![]()

Earnings Review

Group revenues fell slightly (-3% YoY) to S$18.183 billion ($14.55 billion USD) for the quarter ending March 31, 2013. While the Group’s FY13 operational EBITDA margin grew for the first time in eight years, to 28.6% (29.3% ex-digital business), net profit after tax fell 33% YoY to S$868 million ($694.4 million USD) as foreign exchange fluctuations, spectrum investment and digital initiatives in FY13 cut into the bottom line. The S$0.10 per share final dividend was higher than expectations, pushing FY2012 total payouts to S$0.168 per share, implying a 74% payout of free cash flow, compared to S$0.158 per share in FY2012, a 69% payout. This works out to a current yield of 4.5%, which is attractive compared to the Singapore market as well as regional telcos. OCBC cut its rating on the sector to neutral from overweight on May 21, and Singapore Telecom (NASDAQOTH:SGAPY.PK)’s shares declined 2% on the news. It has corrected recently off its highs.

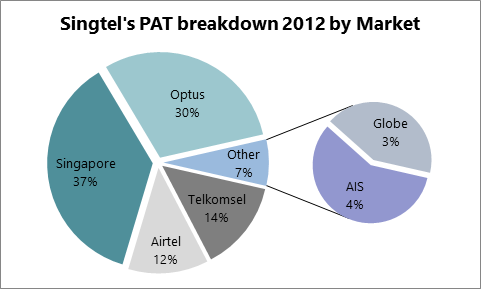

The Group leveraged its combined procurement, network and IT capabilities across geographies, delivering impressive efficiencies, and its investments in regional carriers across Southeast Asia are where much of the company’s earnings came from. Earnings from Indonesia’s Telkomsel (SingTel has a 35% stake), Thailand’s Advanced Info Services (a 23.32% stake) and the Philippines Globe Telecom (a 44% stake) saved Singapore Telecom (NASDAQOTH:SGAPY.PK)’s earnings this year due to growth in both subscribers and mobile data.

Among these investments, Telkomsel had the largest contribution to the Group’s profit after tax — 14% of the total. Meanwhile, AIS’s contributions were further bolstered by the Thai baht’s 2% against the Singapore dollar and lower corporate taxes. AIS is a stock that I have been high on for a while (see here and here). However, India’s Bharti Airtel (a 32.25% stake) continues to be a drag due to higher depreciation and amortization in Africa and the 11% depreciation of the Indian rupee against the SingDollar.

New Models Emerging

In Singapore, despite significant industry challenges from competitors, Singapore Telecom (NASDAQOTH:SGAPY.PK) still manages to remain a robust foundation for continued profitability. Starhub and M1 are both much smaller in terms of scale, market cap and subscribers. And while overall revenue growth has been difficult, post-paid mobile subscriptions rose overall for all three carriers — SingTel (+1.4%), M1 (+1.1%) and Starhub (+0.8%) — but it is the rise of over the top services such as Facebook Inc (NASDAQ:FB), Google Inc (NASDAQ:GOOG), WeChat and Whatsapp.

Nokia Corporation (ADR) (NYSE:NOK)’s bundling of Facebook Inc (NASDAQ:FB) with their Asha phones in India and other emerging markets will help to sell data packages in the long run as it introduces feature phone customers to what is possible with a low-end smartphone. This is an enormous development that will help drive the conversion of customers from minute plans to data packages. The result will be very good for both Nokia and Facebook in the short term, but the effect for the carriers will be felt in the longer term as the conversion rate will take time. Package minutes are a dying business model outside of emerging markets with only 2G service.

The impact of this will be felt more so in emerging markets than in developed ones; as carriers move into new areas new opportunities are presenting themselves, and the challenge for all carriers is to simply not become a dumb wireless network but rather a true value-added service. To that end, SingTel plans to spend $1.6 billion in three years to acquire companies specializing in digital advertising, content and entertainment. As markets like Thailand build out their 3G and LTE networks, there will be a higher percentage of customers ready to make the switch up to an entry-level smartphone. For Nokia Corporation (ADR) (NYSE:NOK), that means selling low-end Lumias running Windows Phone. For Facebook that means more mobile ad and game revenue.

With the deployment of the Australian National Broadband Network, competition is expected to increase as new entrants enter the market. Optus is the only telco company that owns and operates a fleet of five satellites in Australia, while a sixth is scheduled to be launched this year, used by broadcasters and government organizations, including the Australian Broadcasting Corp. and the Australian Department of Defense. But, Australia and Singapore are mostly saturated markets, and margins there are slipping on the need to upgrade to 4G/LTE while data rates are likely to drop.

In the last six months, Telstra, the number on telco in Australia, added around 600,000 new customers of which half are for 4G service, while Optus only added 53,000 new customers. In Q4 2012, its operating revenue and net profit were down to 5.4%, to A$ 2.7 billion (US$2.59 billion), and 6.9%, A$249 million (US$239.2 billion) respectively. For this reason and the potential growth offered by the developing ASEAN countries and India, SingTel is looking to sell its stake in Optus, offering a financing package at around seven times Optus’ EBITDA. That low-growth capital can then be shifted to its higher growth potential markets.

The Data Plan

Right now Singapore Telecom (NASDAQOTH:SGAPY.PK) needs a strategic shift in its priorities to push back towards a growth model versus its current value one. Any large cap producing a 4+% yield is nothing to sneer at, but it is positioned perfectly to build on its current base by fostering growth of its partners around the region. Investors can and should look at SingTel as less of a service provider and more of a private equity firm at this point. Its structure is like that of a REIT that rents digital real estate. Selling the satellite division of Optus would put it in a better position to pivot towards Thailand and the Philippines, which have not begun to show their promise as mobile computing powerhouses.

Net margins improved to 19.3% in Q1, reversing four quarters of margin erosion. With the recent correction in price and the potential of unlocking significant value from the Optus sale value investors are looking at a good opportunity to grab yield from a firm where the dividend payout is not threatened by current or future cash flows.

The article SingTel Needs Sale to Unlock SE Asia originally appeared on Fool.com and is written by Peter Pham.

Peter Pham has no position in any stocks mentioned. The Motley Fool recommends Facebook. The Motley Fool owns shares of Facebook. Peter is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.