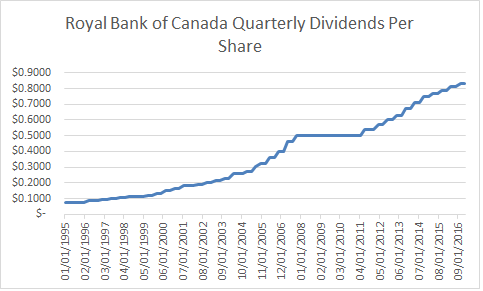

Royal Bank of Canada (NYSE:RY), a diversified financial services company, provides personal and commercial banking, wealth management, insurance, investor, and capital markets products and services worldwide. This is another bank that has operations in the US. Royal Bank of Canada (NYSE:RY) has paid dividends since 1870. Over the past decade, Royal Bank of Canada (NYSE:RY) has increased dividends per share by 7.60%/year, and that’s despite the fact that the annual dividend was left unchanged in 2009 and 2010. Earnings per share have increased by 6.60%/year over the same time period. The bank sells for 14.40 times earnings and yields 3.40%.

Follow Royal Bank Canada Montreal Que (NYSE:RY)

Follow Royal Bank Canada Montreal Que (NYSE:RY)

Receive real-time insider trading and news alerts

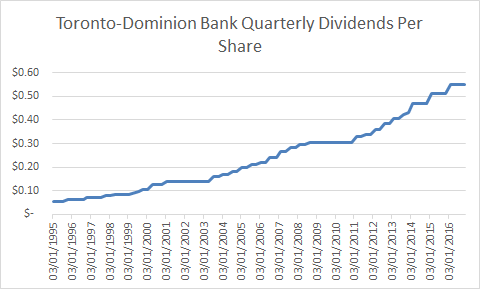

Toronto-Dominion Bank (NYSE:TD) provides financial and banking services in North America and internationally. The company also has significant operations in the US. Toronto-Dominion Bank (NYSE:TD) has paid dividends since 1857. Over the past decade, Toronto-Dominion Bank (NYSE:TD) has increased its quarterly dividends per share at a rate of 8.60%/year, even though the annual dividend was left unchanged in 2010. Earnings per share have increased by 4%/year over the same period. The bank sells for 14.10 times earnings and yields 3.30%.

Follow Toronto Dominion Bank Ont (NYSE:TD)

Follow Toronto Dominion Bank Ont (NYSE:TD)

Receive real-time insider trading and news alerts

All of those banks can easily be purchased by US investors in their regular taxable or tax-deferred accounts. There is a sixth Canadian bank, called National Bank of Canada (OTCMKTS:NTIOF), which is a little bit more difficult to purchase for US investors because it is traded on the pink sheets and not on the major exchanges. Because of low liquidity, and because some brokers do not allow access to that, it may not be available for everyone.

Overall, I like the fact that Canadian Banks didn’t cut or eliminate dividends during the 2007 – 2009 financial crisis. Instead, they kept them steady for a few years, and have been increasing them for a few years now as well. I don’t believe this was due to dumb luck, but because there were stricter lending practices than what we had in the US prior to the Great Recession.

In the grand scheme of things, I am bullish on Canada in the very long-term. An investment in all banks is a bet that Canada will be a developed country in 30 – 40 – 50 years (after that – I don’t care from a personal perspective). It is a bet that its economy will gradually grow over time, the number of people will increase, and that Canadian people and businesses will need the services of a financial institution. I think that the Canadian government has its house in order, and that the relatively more open immigration system will encourage faster population growth.

It seems that most of the banking in Canada is done through one of those five large banks. There are a few smaller ones, but I chose to only focus on the larger entities. Once a consumer starts using the services of one of the banks, they get used to it, and the switching costs are high. Once you establish that relationship with the bank and a banker, chances are that you will do checking through it, manage your investments, use credit cards and take on loans for a car or a mortgage on a house. Therefore, I believe they have competitive advantages, and scale of operations.

That being said, I have no idea whether there will be a financial crisis in Canada in the next 5 – 10 years. It is possible that one of the largest five banks fails during the next major recession. That’s fine, because the ones left standing will pick up the business and do better. This is why I am putting equal amounts of investment in each bank. No matter how the economy does, banking needs to get done, meaning that one of those five banks will get business. Again, as a long-term investor, my holding period is in the decades. I know growth is not going to be smooth year over year, which is why I am fine with encountering bumps along the road. This will help me build out my positions at cheaper prices.

Canada’s economy is dependent on volatile commodity prices, which are some of the country’s chief exports. It is exposed to the cyclical commodity prices such as oil and natural gas. Therefore, its banks will be more affected by drops in commodity prices than Wells Fargo & Co (NYSE:WFC) in the US. In addition, the Canadian dollar is also closely correlated with the rise and fall of commodity prices. For a US investor, this means that the level of dividend income in US dollars from their Canadian dividend portfolio may be a little volatile, even if it rises over time in the base currency. I do believe it makes sense however to evaluate the fundamental performance of an international dividend company in base currency, rather than in US dollars.

It is also possible that earnings on those banks do not do that well over the next decade. That’s fine, since I am essentially getting paid anywhere between 3.50% and 4% annually to hold on to those banks. I think that even if earnings do not grow that much, dividends per share will grow enough to maintain purchasing power of my income. This is why I am slowly putting money once per year in those banks, in case I get the timing of the purchases wrong. Actually, even if I get the timing wrong in the next five years, that’s ok. It is ok, because I am investing for the next 30-40-50 years, not for the next five months. I have a conviction behind those ideas, which is why I would not hesitate to average down if the right opportunity comes along.

US investors should consider holding those shares in a tax-deferred account. Canadian dividends face a 15% withholding in taxable accounts for US residents. However, there is no withholding tax in retirement accounts such as Roth IRA’s.

Full Disclosure: Long all companies listed above

Additional Links:

(1) http://www.dividendgrowthinvestor.com/2013/12/nine-quality-dividend-stocks-purchased.html