It was bound to happen: Natural gas prices are heading higher, and utilities that upped their investments over the last few years could be up the creek without a profitable paddle. Let’s look at where prices are headed, who’s got gas, and what secret dividend stocks could emerge ahead from the newest natural gas alternative.

Natural, but not cheap

Natural gas’ heyday may be over. The Energy Information Administration released its Short-Term Energy Outlook report (link opens in PDF) this week, and high prices are pushing down demand for this alternative fuel. Natural gas fueled 30.4% of total electricity generation in 2012, but the EIA projects that amount to drop to 28% for 2013. That makes sense, considering 2013 Henry Hub natural gas prices are expected to clock in 28% above last year’s $2.75 per MMBtu.

Source: EIA.gov.

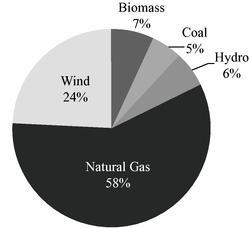

Atlantic Power Corp (NYSE:AT)‘s dividend recently received a haircut, and the utility is counting on natural gas to push its profits back into the black. With 58% of its 2012 generation capacity coming from natural gas, any price increase could have an adverse effect on the dividend stock’s ability to balance its books.

Source: Atlantic Power 10-K.

Source: Exelon Investor Relations Website

But with a battered valuation pushing Exelon Corporation (NYSE:EXC) shares up 23% in the past three months, there could be plenty of growth opportunity to accompany this dividend stock’s 6% yield.

Coal on the comeback?

With natural gas prices up, utilities are looking elsewhere for their fuel. The answer: renewables and coal. And while renewables demand is expected to bump up 3.4% for 2013, a 7.8% spike in demand could put coal users back in cost-competitive territory.

Duke Energy Corp (NYSE:DUK) CEO Jim Rogers recently criticized

Where to invest?

When it comes to picking dividend stocks, there’s no secret recipe. Although TECO Energy, Inc. (NYSE:TE) investors are probably popping the bubbly while Atlantic investors cringe, a dynamic and diverse energy portfolio is the only true way to pull long-term profit. Be sure to check out my other article outlining four companies predicted to ride the renewables rise, and make your investment decisions accordingly.

The article Will Natural Gas Destroy These Dividend Stocks? originally appeared on Fool.com is written by Justin Loiseau.

Fool contributor Justin Loiseau has no position in any stocks mentioned, but he does use electricity. You can follow him on Twitter, @TMFJLo, and on Motley Fool CAPS, @TMFJLo.The Motley Fool recommends Exelon and Southern.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.