Valued at $14.75 billion, L Brands Inc (NYSE:LTD)‘ robust and strong business model possesses a TTM profit margin of 7.20%. Recently, L Brands announced an increase in the company’s quarterly dividend payouts from $0.25 to $0.30, demonstrating the financial strength of the company.

So with the stock coming within dollars of all-time highs, is L Brands a tremendous play on the specialty retail industry, or should investors wait for a considerable pullback?

Strengths

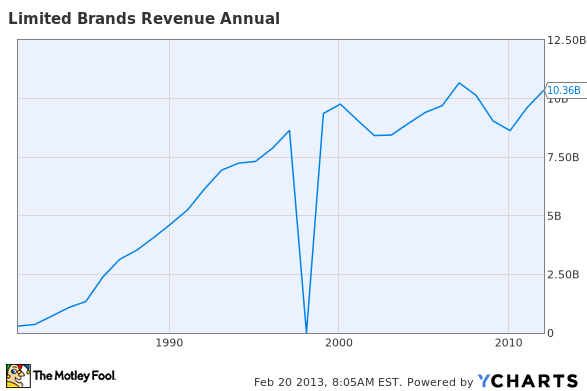

Historic revenue growth:

In 2003, L Brands Inc (NYSE:LTD) reported revenue of $8.44 billion; in 2012, the company announced revenue of $10.36 billion, representing year over year annual growth of 2.30%, a solid trend which is highly anticipated to sustain into the future with projections placing 2017 revenue at $12.68 billion (this growth has been a result of consistent product innovation and strong performance across all segments)

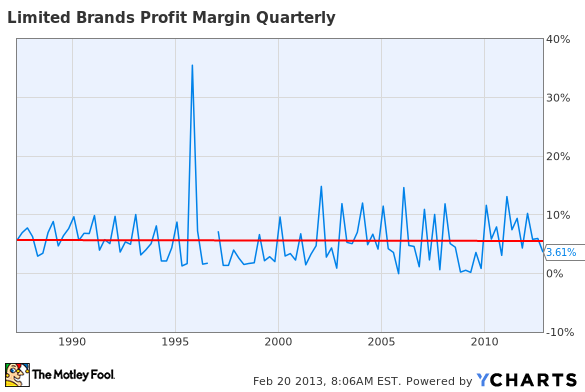

Steady profit margin:

Since 1990, L Brands Inc (NYSE:LTD)’ quarterly profit margin has gyrated around the current 3.61% level, representing a company that has performed on a consistent basis

Institutional vote of confidence:

73.68% of shares outstanding are held by institutional investors, displaying the confidence some of the largest investors in the world have in the company and its future

Strong cash flow position:

In 2012, L Brands generated $1.24 billion in cash flow, representing the financial strength of the company; this cash flow is able to support a 2.70% dividend which has a long history of growth

Reasonable valuation:

At the moment, the company carries a price to earnings ratio of 20.19 and a price to sales ratio of 1.41, both of which represent a company trading with a reasonable valuation

Weaknesses

Net debt:

The $547 million of cash and cash equivalents the company possesses on its balance sheets is outweighed by L’s $7 billion of debt, resulting in a net debt of roughly $6.5 billion, or $22.60 per share, a major financial weakness of the company

Opportunities

International expansion:

In 2011, the company launched 90 new international stores, bringing their international store count to more than 680 stores in nearly 40 countries, with $1 billion in retail sales; further aggressive international expansion is projected and provides an opportunity for the company to fuel overall growth

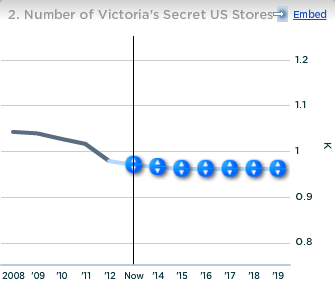

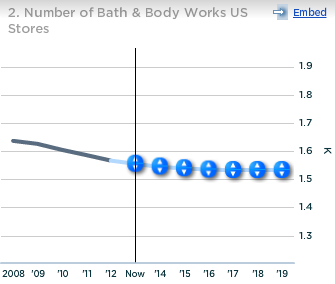

Domestically increasing store count:

In the United States, the number of Victoria’s Secret and Bath & Body stores has decreased from 1,040 K in 2008 to 970 currently, and from 1,640 in 2008 to 1,560 currently, respectively; however as economic conditions improve increasing the store count is a real opportunity

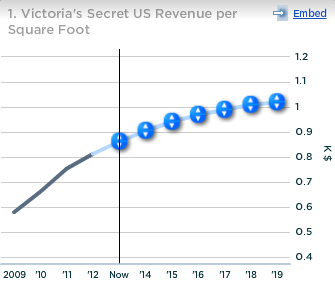

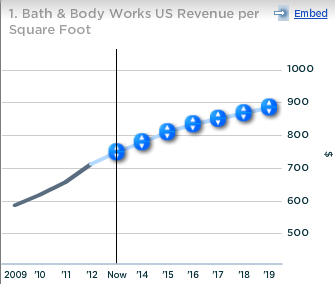

Streamlining revenue per square foot:

