When looking at a stock it is always tempting to take an initial peek at its share price graph to make a quick and easy assessment. In the case of Pall Corporation (NYSE:PLL) and its impressive looking chart, it would be easy to conclude that things are going great, but the reality is that it has been a challenging environment for the industrial sector.

![]()

In summary, there are some changes afoot, and investors would be best advised to be selective with investments within the sector.

Structural changes

I have two main observations here.

The first is that it has been a mediocre Q1 reporting season for the industrial sector outside of the automotive and aerospace sectors. This has been a recurring theme in this reporting season whether from a large industrial bellwether like General Electric Company (NYSE:GE) or a smaller niche player like AMETEK, Inc. (NYSE:AME). I’ve discussed these companies’ results in articles linked here and here.

The second is that the nature and quantum of growth in China is shifting. We all know that China is taking up an increased percentage of global manufacturing but we also know that its reliance on export led growth cannot continue indefinitely. Europe’s growth is anemic, and the long term prospects for US growth look hampered given its public deficits. Moreover, the Chinese government knows this and is gradually trying to shift the economy towards domestic consumption. And China matters for the global players. Even a cursory look at Alcoa Inc (NYSE:AA)’s results will demonstrate the emphasis it is placing on growth from China. Many of us that think that China has the reserves in order to ‘buy’ its way to 7-8% growth but we must recognize that its stimulus plans are likely to be different this time around.

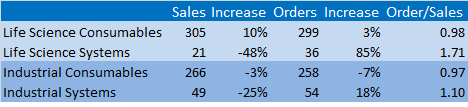

What did all this mean for Pall Corp?

It was a tricky Q3 for Pall Corporation (NYSE:PLL), and the repercussions of these two changes are being seen in its numbers. Total sales fell $18 million to $640 million and investors can take little solace in the fact that excluding currency effects its sales would have been flat. On the positive side pro forma EPS for the nine months was up 11% to $2.15 with some notable cost savings being implemented while higher margin consumables increased as a part of the mix. Naturally this meant that margins went up. This is good but recall that future consumables sales rely on the system sales being made now.

In order not to cover old ground I have a primer article on Pall Corporation (NYSE:PLL) linked here. In fact its growth prospects have progressively weakened since that article. The latest numbers imply that sales are still weakening (particularly within industrial), but at least system orders are looking relatively better at the moment.

Digging deeper into the numbers shows that Life Science sales (67% bio-pharmaceuticals,16.3% food and beverage and 16.7% medical) are doing okay with good growth from bio-pharmaceuticals (pharma is still investing) of 9% offsetting a 21% decline in food and beverage sales.

Turning to Industrial sales (59.4% process technologies, 20% aerospace and 20.6% microelectronics) it’s clear that there are some issues here. AMETEK, Inc. (NYSE:AME) recently spoke to strong performance in its aerospace markets and it’s been a strong reporting season for aerospace companies. On the other hand it mentioned some softer than expected numbers in its process industries as well as softness caused by the heavy truck and trailer market. Indeed, this is exactly the sort of thing that Alcoa Inc (NYSE:AA)’s results had presaged when it forecast deteriorating conditions in its heavy truck markets.

Pall Corporation (NYSE:PLL)’s process technologies sales declined 13%, and it was no surprise to see its microelectronics sales down 14% as well. The one bright spot was–you guessed it–in aerospace as sales rose 25%; but as it only makes up 9.8% of total sales, it is not enough to make a significant difference.

The conclusions are clear, outside of automotive, aerospace and parts of healthcare, the industrial sector is doing great and investors should be minded to consider factoring this into their decision making.

China?

Similarly with regards to the regional breakdown, Pall Corporation (NYSE:PLL) stated that its Asian sales were down 11% due to weakening in its industrial markets in China and ‘mature Asia.’ Obviously part of this will relate to tougher conditions within microelectronics and you only have to look at what Intel said to confirm this. However, Pall’s management stated that conditions were changing in China, and I think this is self evidently true from most commentary on the country. Aerospace and automotive should do fine because they are strongly related to the Asian consumer (car buying and air passenger traffic), but some of the major infrastructural markets may see a slowdown.

For companies like Alcoa Inc (NYSE:AA) or General Electric Company (NYSE:GE) this may cause some problems, but it may cause opportunity as well. Alcoa does have significant exposure to automotive and aerospace but any weakness in China will hit its growth prospects quite hard.