General Electric Company (NYSE:GE)‘s stock price surged a whopping 140% in the last 2 years! That in itself is huge news for investors. Congrats to the people who bought in at the right time, but the real question is where the price is heading from here.

If you are curious what the analysts have to say, let us look at the table below. While most analysts out there tout General Electric Company (NYSE:GE) as a strong buy, earnings are expected to strengthen going forward.

| DESCRIPTION | LAST 5 YRS | FY 2013 | FY 2014 | NEXT 5 YRS | 11 P/E |

| Company | -5.30% | +9.60% | +10.30% | +9.70% | 14.10 |

| Industry | 0.00% | +4.30% | +18.00% | +10.20% | 14.90 |

| S&P 500 | +3.20% | +5.80% | +5.50% | NA | 15.30 |

In the last five years, earnings have actually gone down while the S&P 500 index has gone up. In the next couple of years, the earnings growth rate will likely make up for that (or, that is what the analysts expect).

To verify the analysts’ recommendation, let us dig deeper into the company financials.

Qualitative Analysis

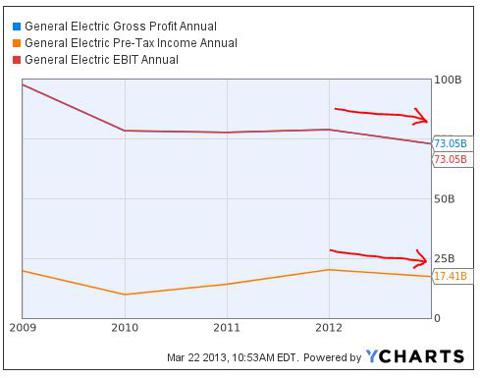

Let us look at the last five years’ EPS summary below. It is good to see that EPS has shown continuous growth in the last five years, which means that the company is doing well when it comes to the bottom line.

| DATE | SALES | EBIT | DEPRECIATION | TOTAL NET INCOME | EPS |

| 12/12 | 147.36 billion | 17.41 billion | 10.96 billion | 14.68 billion | 1.39 |

| 12/11 | 147.29 billion | 20.26 billion | 10.93 billion | 14.23 billion | 1.24 |

| 12/10 | 149.57 billion | 14.19 billion | 11.54 billion | 12.61 billion | 1.15 |

| 12/09 | 154.44 billion | 9.86 billion | 12.70 billion | 10.81 billion | 0.99 |

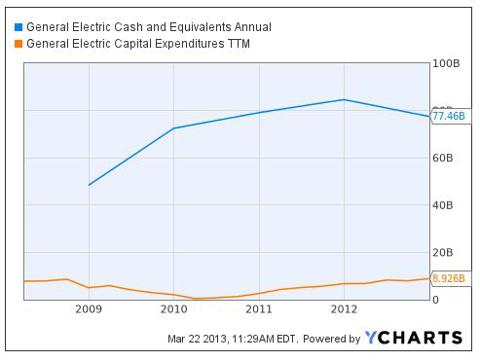

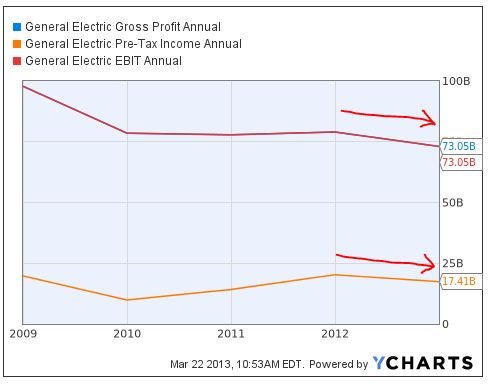

And this is in contrast with the increasing capex being incurred by the company. When the focus is more on the energy and aviation side, it is natural that the company has to incur capex regularly. But the effect on the profitability margins has not been satisfactory to be honest.

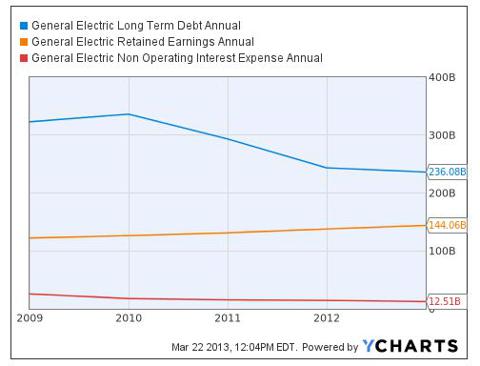

GE’s long-term debt has gone down over the last couple of years, resulting in a decrease in the interest expense nonetheless. And the strain on the working capital has been cushioned with higher retained earnings since 2010. But the question is whether the high capex ratio, with tightened capital availability and declining margins, will not negatively affect shareholder’s equity. In other words, we need to see a better asset utilization factor, not to bother about the high capital expenditures and falling debt.

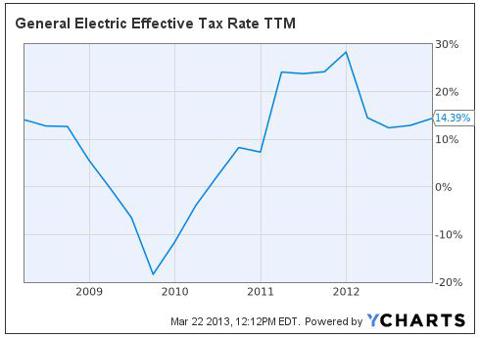

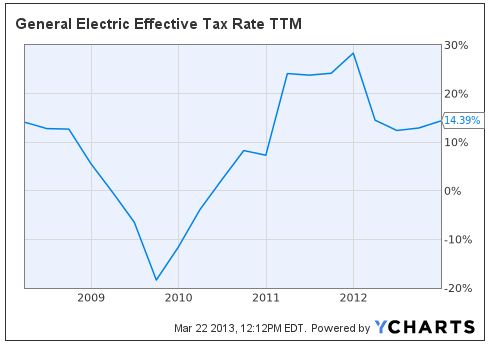

In addition to that, the tax rate is expected to rise sharply in the next couple of years. That might put additional burden on the bottom line as well.

