Open Square Capital, a young asset manager with thematic long-term investment approach, recently released its Q1 2019 Investor Letter – a copy of which you can download here. Among other things in the letter, such as the fund quarterly performance – a gain of 44.35%, it also disclosed its thorough analysis of the stock that amasses 15% of its portfolio, Apple Inc. (NASDAQ:AAPL). In short, the fund strongly believes in the company’s future growth and expects a lot from its services sector which has just being to develop. Namely, last year Apple’s services brought back $37 billion, which represents 14% of the total company’s revenues, and Open Square Capital a greater potential.

“We last discussed Apple in our 2017 Q1 letter. Since it’s been two years, let’s provide you with an update. As background, we’ve owned Apple shares since the fund’s inception nearly 3.5 years ago. At the time, Apple was trading at ~$116/share, and today it’s selling for about ~$200/share. Along the way, we’ve collected $9.28/share in dividends, and remarkably total share count has shrunk by over 17%, falling by almost 1B shares to 4.77B shares. With fewer shares, we’re now enjoying a bigger slice of Apple’s earnings pie. Apple comprises about 15% of our portfolio, and we’ve maintained that weighting fairly consistently. Our baseline investment thesis remains unchanged:

1)Hardware replacement cycle maturing, providing a large recurring revenue stream;

2)Monetization of the ecosystem via broadening and deepening of Apple Services;

3)Improving cash flow generation by shifting revenues from singular transactions (hardware sales, etc.) to recurring subscription/licensing based revenue streams with higher profitability;

4)Continuing share buybacks shrinks the outstanding available shares;

5)Free optionality on numerous tangential themes in other industries, including healthcare, entertainment, vehicles and media; and

6). . . it’s silly cheap on almost any metric.

The company’s size and success hasn’t insulated its shares from short-term volatility. Within the past year, Apple’s shares have reached $230/share and fallen to $142/shares. Much of the concerns today centers on slowing iPhones sales worldwide, market competition, challenges in India, and even general apathy. For us, we’ve always maintained that iPhone sales will slow as Apple has already dominated the high-end handset market. Further growth is more difficult to come by as Apple has intentionally sought to maximize profits and not market share.

In the next few years, we anticipate the wider availability of faster 5G wireless service will catalyze a large upgrade cycle, but until then, iPhone/hardware sales will ebb and flow as the upgrade cycles play out. Even a mature market, however, translates to tremendous recurring profits as people will naturally replace their iOS devices with more current versions when their devices break, degrade, etc. Additionally, slower growth is still growth, and a stable and growing base of iOS users means the ecosystem becomes a riper asset to monetize.

Apple’s deliberate focus on the high-end market gives its ecosystem a tremendous advantage today. By focusing on the well-heeled or those willing to spend more, Apple’s 1.4B users outspend their Android counterparts by almost 4:1 for services. Take a moment to appreciate that. Although two people can own arguably the same advanced smartphone, one will spend 4 times more for services in their ecosystem. So if you’re a developer, producer, or media executive, can you afford not to play in the iOS ecosystem? For most product developers, the answer is no, and thus Apple becomes your digital Les Clefs d’Or concierge, a high-end guide that curates, recommends and provides you with access to an ever expanding digital world, but one that values your privacy and exercises discretion while doing so.

Monetizing the Ecosystem

For Apple the next 5 years of growth will come from monetizing this ecosystem, which is why we believe this company is on the cusp of a major transition/expansion into new industries. Such an endeavor would normally be fraught with risk for other companies, but Apple already has a devoted following, and most of the services introduced are ancillary to its business and an evolution of its offerings.

It’s taken a few years, but the transition is now beginning as the baton for future growth is passed from hardware to services. Although iPhone sales still represent the lion’s share of Apple’s total revenues (>60%), services has steadily gained traction. In 2018, services generated more than $37B, or about 14% of Apple’s total revenues (i.e., 1/4 the size of iPhone’s revenues).

Despite its smaller size, Apple’s Services packs twice the punch. Given how easily services scale (i.e., adding a new subscriber to Apple Music doesn’t increase costs materially), this segment is almost twice as profitable as hardware sales. In its most recent report, the company revealed for the first time that Apple Services had margins of ~63% vs. ~34% for Apple’s hardware products. Thus, as services revenue grows faster than hardware sales, we anticipate Apple’s overall margins to improve. So not only will Apple begin to grow top line sales, but concurrently expand bottom line margins, an unusual feat given a $940B company.

