Every investor can appreciate a stock that consistently beats the Street without getting ahead of its fundamentals and risking a meltdown. The best stocks offer sustainable market-beating gains, with improving financial metrics that support strong price growth. Let’s take a look at what Baidu.com, Inc. (ADR) (NASDAQ:BIDU)‘s recent results tell us about its potential for future gains.

What the numbers tell you

The graphs you’re about to see tell Baidu’s story, and we’ll be grading the quality of that story in several ways.

Growth is important on both top and bottom lines, and an improving profit margin is a great sign that a company’s become more efficient over time. Since profits may not always reported at a steady rate, we’ll also look at how much Baidu’s free cash flow has grown in comparison to its net income.

A company that generates more earnings per share over time, regardless of the number of shares outstanding, is heading in the right direction. If Baidu’s share price has kept pace with its earnings growth, that’s another good sign that its stock can move higher.

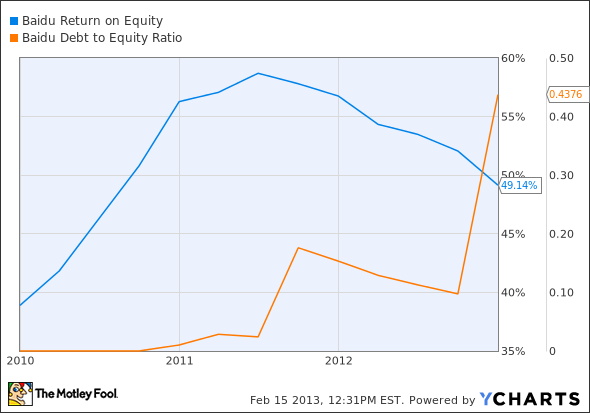

Is Baidu managing its resources well? A company’s return on equity should be improving, and its debt-to-equity ratio declining, if it’s to earn our approval.

By the numbers

Now, let’s take a look at Baidu’s key statistics:

BIDU Total Return Price data by YCharts.

| Criteria | 3-Year* Change | Grade |

|---|---|---|

| Revenue growth > 30% | 444.8% | Pass |

| Improving profit margin | 30% | Pass |

| Free cash flow growth > Net income growth | 468.3% vs. 664.4% | Fail |

| Improving EPS | 659.6% | Pass |

| Stock growth (+ 15%) < EPS growth | 128.7% vs. 659.6% | Pass |

Sources: YCharts and Morningstar *Period begins at end of Q4 2009.

BIDU Return on Equity data by YCharts.

| Criteria | 3-Year* Change | Grade |

|---|---|---|

| Improving return on equity | 26.4% | Pass |

| Declining debt to equity | 4,190% | Fail |

Source: YCharts. *Period begins at end of Q4 2009.

How we got here and where we’re going

The only real cause for concern here is Baidu’s rising debt levels. Five out of seven passing grades somewhat underrates the impressive growth Baidu’s posted over the past three years. Its other miss, on free cash flow against net income, could still be reversed the next time we examine it. Either way, those growth rates are nothing to sneeze at. But can Baidu maintain them?

Last month, in a round-table discussion with my fellow fools Travis Hoium and Sean Williams, I argued that it could. Baidu has two things indisputably on its side: a rapidly connecting populace with rapidly growing earnings power, and a dominant position from which to serve them. We often compare Baidu to Google Inc (NASDAQ:GOOG) — and for good reason. Google is the model for search and Internet dominance that Baidu has thus far been attempting to follow, and my conservative estimates found that Baidu could easily enjoy a 155% upside if its trajectory continues to resemble Google’s.

However, the market doesn’t seem to agree with this sort of optimism, at least not in the near term. Baidu’s most recent quarter, which was reported a month after our round table, showed a company with growing pains, which is now starting to see revenue grow faster than net income as its costs of doing business creep higher. Projecting a sequential decline in revenue didn’t help, either.