Over the last few years, investors have piled into high-quality dividend stocks in search of yield. With bonds paying abysmal yields, dividend stocks became an attractive alternative. This popularity pushed prices up and yields down, and many dividend stocks became overvalued. Although many believe that high-quality dividend stocks are safe, the price which you pay matters greatly.

Now, with treasury yields rising, many dividend stocks have been hit hard, falling considerably in price over a short period of time. A disaster? On the contrary, this is an opportunity. When I was assembling my Ultimate Dividend Growth Portfolio, which you can track here, I was forced to exclude many standard dividend stocks because their prices were just too high. But with prices coming down, these stocks may become attractive again.

A standard dividend stock

Johnson & Johnson (NYSE:JNJ), the diversified health care giant, is a common holding in countless retirement portfolios. A long history, steady growth on all fronts, and consistent dividend increases round out this behemoth of a company. Since the beginning of 2013, the stock has been on a tear:

After reaching a high of about $89, the stock has fallen back to $84 in just a few days. Is $84 per share cheap enough? Or does the price need to fall further to justify a position in Johnson & Johnson (NYSE:JNJ)?

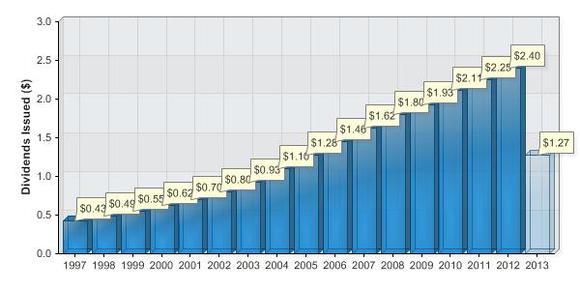

Johnson & Johnson (NYSE:JNJ) hiked its quarterly dividend by 8.2% in May, and this new payment puts the current projected yield at 3.13%. At the high of $89 per share, the yield was a lower 2.97%, so the yield is a little more attractive now. Since 1997, it has increased its dividend at an annualized rate of about 12.1%.

This rate has slowed, as the annualized rate of growth since 2008 is closer to 10% and the most recent hike was only 8.2%. So, it’s unlikely that dividend growth going forward will match the last decade.

Since dividends are paid out of the free cash flow, it makes sense to see how the payout ratio with respect to the FCF has changed over the years. In 2003, the payout ratio was just 33.5%. By 2012, the payout ratio had risen to 54.2%, and the recently hiked dividend pushes that number close to 60%. What this means is that much of the dividend growth of the last decade was a result of an expanding payout ratio.

The next decade, then, will feature far slower dividend growth than the previous one. Earnings growth will be the main driver, so I don’t expect the dividend to grow much faster than 8% per year. Based on this assumption, what’s the maximum you should pay for a share of Johnson & Johnson (NYSE:JNJ)?

If the dividend grows by 8% per year for the next decade, the most you should pay is a little under $81 per share. So the stock needs to fall at least another 4% or so before it becomes a fairly valued dividend stock. I’d like to see it fall into the 70’s before considering it for The Ultimate Dividend Growth Portfolio, as there are still plenty of dividend stocks which are cheap in comparison. But in terms of the company itself, you can’t do much better than Johnson & Johnson (NYSE:JNJ).

A similar story

Another standard dividend stock, The Procter & Gamble Company (NYSE:PG), is in a similar boat as Johnson & Johnson (NYSE:JNJ). The stock has a yield of 3.13% after a recent 7% dividend hike, well below the historical dividend growth rate. The annualized dividend growth rate over the past decade was 11.2%, and 10.2% over the past five years. The payout ratio with respect to free cash flow has risen from 31.% in 2003 to 67.5% in 2012.