Textron Inc.’s analysis versus peers uses the following peer-set: The Boeing Company (NYSE:BA), Lockheed Martin Corporation (NYSE:LMT), EADS NV (EPA:EAD), General Dynamics Corporation (NYSE:GD), BAE SYSTEMS PLC ORD (PINK:BAESF), Dassault Aviation SA (EPA:AM), Bombardier, Inc. (TSE:BBD.B), Embraer S.A. (EMBR3), Finmeccanica SpA (BIT:FNC) and Korea Aerospace Industries Ltd.(047810). The table below shows the preliminary results along with the recent trend for revenues, net income and returns.

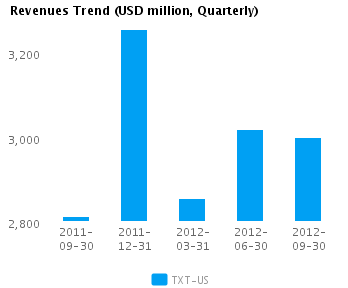

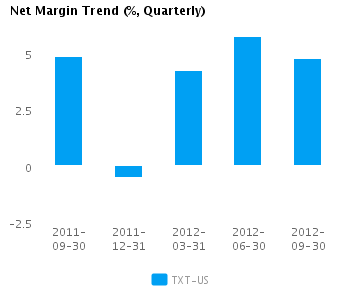

| Quarterly (USD million) | 2012-09-30 | 2012-06-30 | 2012-03-31 | 2011-12-31 | 2011-09-30 |

|---|---|---|---|---|---|

| Revenues | 3,000.0 | 3,019.0 | 2,856.0 | 3,254.0 | 2,814.0 |

| Revenue Growth % | (0.6) | 5.7 | (12.2) | 15.6 | 3.2 |

| Net Income | 142.0 | 173.0 | 120.0 | (17.0) | 136.0 |

| Net Income Growth % | (17.9) | 44.2 | N/A | (112.5) | 47.8 |

| Net Margin % | 4.7 | 5.7 | 4.2 | (0.5) | 4.8 |

| ROE % (Annualized) | 17.7 | 23.0 | 17.0 | (2.2) | 16.8 |

| ROA % (Annualized) | 4.3 | 5.3 | 3.6 | (0.5) | 3.6 |

Valuation Drivers

Textron Inc.’s current Price/Book of 2.2 is about median in its peer group. The market expects TXT-US to grow faster than the median of its chosen peers (PE of 18.8 compared to peer median of 13.5) and to improve its current ROE of 12.6% which is below its peer median of 16.1%. Thus, the market seems to expect a turnaround in TXT-US’s current performance.

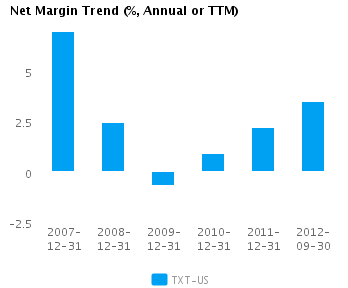

The company’s profit margins are below peer median (currently 3.4% vs. peer median of 5.7%) while its asset efficiency is about median (asset turns of 0.9x compared to peer median of 0.8x). TXT-US’s net margin continues to trend upward and is above (but within one standard deviation of) its five-year average net margin of 2.3%.

Economic Moat

The company enjoys both better than peer median annual revenue growth of 7.1% and better than peer median earnings growth performance 163.0%. TXT-US currently converts every 1% of change in annual revenue into 22.9% of change in annual reported earnings. We view this company as a leader among its peers.

TXT-US’s return on assets is less than its peer median currently (2.9% vs. peer median 4.2%). It has also had less than peer median returns on assets over the past five years (1.7% vs. peer median 3.2%). This performance suggests that the company has persistent operating challenges relative to peers.

The company’s gross margin of 19.3% is around peer median suggesting that TXT-US’s operations do not benefit from any differentiating pricing advantage. In addition, TXT-US’s pre-tax margin is less than the peer median (5.0% compared to 7.7%) suggesting relatively high operating costs.

Growth & Investment Strategy

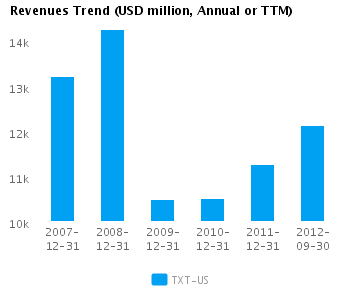

While TXT-US’s revenues have increased more slowly than the peer median (-7.5% vs. 2.9% respectively for the past three years), the market currently gives the company a higher than peer median PE ratio of 18.8. The stock price may be factoring in some sort of a strategic play.

TXT-US’s annualized rate of change in capital of -14.6% over the past three years is less than its peer median of -3.5%. This below median investment level has also generated a less than peer median return on capital of 1.1% averaged over the same three years. This outcome suggests that the company has invested capital relatively poorly and now may be in maintenance mode.

Earnings Quality

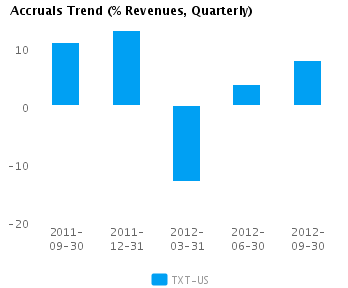

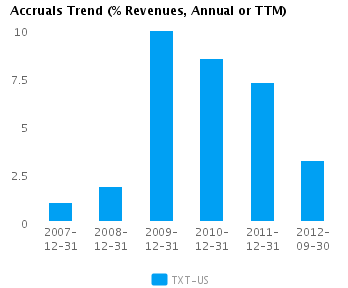

TXT-US reported relatively weak net income margins for the last twelve months (3.4% vs. peer median of 5.7%). This weak margin performance and relatively conservative accrual policy (3.2% vs. peer median of 1.5%) suggest the company might likely be understating its net income, possibly to the extent that there might even be some sandbagging of the reported net income numbers.

TXT-US’s accruals over the last twelve months are positive suggesting a buildup of reserves. In addition, the level of accrual is greater than the peer median — which suggests a relatively strong buildup in reserves compared to its peers.

Trend Charts

Company Profile

Disclaimer

This article was originally written by abha.dawesar, and posted on CapitalCube.