While Chevron might win by a nose if you simply want to buy the stock, Exxon is very desirable for a leveraged trade through the use of call options. It comes down to this: stock buybacks only have one purpose, which is to increase the value of the stock through shrinking the outstanding share count. Presently, Exxon is repurchasing $20 billion in stock every year, or 5% of the outstanding count. Two years into the future, this should shrink the count by a further 10%. With the stock trading at the bottom of its long-term valuation in terms of cyclically adjusted P/E or price/sales, it is very hard to imagine how this price will not rise, unless two years from now the economy is in very dire straits.

While natural gas prices have been harmful to both Exxon and Chevron, these prices seem to have bottomed recently. With oil trading about where it has been for the last several years and natural gas trending up, there should be no negative surprises in store unless the economy takes a turn for the worse.

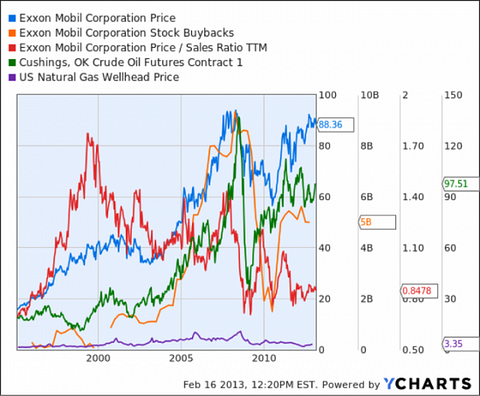

Figure 5: ExxonMobil Price, Repurchases and Price to Sales

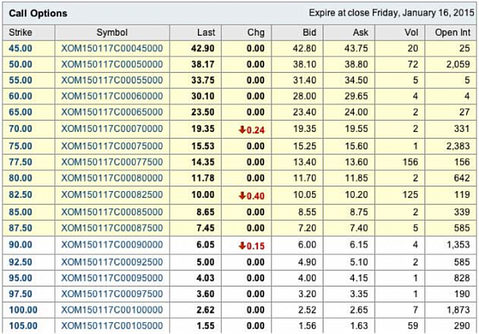

As a result of their repurchase program, I would argue that long-dated calls on Exxon are dramatically underpriced. Purchase of a $70 Jan 2015 call delivers a breakeven price of $89.45 or 1.1% above where the stock is presently trading. In other words, the owner of 100 shares of Exxon is willing to sell you his upside minus the 2.5% dividend, or a 4.5:1 levered trade at a cost of 3.1% per year.

A $75 Jan 2015 call would have a breakeven of $90.42 or 2.3%, a 5.7:1 levered trade at a cost of 3.7% per year. Because Exxon pays most of its shareholder remuneration in repurchases, dividends you will recieve the full value of the share repurchases, although it is possible the market will not efficiently price it in. Consider that if there is no growth in Exxon’s earnings, a 10% reduction in share count and the same valuation a purchaser of the $75 Jan-2015 call would expect a 50% return by Jan-2015. With Exxon still near its lowest price to sales valuation in 20 years, this wager appears very desirable in terms of risk vs. reward.

Figure 6: Options Chain for ExxonMobil

Another interesting part of this strategy is that you cannot lose more than the value you paid for the option, thus instead of buying 100 shares of Exxon for $8,900, you could buy one contract for $15.45 and invest the rest in bonds. Your maximum loss would then be 16.7% no matter how badly the market declines and you would expect all the upside for holding 100% of your portfolio in stocks, depending of course on how Exxon performs relative to the market. Because the contract is dated two years out and the average bear market lasts 1.5 years, it is likely that even if you bought the call and a bear market started immediately you would recoup some of your capital before the contract expires in 2015.

The options strategy is therefore an interesting idea for limiting losses while keeping pace should the present bull market continue. Otherwise, you could simply buy the stock and know that eventually Exxon should do quite well: higher prices are simply inevitable with the share count shrinking by 5% each year and the some of the lowest valuations in the past 20 years excluding 2008-2009. Collecting a 2.6% dividend while you wait isn’t too shabby either.

The article 5 Undervalued Major Oil Companies: But Which Will Be a Gusher for Your Portfolio? originally appeared on Fool.com and is written by Brendan O’Boyle.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.