Introduction

The 5 MLPs covered in this article offer yields ranging from 5.7% to 10.7%. Additionally, each of these MLPs appears reasonably valued given their high yields and prospects for growth. However, two of these MLPs are currently in the process of merging.

MLPs Simple and Complex at the Same Time

I believe that MLPs represent an investment choice that is a conundrum of sorts. In some ways, MLPs are very simple investments. They are primarily income generating vehicles that typically produce higher yields than most other investment choices. Furthermore, as a general rule, best-of-breed MLPs have a history of increasing their distributions each year. Therefore, investing in MLPs is primarily about the dividend income, or more precisely stated, the “income distributions” that they offer unit holders. On the other hand, many best-of-breed MLPs have also proven themselves to be excellent capital appreciation generators over the long term as well.

photofriday/Shutterstock.com

But there is also a lot of complexity associated with investing in MLPs. They have complex capital structures and many have general partner relationships that do not always favor public unit holders. Therefore, each prospective individual MLP investor should also carefully examine the partnership agreements between the general partners and limited partners. These agreements will also cover the distributable cash flow levels to include discretionary reserves mandated by the general partner.

In this same regard, there also tax considerations associated with investing in MLPs. As long as the MLP is deriving 90% or more of their income from qualifying sources, there is no tax at the entity level. Furthermore, unit holders are offered tax benefits on their distributions because a portion is considered return of capital. However, the return of capital portion also reduces the unit holder’s basis in the units.

As a result, unit holders must deal with a K-1 each year and keep track of their cost basis. This tax pass-through status is generally considered a benefit, but it also comes with additional complexity. MLPs also provide challenges to tax advantaged accounts such as IRAs because partnership income can be considered unrelated business taxable income and subject to unrelated business income tax (UBIT) if it exceeds $1000 a year. There is also estate planning tax considerations that investors must consider.

With the above said, I want to be clear to the reader that I am not an expert in investing in MLPs. However, I do believe I have something to offer that is often overlooked by investors regarding investing in MLPs. In talking with individual investors about MLPs, I have discovered that few are aware of the amount of dilution associated with investing in MLPs.

MLPs are constantly issuing more shares (units) which dilute existing unit holders, but raises much-needed capital to fund growth at the same time. For the MLPs covered in this article, this additional capital has been the source of significant revenue increases. These increased revenues allow the MLPs to continue to increase distributions in spite of the heavy dilution.

MLPs Simplified

For those readers not fully versed in MLPs, I offer the following links to the educational section of Alerian an independent provider of master limited partnership products and exchange traded funds. The first is titled MLP 101 and the second is titled MLP 201. These links will provide a basic education on MLPs. I also offer the following info graphic from the same website that simplifies MLPs and how they function.

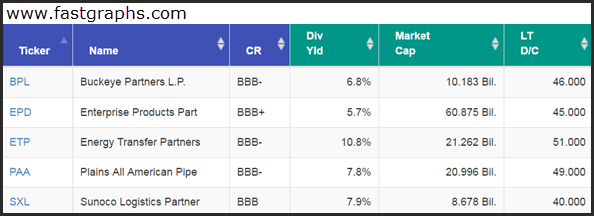

5 Fairly Valued MLPs

The following FAST Graphs’ summary lists 5 MLPs that I considered fairly valued in alphabetical order. As previously mentioned, Energy Transfer Partners LP (NYSE:ETP) and Sunoco Logistics Partners L.P. (NYSE:SXL) have entered into a merger agreement providing for the acquisition of ETP by SXL as a unit for unit transaction. My rationale for including these as separate entities prior to the merger is to cast a light on the complexities and challenges often associated with investing in MLPs. Limited partner unit holders are often at the mercy of controlling general partners.

In this case there is a third entity, Energy Transfer Equity LP (NYSE:ETE) that owns the general partner and 100% of the incentive distribution rights (IDRs) of Energy Transfer Partners LP (NYSE:ETP) and Sunoco LP (NYSE:SUN). This is offered simply to illustrate the complexity of investing in MLPs. Unlike investing in traditional companies, it’s important to not only analyze the specific MLP under consideration, it’s also critical to understand and analyze the general partner and all of its parts.