Currently, about half of Apple’s services revenue comes from the App Store and Google’s Traffic Acquisition Costs (“TAC”) payments (i.e., every time you search for something using Siri or Apple’s search bar, it routes that query to Google). In CY 2018, TAC payments totaled ~$9.5B, and we anticipate it will grow at >25% for the next few years. Similarly the App Store should grow around 15% a year for the next few years. So with these two core drivers, services revenue has a clear path to grow to $50B in the next two years. After that? It’ll be up to Apple’s newest offerings.

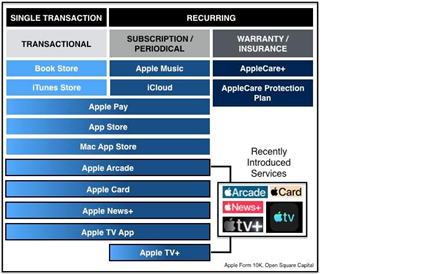

Showtime

At a recent presentation held on March 25th, the company unveiled a host of products in entertainment (Apple TV App and Apple TV+), news (Apple News+), video games (Apple Arcade) and financial services (Apple Card). We’ve categorized them in the following manner to give you an idea for how we think about these services:

it will grow at >25% for the next few years. Similarly the App Store should grow around 15% a year for the next few years. So with these two core drivers, services revenue has a clear path to grow to $50B in the next two years. After that? It’ll be up to Apple’s newest offerings. ShowtimeAt a recent presentation held on March 25th, the company unveiled a host of products in entertainment (Apple TV App and Apple TV+), news (Apple News+), video games (Apple Arcade) and financial services (Apple Card). We’ve categorized them in the following manner to give you an idea for how we think about these services:You’ll notice that as Apple builds out its offerings, the focus shifts from singular transactions to generating recurring revenue in large markets. Some of the markets will certainly be more challenging to penetrate. For instance, Apple TV+, Apple’s new streaming service available in the fall, will encounter stiff competition against entrenched rivals and upstarts such as Hulu, Disney+, Netflix, Amazon Prime, and HBO. The streaming video on demand space isn’t exactly a green space. Much of its success will depend on the quality and popularity of its programming. Nevertheless if Apple Music was able to become the #1 streaming music service in the US since its launch only three years ago, it bodes well for how quickly/willing Apple’s users are to adopt a new service. We’ve made a few projections based on what these categories could generate, but it’s early days, so we’ll firm those numbers up once launched.

The Digital Wallet

While it’s great that Apple will provide more entertainment options to us, we’re more intrigued by how the company is increasingly retaining its customers, and among the five announced offerings, the Apple Card could be the most impactful. From a high level, McKinsey estimates that global digital commerce volume (i.e., online and in-app purchases) will exceed $6 trillion by 2022, and mobile commerce will comprise 70% of those sales. Digitization provides two-sided benefits, it lowers the cost of each transaction and increases customer satisfaction. It removes friction at the point of sale and enhances security for its users. As the shopping experience migrates increasingly to the digital world, who controls the digital wallet holds the keys to the electronic kingdom.

Loup Ventures estimates that Apple Pay has ~383M users (i.e., ~43% of the active iPhone base), but 88% of Apple Pay users are international vs. 12% in the US even though 21% of iPhone users are in the US. Adoption rates vary by country, but some countries like China have effectively gone cashless. According to iResearch Consulting Group mobile payments in China totaled $9T. In the US? $112B. One reason for the lower usage in the US is because US public transit systems have been slower to accept digital wallet payments. Recently NYC and Chicago transit authorities announced plans to accept Apple Pay, so waving your phone while running through a subway turnstile will soon be a reality, speeding your journey and Apple Pay’s adoption. On the whole, digital wallet penetration in the US is projected to grow at a 45% CAGR, and reach $400B in annual flows by 2022.

Introducing an Apple Card will help accelerate this trend as credit cards are used in about a third of all transactions in the US. To receive the highest 2% rebate using the Apple Card, you’ll also need to use it with Apple Pay (i.e., either swiping at the point of sale in a store or using it to pay when shopping online). Apple Pay’s revenue is still small, comprising just 1-2% of total services revenue, but growing rapidly. As transactions grow in volume (1.8B in the December 2018 quarter alone, a 3x growth from last year), so too will revenues. Admittedly, we anticipate the Apple Card won’t move the needle much as we estimate Apple will earn approximately the same ~0.15% per transaction, but that’s not what’s important.

Encouraging Apple Pay adoption is all about changing consumer behavior so that eventually using a digital wallet becomes habitual and entrenches Apple as a toll taker for commercial transactions. Furthermore, it increases customer captivity because trust is the handmaiden of loyalty. As technology companies embrace services, privacy and security become increasingly paramount, and with Apple’s suite of biometric protections (i.e., two-factor identification using Touch ID, Face ID, password or PIN), the more you trust Apple with your personal financial data, the more you’ll trust Apple with all your data. So once you’re used to storing financial data on Apple’s devices, perhaps you’ll trust Apple to store your healthcare data, especially as your Apple Watch and iPhone track your activities. Ultimately, healthcare is one of the holy grails, a $3.5T industry ripe for disruption. We’re in the midst of a deeper dive into opportunities in this space as a next potential investment theme for the fund, and will update you on our findings in later letters, just know that Apple is a multi-prong investment for us.

