I must confess I am finding the current market to be one of the most frustrating periods of my investing life. I’ve always liked a defensive growth stock, but nowadays they seem to be so expensive that the only thing left to do is refrain from buying and sulk in the corner for a while. However, I can’t complain too much about Allergan, Inc. (NYSE:AGN), as it’s a stock I held during its sterling run lately. I like the stock, but it is fairly valued now and on a risk reward basis I won’t be buying back in just yet.

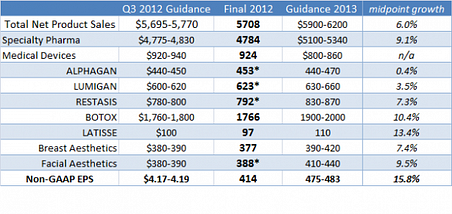

I initially covered the stock in an article linked here, which is useful as a primer for research. In order to assess current prospects I’ve tabulated what Allergan forecast for the full year in 2012 alongside what it achieved and then the guidance for 2013. The starred figures in the middle column are for those products that beat the mid-point of full year guidance from Q3.

Allergan is offering a mix of mid-single digit top line growth along with mid-teens EPS growth. All of this is fine but, in my opinion, it doesn’t justify a trailing PE ratio of 31 and a forward PE of 22. Moreover, the forecast figure of around $1 billion in free cash flow puts it on a free cash flow yield of around 3.2%. It’s hardly cheap.

Botox Driving Growth

With that said, investors need to appraise the long term prospects for the company, and they do look solid. The biggest single product is the market leading neuromodulator Botox. AGN claims to have around 77% of the global market and is gaining share in therapeutic uses but losing it in aesthetics. The plan is to increase sales in new or expanding indications like migraine, spasticity and bladder treatments.

Obviously with such a dominant position the concern is that it could lose some share in future. Indeed, Valeant Pharmaceuticals Intl Inc (NYSE:VRX) is buying Medicis partly because it wants to expand its dermatology operations with Dysport (the key rival to Botox). Furthermore, Merz Pharma will be allowed to re-commercialize Xeomin for aesthetics in the current quarter. Listening to the commentary around the results, AGN seem to think it may gain some market share from Dysport as a result of the impending takeover but that it will lose some thanks to Xeomin’s re-introduction; this is baked into the guidance. Given that Botox has 84% of the US aesthetic market it’s not surprising to see some pressure. AGN also faces competition from Johnson & Johnson (NYSE:JNJ) , which has an anti-wrinkle product that it obtained from the acquisition of Metnor. However, JNJ hasn’t exactly set the world on fire with its skin care numbers lately.

Turning back to Botox, I’m a great believer in the idea that neuromodulators have a bright future for aesthetic purposes. More old people, more divorces, more wealthy women running around without kids, is there a more perfect climate for more plastic surgery? Indeed, AGN pointed out that Italy, Spain and France (challenged economies in Europe) reported strong numbers.

Looking at Botox longer term, the growth is expected to occur within therapeutic, and it has been obtaining approvals for its migraines and bladder treatments in various countries recently. However, the key news recently has been the FDA approval for use in overactive bladder treatment. Prospects look good for Botox, and investors can feel confident.

Ophthalmology Looking Good Too

Referencing the table above, it’s clear that AGN gave good numbers in ophthalmology. Indeed, I noted that Johnson & Johnson also gave good numbers in eye care. Its segment sales growth was 6.4% in the last quarter, which strikes me as an acceleration from the kind of 5% growth that the industry was achieving at the start of the year.

Eye-care is relatively recession resistant. A specialist company like The Cooper Companies, Inc. (NYSE:COO) argues that a typical growth rate for the industry in a recession is 3-5% moving up to 5-7% when the economy recovers. The good news is that COO, JNJ and AGN (8.2% in local currencies for Q4) are all reporting numbers in excess of the ‘recession’ figures, so does this imply the economy is recovering or that eye-care is experiencing a ramp up in growth thanks to demographic issues? I suspect the latter.

However, it isn’t all plain sailing. Lumigan (eye pressure) patents will expire in August 2014 and Novartis AG (ADR) (NYSE:NVS) is believed to be planning to release a generic by the end of 2014. Novartis needs to do something because of all the companies mentioned, its eye-care division (Alcon) seems to have the slowest growth. Bausch & Lomb is probably available for purchase, but I doubt Novartis is interested.

Where Next for Allergan?

I like the company, I like its execution, I like the quality of its long term growth prospects. However, I cant see a reason to chase the evaluation higher here. When I last looked at the stock it was closer to $90 and I mentioned that it had the potential to ‘do its earnings.’ Well it did that and some more, so at $104 it is probably fairly priced. I’m afraid it’s another one for the increasingly lengthening watch list.

The article No Sign of a Slowdown at This Recession Resistant Company originally appeared on Fool.com and is written by Lee Samaha.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.