Number crunching

Duke Energy Corp (NYSE:DUK)sales clocked in at $5.9 billion for Q1 2013, beating analyst estimates by 3%. Compared with its pre-Progress merger Q1 2012 sales, these newest numbers reflect a 62.5% spike.

But even as sales soared, Duke’s bottom line left investors wanting more. Adjusted EPS came in at $1.02, $0.09 less than 2012’s first quarter and $0.02 below analyst estimates.

Looking ahead, Duke Energy Corp (NYSE:DUK) reaffirmed its 2013 guidance of $4.20 to $4.45 and expects to retain its “dividend stock” title with a 2% compound annualized growth rate.

Diving into Duke

Duke Energy operates a diverse array of businesses, from unregulated and regulated subsidiaries in the U.S. to generation businesses across Central and South America.

Its July 2012 Progress Energy merger had the largest effect on domestic regulated utilities, with adjusted EPS up $0.44 this quarter. Progress Energy utilities added $0.35, while favorable weather, rates, and wholesale revenues made up the rest of the increase.

Duke Energy Corp (NYSE:DUK)’s sales match up with its merger expectations of a 61% increase, and its new utilities have already provided sustainable sales in the face of a tough quarter for unregulated markets. Exelon Corporation (NYSE:EXC) merged with Constellation last March, but its latest earnings report shows that its 44% sales increase didn’t live up to expectations of a 73% spike.

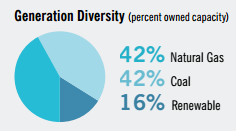

Although expected, Duke Energy Corp (NYSE:DUK)’s commercial power earnings fell $0.03 on a per-share basis, primarily because of falling sales for its Midwest generation fleet. With gas and coal making up major pieces of its capacity pie, adjusted income fell from $30 million in Q1 2012 to just $6 million for this quarter.

Source: Duke Energy 2012 Sustainability Report

Duke’s international division felt a $0.06 squeeze from unfavorable exchange rates and low commodity prices for a Saudi Arabian methanol investment, and low rainfall dried up its Brazil hydro profits. NextEra Energy, Inc. (NYSE:NEE) sold off its last hydro assets in March to “further [optimize our] generation portfolio and concentrate [our] resources.” Although Duke isn’t pulling out today, CEO Jim Rogers once again assured investors that Duke Energy Corp (NYSE:DUK) “will continue to monitor the reservoir levels.”

Is Duke’s dividend dynamite?

Duke boosted its dividend 200% in 2012, and investors currently enjoy a 4.8% dividend yield. The company is nearing the end of its massive $9 billion 6,600 MW modernization project, which could clear up finances for additional payout increases. But the dividend stock’s regulated utilities are in the middle of a myriad of rate-increase applications, and outcomes will ultimately determine how big its bottom line becomes.

Duke Energy Corp (NYSE:DUK)’s future also depends on natural gas pricing. Thirty-seven percent of its regulated utility capacity comes from gas, with another 39% from coal and 17% from nuclear. But its energy diversity should keep any major price spikes under control, with coal and nuclear becoming more cost competitive if gas heads higher.

Source: Duke Energy 2012 Sustainability Report

Although natural gas spikes or stumbles won’t have major effects on Duke, less-hedged utilities such as Atlantic Power Corp (NYSE:AT) could feel a major squeeze. With 58% gas capacity and plans to focus its future on gas and wind, Atlantic Power Corp (NYSE:AT)’s lack of diversity could put it in a tough position in the quarters ahead.

Can Duke become king?

With merger expectations matched and a larger regulated position to ensure sustainable sales, Duke Energy Corp (NYSE:DUK)’s latest quarter has put it in a good position for the future. The dividend stock is already up 17% for 2013, and Duke’s energy diversity will continue to protect it from price wars that other utilities will have to fight.

Looking ahead, investors will need to watch small profit leaks to make sure Duke can keep delivering. Continued international fumbles or a regulatory loss could push down Duke’s upside and decrease its ability to deliver on its dividend.

The article Duke Energy Earnings: Is Bigger Better for This Dividend Stock? originally appeared on Fool.com and is written by Justin Loiseau.

Motley Fool contributor Justin Loiseau has no position in any stocks mentioned, but he does use electricity. You can follow him on Twitter, @TMFJLo, and on Motley Fool CAPS, @TMFJLo.The Motley Fool recommends Exelon.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.