Emerson Electric Co.’s analysis versus peers uses the following peer-set: General Electric Company (NYSE:GE), Honeywell International Inc. (NYSE:HON)*, ABB Ltd (NYSE:ABB), Danaher Corporation (NYSE:DHR), Schneider Electric SA (EPA:SU), Roper Industries, Inc. (NYSE:ROP), AMETEK, Inc. (NYSE:AME) and REGAL-BELOIT CORPORATION (NYSE:RBC). The table below shows the preliminary results along with the recent trend for revenues, net income and returns.

*For CapitalCube’s analysis of Honeywell’s recent earnings announcement click here.

| Annual (USD million) | 2012-09-30 | 2011-09-30 | 2010-09-30 | 2009-09-30 | 2008-09-30 |

|---|---|---|---|---|---|

| Revenues | 24,412.0 | 24,211.0 | 21,044.0 | 20,939.0 | 24,807.0 |

| Revenue Growth % | 0.8 | 15.0 | 0.5 | (15.6) | 9.9 |

| Net Income | 1,968.0 | 2,454.0 | 1,978.0 | 1,724.0 | 2,454.0 |

| Net Income Growth % | (19.8) | 24.1 | 14.7 | (29.7) | 14.9 |

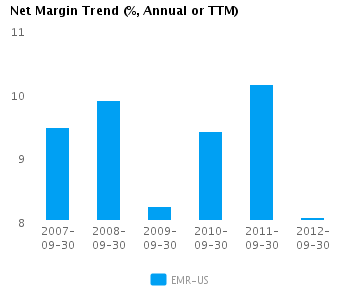

| Net Margin % | 8.1 | 10.1 | 9.4 | 8.2 | 9.9 |

| ROE % | 18.9 | 24.3 | 21.6 | 19.5 | 27.4 |

| ROA % | 8.3 | 10.5 | 9.3 | 8.5 | 12.1 |

Valuation Drivers

Emerson Electric Co. currently trades at a higher Price/Book ratio (3.5) than its peer median (1.8). EMR-US’s operating performance is higher than the median of its chosen peers (ROE of 18.9% compared to the peer median ROE of 13.9%) but the market does not seem to expect higher growth relative to peers (PE of 18.9 compared to peer median of 16.8) but simply to maintain its relatively high rates of return.

The company’s median net profit margins of 8.1% and relative asset efficiency (asset turns of 1.0x compared to peer median of 0.7x) give it some operating leverage. EMR-US’s net margin is its lowest relative to the last five years and compares to a high of 10.1% in 2011.

Economic Moat

Changes in the company’s annual top line and earnings (0.8% and -19.8% respectively) generally lag its peers. This implies a lack of strategic focus and/or inability to execute. We view such companies as laggards relative to peers.

EMR-US’s return on assets is above its peer median both in the current period (8.3% vs. peer median 6.4%) and also over the past five years (9.7% vs. peer median 7.3%). This performance suggests that the company’s relatively high operating returns are sustainable.

The company’s gross margin of 42.5% is around peer median suggesting that EMR-US’s operations do not benefit from any differentiating pricing advantage. In addition, EMR-US’s pre-tax margin of 12.8% is also around the peer median suggesting no operating cost advantage relative to peers.

Growth & Investment Strategy

EMR-US’s revenues have grown at about the same rate as its peers (5.2% vs. 5.7% respectively for the past three years). Similarly, the stock price implies median long-term growth as its PE ratio is around the peer median of 18.9. The historical performance and long-term growth expectations for the company are largely in sync.

EMR-US’s annualized rate of change in capital of 6.2% over the past three years is less than its peer median of 11.4%. This investment has generated a better than peer median return on capital of 14.3% averaged over the same three years. This combination of a relatively low investment with good returns suggests that the company is likely milking its business.

Earnings Quality

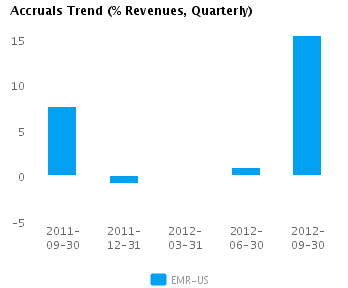

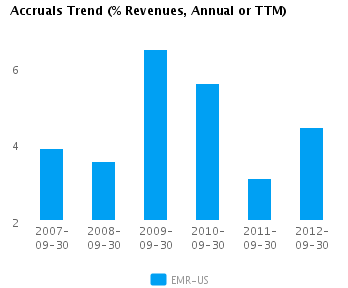

EMR-US’s net income margin for the last twelve months is around the peer median (8.1% vs. peer median of 8.1%). This average margin combined with a level of accruals that is around peer median (4.4% vs. peer median of 4.4%) suggests there possibly isn’t too much accrual movement flowing into the company’s reported earnings.

EMR-US’s accruals over the last twelve months are positive suggesting a buildup of reserves. However, this level of accruals is also around the peer median and suggests the company is recording a proper level of reserves compared to its peers.

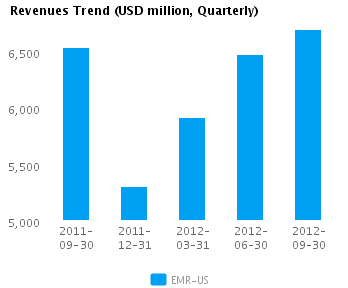

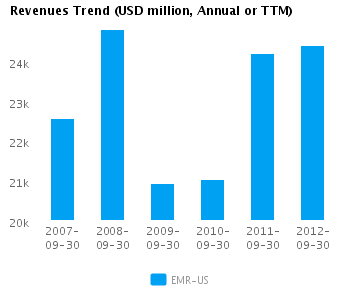

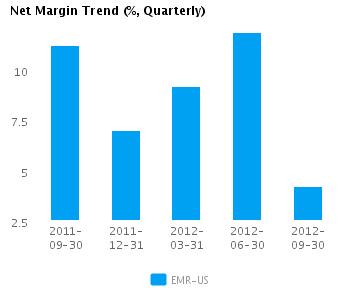

Trend Charts

Company Profile

Disclaimer

This article was originally written by abha.dawesar, and posted on CapitalCube.