For centuries moats played an important role in keeping attackers at bay. In the modern world, entrepreneurs and established players fight for market share in a similar way. 3D printing is a hot technology and any manufacturer with staying power will need to develop a moat in order to survive. As the technology continues to develop, each company’s patent portfolio will be crucial in determining the firm’s prospects.

SSYS Income from Cont. Ops Quarterly data by YCharts

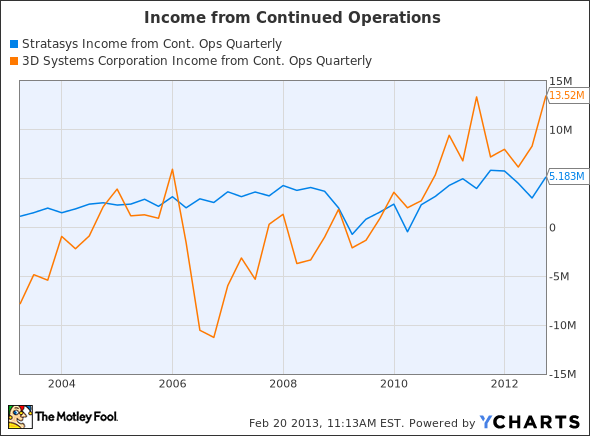

Stratasys, Ltd. (NASDAQ:SSYS) tends to focus on the professional side of the 3D printing industry. It boasts a patent portfolio with more than 500 patents and a recent Wired article shows how a number of lower end consumer printers need to careful in order to avoid infringement of Stratasys’ patents. The company recently merged with the Israeli firm Object. Object’s experience with multi-material printers will help to maintain Stratasys as an innovator.

![]()

Stratasys’ five year revenue growth rate of 8.87% and five year EPS growth rate of 6.74% are strong, but not amazing. Strong tech companies like Google have larger growth figures. Stratasys currently trades at a price to earnings growth ratio of 3.8. This is quite expensive and forces investors to count on strong growth for years and years.

3D Systems Corporation (NYSE:DDD) has had a very public life with allegations that their accounting methods miss-represent organic growth. The firm has gone on a string of acquisitions over the past couple years and this provided a large boost to revenue. These acquisitions have also grown its patent portfolio and after the purchase of Geomagic it will have over 1200 patents. 3D Systems has started to focus on the consumer market. In an effort to make 3D printing more accessible to the masses the company is trying to develop better software solutions that are easier to understand.

This company’s five year revenue growth of 13.89% is significantly strong than Stratasys’. Such numbers must be taken with a grain of salt due to 3D Systems’ large number of acquisitions. The bigger growth figures give the company a smaller price to earnings growth ratio of 1.95. This is less than Stratasys, but still expensive. A price to earnings growth ratio at or above 2 is considered high.

ExOne Co (NASDAQ:XONE) is a young company that recently IPO’d. It focuses on metal 3D printers and industrial grade solutions. Powerful lasers fuse metal particles together layer by layer to create an object. Currently, ExOne leases a number of patents from MIT and will pay them $100,000 per year for the next couple of years. ExOne’s own patent portfolio has expiration dates that range from 2013 to 2029.

ExOne’s own sales are insignificant. In 2011 it reported sales of just $15.29 million. The company has a small long term debt load of $4.13 million. The market has already given this player a market value greater than $300 million. Until ExOne grows and shows that it can deliver solutions that significant numbers of manufactures are willing to pay for, it is best to leave this stock on the watch list.

Conclusion: Growth is already Priced in

Formlab’s Form 1 desktop printer has generated a large amount of press lately. Patent infringement allegations from 3D systems abound. The reality is that established players with large R&D departments are in control. Established players use their patents to maintain their pricing power and control. In the short term this will reduce the availability of low cost solutions and limit the growth of the industry as a whole.

The top 3D printing companies have serious moats with their large patent portfolios, but they are very expensive. Stratasys price to earnings growth ratio of 3.8 and 3D Systems’ ratio of 1.95 price in a large amounts of growth. ExOne is still a small company with paltry sales. Until expectations come down or growth pans out, 3D printers are best analyzed from the sidelines.

The article Do 3D Printers Have Moats? originally appeared on Fool.com and is written by Joshua Bondy.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.