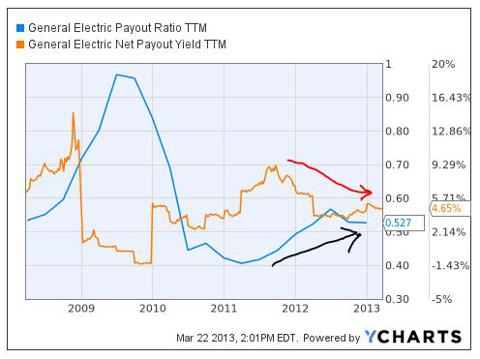

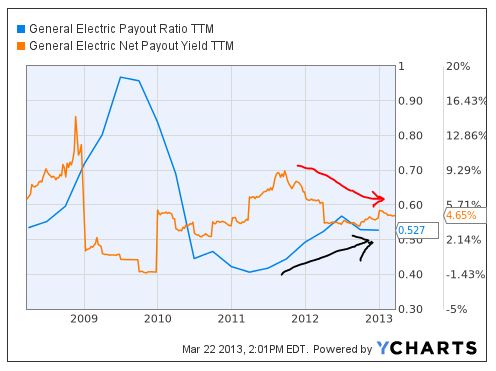

Moreover, if you look at the dividend yield graph below, it seems it has fallen over the last couple of years, even when the dividend payout ratio has gone up. That is just the effect of declining EPS over time. The question is what happens if the EPS further falls or stays stagnant at the current level for the next one year or so. I am apprehensive about a fall in stock price if that happens.

In other words, we cannot say that the company is going to crumble down, but more focus to asset utilization should be given.

Competitive Analysis

| Companies | P/E (TTM) | P/S | PEG | Debt/Equity | Quick Ratio | ROA % | Operating Margin % | Net Margin % |

| General Electric Company (NYSE:GE) | 18.08 | 1.65 | 1.23 | 1.84 | 2.85 | 2.31 | 10.9 | 9.26 |

| United Technologies Corporation (NYSE:UTX) | 16.5 | 1.47 | 1.12 | 0.8 | 0.84 | 6.57 | 9.04 | 8.89 |

| Siemens AG (ADR) (NYSE:SI) | 17.75 | 0.93 | 0.23 | 0.55 | 0.83 | 4.58 | 6.29 | 5.41 |

| Koninklijke Philips Electronics NV (ADR) (NYSE:PHG) | 95.9 | 0.86 | 16.24 | 0.33 | 0.91 | 3.96 | 4.82 | 0.96 |

| Citigroup Inc. (NYSE:C) | 18.53 | 2.32 | 0.82 | 1.27 | 1.01 | 0.62 | 15.01 | 9.51 |

| The Boeing Company (NYSE:BA) | 16.61 | 0.78 | 0.98 | 1.5 | 0.43 | 4.57 | 4.68 | 4.77 |

Valuation – While Koninklijke Philips Electronics NV (ADR) (NYSE:PHG)‘ PE ratio is too high to even consider, which is also the reason why Philips’ stock price fell by over 12% in the last 1 month, GE’s P/E ratio is more in line with the other competitors such as Siemens AG (ADR) (NYSE:SI). Moreover, with a 3.7% drop in healthcare sales and 2% in lighting revenue (two segments that generate 80% of Philips’ revenue), Philips’ first quarter of 2013 is already shaky, compared to General Electric Company (NYSE:GE). Although GE investors seem to be putting higher value on GE’s revenue, when compared with that of The Boeing Company (NYSE:BA), I would not say it is ‘off limits.’ With the recent Federal Aviation Administration (FAA) probe on the Boeing 737s and 787s, it is natural for Boeing investors to be rather wary of the future sales. It must be noted though that with the current P/E valuation, a lower PEG would have been better.

Leverage – Although GE’s debt/equity ratio at 1.84 is pretty higher than 0.8 of United Technologies, 0.55 of Siemens and 0.33 of Philips, the high quick ratio of 2.85 more than compensates for it. I would say that the company is still in a strong financial position.

Performance – Asset utilization looks pretty weak with ROA at 2.31%. Even though the profitability margins look good when compared to the rest, except Citigroup Inc. (NYSE:C), the couple of quarters ahead would be highly crucial in deciding whether the company is still profitable or not.

Conclusion

General Electric Company (NYSE:GE) shows growth potential. I would definitely not reject the popular analysts’ estimates. The strong fundamentals, the competitive edge and the global expansion of the company definitely promise future growth. Having said that, there is a strong need for the company to justify its capital expenditures. In other words, asset utilization is still an important yet undermined factor for GE. The next couple of quarters ahead will hopefully prove me wrong. For now, I am neutral about the company.

Ron Chatterjee has no position in any stocks mentioned. The Motley Fool owns shares of Citigroup Inc and General Electric Company.

The article I’m Not Too Positive About General Electric originally appeared on Fool.com and is written by Ron Chatterjee.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}