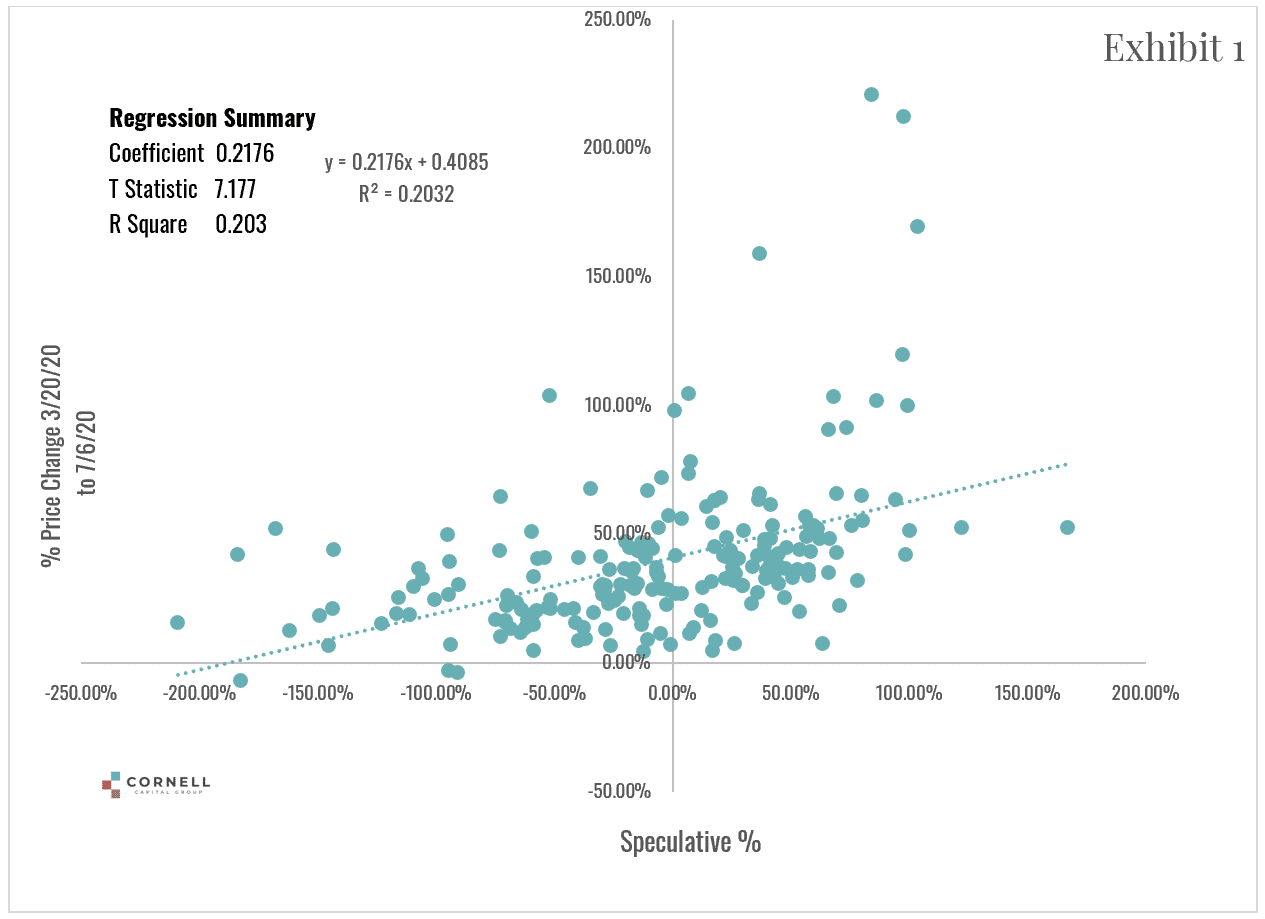

Given the data, the question we asked was whether the extent of the Covid stock price rebound was related to a company’s speculative value percentage. To answer that question, we ran a regression of each company’s total stock return between March 20, 2020 and July 6, 2020 on the company’s percentage speculative value. The regression results, along with a scatter plot, are reported in Exhibit 1. The t-statistic and R2 are also included. The results show that the percentage of speculative value is a highly significant explanatory variable for how much a stock ran up during the recovery that began on March 20, 2020. The higher the fraction of speculative value the greater the price increase.

![]()

Adding Beta To The Regression

It is possible that the regression result may simply be due to the fact that companies with a high fraction of speculative value are more sensitive to market moves. To test that hypothesis, we added beta to the regression. It turns out that adding beta has almost no impact on the regression results. The coefficient of the speculative percentage remains largely unchanged and is still highly significant, while beta adds almost no explanatory power to the regression.

Given the highly significant relation between the fraction of speculative value and stock changes during the run up, we thought it would is interesting to check if a similar relation held during the stock price collapse from mid-February to March 20. To investigate, we collected data on the stock returns for our sample companies over the period from February 19, 2020 to March 20, 2020 during which time the S&P 500 dropped 32.38% and reran our regressions.

The results reported in Exhibit 2 are markedly different from those in Exhibit 1. Instead of being significantly positive, the coefficient for the percentage of speculative value is almost identically zero so that the regression line is virtually flat and the R2 is essentially zero. The lack of a relationship can also be seen by looking at the scatter plot which is just an amorphous cloud. The conclusion is that during the market decline there was no relation between the extent of drop and the percent of speculative value. Finally, we again added beta to see if it affected the regression results. Once again adding beta had no impact.

While it is tempting to speculate as to why the market treated stocks with a high fraction of speculative earnings so much differently during the decline than during subsequent rebound, we leave that exercise to our readers.