According to research conducted in 2011 by the United States Department of Agriculture, the average American consumes approximately 2,000 pounds of food every year. This includes 185 pounds of meat, 85 pounds of fats and oils, 415 pounds of vegetables, and 630 pounds of milk and milk products. As a result of this consumption, U.S. fast food restaurants produce three billion gallons of used cooking oil and one billion gallons of animal fat waste annually. This huge production of domestic and animal waste creates a problem regarding disposal.

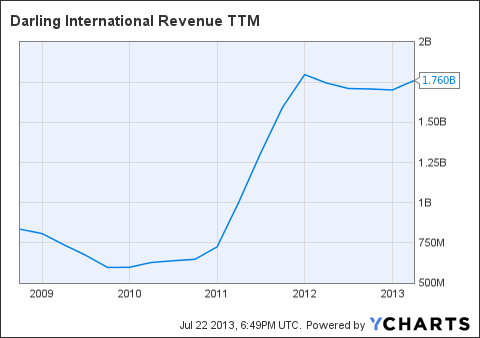

Thankfully though, Darling International Inc. (NYSE:DAR) recycles this waste and converts it into usable, edible products. The company has been in the waste recycling business for more than 130 years. In the last three years of operation, Darling experienced a spike in growth, with the company reporting revenue of more than $1.7 billion in 2012, growing at a CAGR of more than 40% in the last three years.

Going green

Diamond Green Diesel, or DGD, is a 50-50 joint venture project between Darling International Inc. (NYSE:DAR) and Valero Energy Corporation (NYSE:VLO). This joint venture will convert animal fats, used cooking oil, and other economically and commercially viable feed stock into renewable diesel. DGD converts these raw materials (supplied by Darling) into renewable diesel, which Valero transports using its network. The financing for this $413 million project was secured internally from a subsidiary of Valero Energy Corporation (NYSE:VLO) in May 2011.

The plant has a maximum capacity to produce 9,300 barrels per day of renewable diesel, translating to an annual capacity of 137 million gallons per year of renewable diesel. This amounts to diesel conversion of approximately 11% of America’s animal fat and used cooking oil. Renewable diesel has all the properties of petroleum-based diesel, but it reduces greenhouse gases by more than 80% compared to conventional diesel.

In June 2013, plant construction was completed and production began. With the gradual depletion of non-renewable energy sources, the demand for renewable sources of energy is increasing rapidly. In 2012, global investments of $244 billion were made in new renewable sources. Global renewable diesel production reached 22.5 billion liters in 2012, growing at a CAGR of 10.3% since 2010. This signifies the potential that exists for Darling International Inc. (NYSE:DAR) and Valero moving forward.

Considering 10% annual growth, the global biodiesel production will be 24.75 billion liters in 2013 and 27.2 billion liters in 2014. The DGD project has an annual capacity of 520 million liters (137 million gallons) in 2013. This capacity can be expanded to 675 million liters (178 million gallons) in 2014, by spending $50 million-$100 million funded from the joint venture earnings. This implies that this project will produce 2.1% of the world’s biodiesel in 2013, improving to 2.5% in 2014.

Standing strong against competition

Bunge Limited produces oilseed-based biodiesel at its joint venture facilities in the Americas. Bunge oilseed processing plants also act as an important supplier of vegetable oil to major players in the biodiesel industry. The DGD joint venture project, which produces biodiesel in house, will be a significant threat to Bunge’s oilseed processing and biodiesel business.

Renewable Energy Group Inc (NASDAQ:REGI), or REG, is a biodiesel producer that converts natural fats, oils, and greases into biodiesel. REG is a market leader in North America and has presence across the continent. The company’s six bio-refinery plants have an annual capacity of 225 million gallons of biodiesel production capacity.

Darling International Inc. (NYSE:DAR)’s DGD, with an annual capacity of 137 million gallons, has more than 60% of REG’s total capacity. There is significant potential for future expansion for Darling, considering that this is its first green diesel project. The success of this joint venture will fuel expansion efforts, or more joint venture projects, from the two companies in order to beat competition.

Capacity expansion will result in incremental EPS

The DGD project can support a 15% expansion in capacity without requiring additional invested capital; capacity expansion beyond 15% would require additional capital expenditure. The project, which began production in late June, will stay in the start-up phase for the next six months. Expansion will begin after the completion of the start-up phase in December 2013. The expansion beyond 15% will cost around $50 million-$100 million, and the joint venture earnings will fund it.

The DGD project is expected to contribute $45 million and $80 million in earnings for equity shareholders in 2013 and 2014, respectively. The earnings for 2014 have been calculated considering that the project will be running at 115% capacity. The estimated EPS for 2013 is $1.22, of which the DGD project is expected to contribute almost one-fifth at $0.20-$0.25. After capacity expansion in 2014, the project is likely to contribute almost 33% of the expected $1.35 EPS generation.

Free cash flow generation

Darling International Inc. (NYSE:DAR) had $121.8 million in cash on the balance sheet at the end of the first quarter of 2013. The free cash flow is expected to swell to $110 million-$115 million annually in the long term. The current cash and the expected free cash flow are prompting the company’s management to consider a dividend payout and share buyback program. A three-year share buyback program worth $250 million can be initiated without requiring additional leverage, considering the amount of cash and expected income from the DGD project. Considering a 10% year-over-year increase in earnings in the next three years, the EPS is expected to rise to $1.67 from the $1.11 figure in 2012 if the company initiates the share buyback program.

Conclusion

Despite being a leading player in the U.S. in the rendering market, Darling is a relatively small organization with approximately $2.45 billion market capitalization at the end of the first quarter of 2013. This suggests that the company has plenty of scope to grow organically, and inorganically through joint ventures and acquisitions. Darling has enough cash on its balance sheet to target small companies in the rendering segment to improve its profitability.

The DGD project provides a huge opportunity to the company in terms of venturing into the renewable fuel market and gaining significant market share. The company will expand DGD’s production capacity to 115% in 2014, and thus pose a significant threat to REG in biodiesel production capacity.

Shweta Dubey has no position in any stocks mentioned. The Motley Fool recommends Darling International. The Motley Fool owns shares of Darling International.

The article A Dirty Business You Can Bet Your Clean Money On originally appeared on Fool.com and is written by Shweta Dubey.

Shweta is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.