As consumer behavior, data/data analytics and advancements in software/hardware intersect, this is where it gets interesting. Introducing products in one category can facilitate entry into another, and as Apple evolves its services offerings, we anticipate Apple products will eventually envelope our lives. We needn’t be patient investors while we wait because Apple is buying back shares and paying dividends while we wait. All we have to do is be sensible and let the tree bear fruit.”

FooTToo / Shutterstock.com

Heading into the first quarter of 2019, a total of 116 of the hedge funds tracked by Insider Monkey were bullish on this stock, a change of 4% from the second quarter of 2018. Below, you can check out the change in hedge fund sentiment towards AAPL over the last 14 quarters. With hedgies’ sentiment swirling, there exists a few notable hedge fund managers who were increasing their stakes meaningfully (or already accumulated large positions).

The largest stake in Apple Inc. (NASDAQ:AAPL) was held by Berkshire Hathaway, which reported holding $39370.2 million worth of stock at the end of September. It was followed by Fisher Asset Management with a $2013.8 million position. Other investors bullish on the company included Citadel Investment Group, AQR Capital Management, and Adage Capital Management.

Co-Founder and Research Director at Insider Monkey

When Jeff Bezos said that one breakthrough technology would shape Amazon’s destiny, even Wall Street’s biggest analysts were caught off guard.

Fast forward a year and Amazon’s new CEO Andy Jassy described generative AI as a “once-in-a-lifetime” technology that is already being used across Amazon to reinvent customer experiences.

At the 8th Future Investment Initiative conference, Elon Musk predicted that by 2040 there would be at least 10 billion humanoid robots, with each priced between $20,000 and $25,000.

Do the math. According to Musk, this technology could be worth $250 trillion by 2040.

Put another way, that’s roughly equal to:

175 Teslas

107 Amazons

140 Metas

84 Googles

65 Microsofts

And 55 Nvidias

And here’s the wild part — this $250 trillion wave isn’t tied to one company, but to an entire ecosystem of AI innovators set to reshape the global economy.

It’s a leap so massive, it could reshape how businesses, governments, and consumers operate worldwide.

Even if that $250 trillion figure sounds ambitious, major firms like PwC and McKinsey still see AI unlocking multi-trillion-dollar potential.

How could anything be worth that much?

The answer lies in a breakthrough so powerful it’s redefining how humanity works, learns, and creates.

And this breakthrough has already set off a frenzy among hedge funds and Wall Street’s top investors.

What most investors don’t realize is that one under-owned company holds the key to this $250 trillion revolution.

In fact, Verge argues this company’s supercheap AI technology should concern rivals.

Before I reveal the details, let’s talk about how some of the richest people on the planet are positioning themselves.

Bill Gates sees artificial intelligence as the “biggest technological advance in my lifetime,” more transformative than the internet or personal computer, capable of improving healthcare, education, and addressing climate change.

Larry Ellison — through Oracle, is spending billions on Nvidia chips and partnering with Cohere to embed generative AI across Oracle’s cloud and apps.

Warren Buffett — not known for tech hype — says this breakthrough could have a ‘hugely beneficial social impact.

When billionaires from Silicon Valley to Wall Street line up behind the same idea — you know it’s worth paying attention to.

Even as we admire what Tesla, Nvidia, Alphabet, and Microsoft have built, we believe an even greater opportunity lies elsewhere…

But the real story isn’t Nvidia — it’s a much smaller company quietly improving the critical technology that makes this entire revolution possible.

And judging by what I’m hearing from both Silicon Valley insiders and Wall Street veterans…

This prediction might not be bold at all:

A few years from now, you’ll wish you’d owned this stock.

The best part? You can discover everything about this company and its groundbreaking technology right now.

I’ve compiled everything you need to know about this groundbreaking company in a detailed, members-only report.

Trust me — you’ll want to read this report before putting another dollar into any tech stock.

For a ridiculously low price of just $9.99 a month, you can unlock a year’s worth of in-depth investment research and exclusive insights – that’s less than a single fast food meal!

Here’s why this is a deal you can’t afford to pass up:

• Access to our Detailed Report on this Game-Changing AI Stock: Our in-depth report dives deep into our #1 AI stock’s groundbreaking technology and massive growth potential.

