The largest cruise company in the world, Carnival Corporation (NYSE:CCL), is trading 9.98% lower from where it started in 2013, a rarity in this bull market.

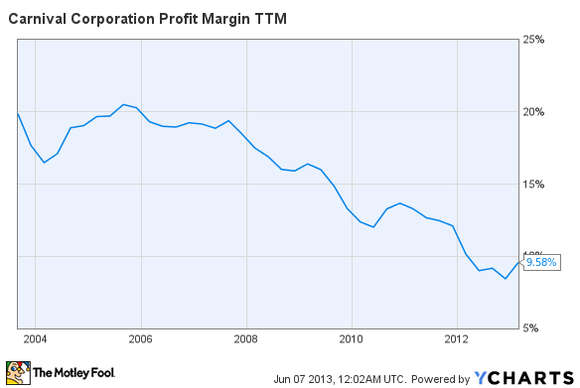

The company operates about 100 cruise ships and tour companies in Alaska and Canada. Based on market capitalization, Carnival Corporation (NYSE:CCL) is valued at $26.73 billion, and the stock carries a price to book ratio of 1.13. Currently, the company carries a TTM profit margin of 9.58%.

With Carnival Corporation (NYSE:CCL) trading at nearly half of its all time-highs, is the company a bargain in this inflated market, or should investors look for a different company to set sail on?

Strengths:

Historic Revenue Growth:

In 2003, Carnival Corporation (NYSE:CCL) reported revenue of $6.71 billion; in 2012, the company announced revenue of $15.38 billion, representing year over year annual growth of 9.65%, a strong trend that should continue into the future, with projections placing 2015 revenue at $18.35 billion. This growth has been a result of multiple mergers and a rapidly growing fleet.

Opportunities:

Dividend Growth: Since implementing their dividend program in 1988, Carnival has consistently raised their dividend payouts, and is widely anticipated to do so into the future.

Competitors:

Major publicly traded competitors of Carnival include Norwegian Cruise Line Holdings Ltd (NASDAQ:NCLH), Royal Caribbean Cruises Ltd. (NYSE:RCL), The Walt Disney Company (NYSE:DIS), and Comcast Corporation (NASDAQ:CMCSA).

Norwegian Cruise Line Holdings Ltd (NASDAQ:NCLH) is valued at $6.27 billion, does not pay out a dividend, and carries a price to earnings ratio of 70.87. The company competes directly against Carnival, offering cruise experiences. Norwegian Cruise Line Holdings Ltd (NASDAQ:NCLH)’s business is not as financially strong as Carnival’s, with a TTM profit margin of 3.01%.

Royal Caribbean Cruises Ltd. (NYSE:RCL) is valued at $7.68 billion, pays out a dividend yielding 1.37%, and carries a price to earnings ratio of 169.23. Royal also competes in the cruise industry, but possesses an incredibly weak business model with a TTM profit margin of only 0.61%.

The Walt Disney Company (NYSE:DIS) is valued at $113.60 billion, pays out a dividend yielding 1.19%, and carries a price to earnings ratio of 19.16. Walt Disney’s business stretches across several industries and is extremely diversified, but the company most directly competes against Carnival through its theme park segment. The Walt Disney Company (NYSE:DIS)’s business model is strong and thriving, with a TTM profit margin of 13.64%.

Comcast Corporation (NASDAQ: CMCSA) is valued at $105.77 billion, pays out a dividend yielding 1.94%, and carries a price to earnings ratio of 16.92. Comcast’s core business, much like Disney’s, is diversified, but this media giant competes directly with Carnival through it theme park segment. With a TTM profit margin of 10.18%, the company’s business is profitable.

The Foolish Bottom Line

Financially, Carnival Corporation (NYSE:CCL) is mildly strong. The company possesses stable revenue growth, a growing dividend, and a leading industry position. The major weaknesses of the company include its massive debt load and single digit profit margin, which has been in a state of downfall over the past decade. Looking forward, the company is likely to continue its trend of dividend growth and should repeat history and continue expanding its ship fleet. All in all, the recent pullback in Carnival may present a long-term buying opportunity to long-term investors, however until the cruise industry stabilizes and the company’s profit margin displays signs of strength, investors should stay away from this volatile cruise-liner.

The article Is This Company A Prime Destination for Investors? originally appeared on Fool.com and is written by Ryan Guenette.

Ryan Guenette has no position in any stocks mentioned. The Motley Fool recommends Walt Disney. The Motley Fool owns shares of Walt Disney. Ryan is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.