U.S. retail same-store sales exceeded expectations in January, led by Macy’s, Inc. (NYSE:M), Kohl’s Corporation (NYSE:KSS), and Nordstrom, Inc. (NYSE:JWN). We need more economic data to understand whether this was spurred by larger than anticipated promotions or if U.S. shoppers simply spent more money than analysts predicted. But I think this could be a long-term trend driven by our recovering economy, and I’m inclined to believe that Nordstrom is best-positioned to capitalize on this trend.

Healthy Wallets

Despite a surprising decrease in U.S. GDP last quarter, the overall health of the U.S. consumer continues to improve. Real disposable income has recovered to pre-financial crisis levels. Unemployment is now below 8% as the slow march back to normal levels moves forward. And the U.S. housing market recovery is in full bloom as home prices are up in 88% of metropolitan areas and the year-over-year price growth rate is at its highest level since 2006.

All of these signs point to a healthy economy and a healthy consumer. As we move forward consumer spending will not only continue to increase, but also shift from value retail like Wal-Mart Stores, Inc. (NYSE:WMT) and Target Corporation (NYSE:TGT) to shopping malls and department stores like Kohl’s, Macy’s, and Nordstrom.

Nordstrom Inc. (JWN)’s Advantages

Why do I think Nordstrom is better positioned than Macy’s and Kohl’s? First, Nordstrom is synonymous with legendary customer service. This is critical for department stores because they have to fight off competition from both value retailers and online retailers. Genuinely great in-store customer service is the differentiator that will draw certain consumers away from Target, and even from online retail, as people become able to afford more frequent shopping trips. No one does this better than Nordstrom.

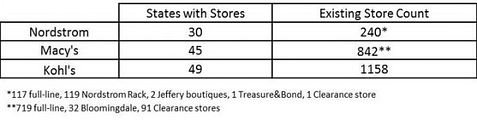

Nordstrom also has more room to expand and open new stores in the U.S. compared to Kohl’s and Macy’s. Nordstrom is currently adding a single full-line store this year, along with 15 Nordstrom Rack stores. They also have aspirations of doubling their number of Nordstrom Rack stores by the end of 2016.

Compare that to Macy’s, which plans to open just three stores this year. Now, I don’t expect Nordstrom to unveil any sort of aggressive plan to quadruple full-line stores in the next five years. But for long-term investors like me, I think it’s worth noting that Nordstrom still has abundant opportunities to expand its store operations into attractive markets.

Finally, I think Nordstrom has an advantage in the boardroom. It’s incredibly difficult to assess corporate leadership as a small-time individual investor, so I wouldn’t invest solely on this perceived advantage. But a quick search in the salary.com Executive Pay Wizard shows that president Blake Nordstrom’s total compensation is about 4 times less than Macy’s CEO/president Terry Lundgren and 3 times less than Kohl’s chairman/president/CEO Kevin Mansell.

I don’t begrudge Mr. Lundgren or Mr. Mansell for accumulating wealth, and some of the difference here could be explained by the difference in the size of operations. But Nordstrom’s family legacy within the company is an extra incentive to do what’s best for the company with a long-term view in mind.

Foolish Bottom Line

Department stores should grow stronger as the health of the U.S. economy continues to improve. Though economic health is far from guaranteed, the future looks bright when taking a long-term view. Nordstrom’s legendary customer service, store expansion opportunities, and strong family leadership could add up to healthy investor returns for many years to come.

The article Healthy Wallets, Healthy Returns originally appeared on Fool.com and is written by Michael Cash.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.