• 11 New Issues of Our Premium Readership Newsletter: You will also receive 11 new issues and at least one new stock pick per month from our monthly newsletter’s portfolio over the next 12 months. These stocks are handpicked by our research director, Dr. Inan Dogan.

• One free upcoming issue of our 70+ page Quarterly Newsletter: A value of $149

• Bonus Reports: Premium access to members-only fund manager video interviews

• Ad-Free Browsing: Enjoy a year of investment research free from distracting banner and pop-up ads, allowing you to focus on uncovering the next big opportunity.

• 30-Day Money-Back Guarantee: If you’re not absolutely satisfied with our service, we’ll provide a full refund within 30 days, no questions asked.

If you’re thinking about getting in, don’t wait – because once Wall Street catches wind of this story, the easy money will be gone.

Space is Limited! Only 1000 spots are available for this exclusive offer. Don’t let this chance slip away – subscribe to our Premium Readership Newsletter today and unlock the potential for a life-changing investment.

Here’s what to do next:

1. Subscribe to our Premium Readership Newsletter for just $9.99 a month. (33% Off – was $14.99).

2. Enjoy a year of ad-free browsing, exclusive access to our in-depth report on the revolutionary AI company, and the upcoming issues of our Premium Readership Newsletter over the next 12 months.

3. Sit back, relax, and know that you’re backed by our ironclad 30-day money-back guarantee.

Don’t miss out on this incredible opportunity! Subscribe now and take control of your AI investment future!

Co-Founder and Research Director at Insider Monkey

My name is Inan Dogan. I’m the co-founder and Research Director of Insider Monkey. I have an important message for you today.

Since March 2017, my stock picks have returned 16.5% annually. Today, I’ve found an opportunity even bigger than my British American Tobacco call.

Two years ago, Wall Street wrote off British American Tobacco (BTI) as a “melting ice cube.” The stock had crashed 40% from its peak, and consensus said the business was dying.

We looked under the cover and realized they were wrong.

We alerted our subscribers, and BTI returned 90% in just 16 months.

Now if you had invested just $10,000 in BTI in June 2024, you’d be sitting on $19,000 in October 2025.

Today, we have identified a nearly identical pattern in a digital-first giant trading at $3.

While the market panics over a surface-level revenue decline, our PhD-led research shows management has actually surgically cut $100 million in waste to focus on high-margin growth.

This pattern is a hallmark of our 16.5% annual return track record. The current opportunity offers a 400% upside potential—dwarfing even our 90% BTI return.

Get the ticker for our new “Underdog” pick and the full BTI case study for just 99 cents.

This exclusive offer is for NEW newsletter subscribers ONLY! Join our Premium Readership Newsletter for only $0.99 and become part of a savvy investor community.!

This offer vanishes in 7 days, so don’t miss your chance to lock in market beating returns! Sign up NOW! The monthly newsletter comes with a 30-day, no-risk money-back guarantee. This offer is available to the first 1000 new investors who respond.

Here’s why this is a deal you can’t afford to pass up:

Access to our Detailed Report on this $3 stock with 400% upside potential.

BONUS REPORT on our #1 AI-Robotics Stock with 10000% upside potential: Our in-depth report dives deep into our #1 AI/robotics stock’s groundbreaking technology and massive growth potential.

One New Issue of Our Premium Readership Newsletter: You will also receive one new issue per month and at least one new stock pick per month from our monthly newsletter’s portfolio over the next 12 months. These stocks are handpicked by our research director, Dr. Inan Dogan.

One free upcoming issue of our 70+ page Quarterly Newsletter: A value of $149

Bonus Content: Premium access to members-only fund manager video interviews

Ad-Free Browsing: Enjoy a month of investment research free from distracting banner and pop-up ads, allowing you to focus on uncovering the next big opportunity.

Lifetime Price Guarantee: Your renewal rate will always remain the same as long as your subscription is active.

30-Day Money-Back Guarantee: If you’re not absolutely satisfied with our service, we’ll provide a full refund within 30 days, no questions asked.

Space is Limited! Only 1000 spots are available for this exclusive offer. Don’t let this chance slip away – subscribe to our Premium Readership Newsletter today and unlock the potential for a life-changing investment.

Here’s what to do next:

1. Head over to our website and subscribe to our Premium Readership Newsletter for just $0.99.

2. Enjoy a month of ad-free browsing, exclusive access to our in-depth report on the Trump tariff and nuclear energy company as well as the revolutionary AI-robotics company, and the upcoming issues of our Premium Readership Newsletter.

3. Sit back, relax, and know that you’re backed by our ironclad 30-day money-back guarantee.

Don’t miss out on this incredible opportunity! Subscribe now and take control of your AI investment future!