While over the past years total store count has been decreasing, revenue per square foot has been rising moderately (Victoria’s Secret 2009- $580 Currently- $860 Bath & Body 2009- $587 Currently- $749); with further growth in these statistics projected

Threats

Rising material prices:

L utilizes several distinct materials to compose their products, and any rise in the price of the materials the company uses could squeeze margins

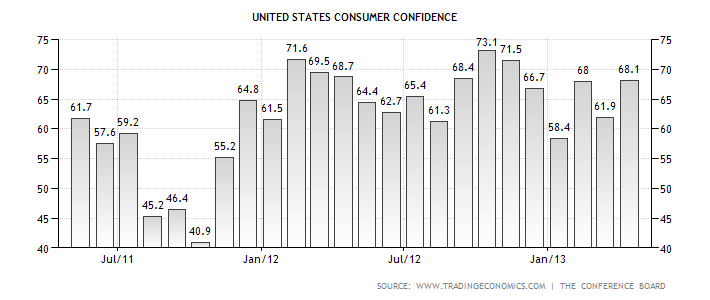

Falter in consumer confidence:

When consumer confidence prospers, customers have more conviction to purchase luxuries such as those sold at L Brands Inc (NYSE:LTD) stores, however any falter in consumer confidence could threaten sales

Competitors

Major competitors include Ann Inc (NYSE:ANN), Chico’s FAS, Inc. (NYSE:CHS), Ascena Retail Group Inc (NASDAQ:ASNA), and The Wet Seal, Inc. (NASDAQ:WTSL). All of these companies operate in the specialty retail industry and target women as one of their main demographics, as well as compete with L Brands.

Ann Inc (NYSE:ANN) is valued at $1.39 billion, does not pay out a dividend, and carries a price to earnings ratio of 14.20. Ann’s core business consists of the brands of Ann Taylor and LOFT, which target women in the apparel, shoes, and accessories industries. Ann Inc (NYSE:ANN)’s TTM profit margin has held steady around 4% since 2011, and is currently sitting at 4.32%, with expectations placing the profit margin at 4.9% by 2018. Mid-single digit rate growth is anticipated for revenue fueled by store expansion, however this growth is contingent on innovative product offerings. Ann does not pose a major threat to L Brands Inc (NYSE:LTD) as they compete mainly in different sub-sectors of the industry.

Chico’s FAS, Inc. (NYSE:CHS) is valued at $3.00 billion, pays out a dividend yielding 1.20%, and carries a price to earnings ratio of 17.08. High-single digit growth is projected in the revenue department, with the same projected in the earnings statistic. The company’s TTM profit margin has recovered from its 2008-2009 slump and is currently a strong 6.98%. Year to date, Chico’s FAS, Inc. (NYSE:CHS) is slightly down, despite no majorly negative news.

Ascena Retail Group Inc (NASDAQ:ASNA) is valued at $2.97 billion, does not pay out a dividend, and carries a price to earnings ratio of 20.99. The company’s business model has experienced a substantial contraction as the company’s profit margin has decreased from 6% to the current 3.45% level, which has caused a drop in earnings, however this trend is projected to reverse by 2014. Revenue is expected to grow nearly 50% from 2012 to 2013, with a mid-single growth rate anticipated for years after 2013.

The Wet Seal, Inc. (NASDAQ:WTSL) is valued at $303.13 million, does not pay out a dividend, and carries a negative price to earnings ratio. The Wet Seal, Inc. (NASDAQ:WTSL) is a much smaller and volatile company than other mentioned in this article, and is one that has experienced a history of inconsistent earnings. Because of this, the company trades with a cheap valuation (price to sales ratio of 0.52 and a price to book ratio of 2.36).

Foolish bottom line

Financially, the company is strong disregarding its rather substantial debt position. L Brands possesses a track record of consistent revenue growth, a growing dividend, and a reasonable valuation. The company’s weaknesses include a major segment of their business being unprofitable and the gradual decay of the company’s assets. Looking forward, the company is likely to drive fast-paced growth from its international segment while seeing slower-paced growth domestically. All in all, L Brands Inc (NYSE:LTD) is a cyclical company, and should prosper as long as the economic picture improves, and at least in the short-term will provide attractive returns.

The article A Seductive Company Trouncing The Overall Market originally appeared on Fool.com and is written by Ryan Guenette.

Ryan Guenette has no position in any stocks mentioned. The Motley Fool recommends Ascena Retail Group. Ryan is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.