I noted back in mid-August that these stocks looked ripe for deeper drops, and that prediction has surely happened. This whole industry is the epitome of “dead money,” with a range of headwinds that will likely keep them in the investor doghouse for quite some time to come.

Still, it’s useful to take an end-of-quarter look at the crop of recent losers. Though some stocks surely deserve the thrashing they’ve received over the past three months, others have only been temporarily pushed out of favor and now represent deep value. The key is to look at what drove the sell-off and how soon management can stabilize the ship.

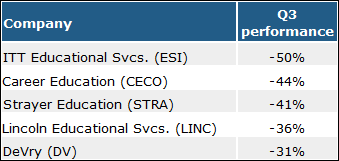

Here are the 20 biggest losers in the third quarter. All of these companies are members of the S&P 400 (mid-caps), S&P 500 (mid and large caps) or the S&P 600 (small caps).

Third-Quarter Losers

Questcor Pharmaceuticals, Inc. (NASDAQ:QCOR) is the quarter’s biggest loser and is unlikely to rebound any time soon. Shares may have been tempting for bottom-fishers after dropping in mid-September on news that health insurer Aetna Inc. (NYSE:AET) would limit reimbursement coverage for its $23,000 Acthar drug to just one type of treatment — infantile spasms. Yet when it eventually became apparent that the Food and Drug Administration was looking at Questcor’s possible wrong-headed marketing practices, this truly became a stock to shun. Such FDA investigations rarely end well.

A few pegs down the list you’ll find RadiSys Corporation (NASDAQ:RSYS), a provider of software and services to the wireless communications sector, that has seen its stock fall from $10 to just $3 in the past two years. The company just announced plans to replace its CEO in tandem with lowered third-quarter sales guidance (which will now likely be around $65 million instead of the previously guided range of $66 to $72 million.)

Despite the weak outlook, this stock is beginning to hold deep value for patient investors. The price to sales multiple is now below 0.5 — quite low for a company with a fair mix of high-margin software in the sales mix, and when the wireless telecom equipment markets stabilizes, earnings could move back north of 50 cents per share — either in 2013 or 2014. Shares trade for around six times that outlook.

A trucker’s rebound?

In late August, I noted that trucking firm Arkansas Best Corporation (NASDAQ:ABFS) had been dogged by a recent legal verdict in favor of the Teamsters union. At the time, I noted that the sell-off may have been overdone as Arkansas Best appeared poised for rising profits, despite those labor challenges. Well, shares have fallen another 10% since then, perhaps due to a factor I cited in late August: “Arkansas Best is in the midst of shaking out its current base of shareholders. Once that process is complete, value investors are likely to take note and send the stock higher.”

Is that still the case? I think so. That’s because the company is valued at just $200 million, but has tangible book value of $300 million. And although analysts have trimmed their 2013 earnings forecasts from $1.20 a share back in July to a recent 90 cents a share, the even larger share price drop (on a percentage basis) means that the forward price-to-earnings (P/E) multiple is now just nine. I still think that Wabash National Corporation (NYSE:WNC) is the best play in the trucking sector, as I noted here, though Arkansas Best also looks to have solid rebound potential.

A market share gainer

After falling from $70 at the start of the third quarter to around $50 by late August, I saw clear rebound potential for Coinstar, Inc. (NASDAQ:CSTR).

Well, shares have fallen another $5 to a recent $45. Investors are apparently taking a wait-and-see approach to the company’s imminent launch of a video-streaming service to rival a similaroffering by Netflix, Inc. (NASDAQ:NFLX). Management is likely to shed a lot more light on the economics of the service when quarterly results are released on Oct. 25.

As I’ve noted on a few occasions in the past, Coinstar has a multi-year history of a rising tide of doubters about its business model. And management has invariably delivered financial results that are handily better than what the company’s detractors usually predict. So this stock gets repeatedly beaten down and then rises anew. The current beatdown looks like a chance for Coinstar to surpass increasingly low expectations.

Risks to Consider: These stocks have tumbled in an otherwise strong quarter, so if the market softens in the fourth quarter, then these stocks may be hard-pressed to rebound in the near-term.

Action to Take –> In most instances, the bad news for these stocks is priced in. The key is determining which are likely to just sit at current depressed levels and which ones are poised to rebound.

It helps to focus on value in making your assessment: RadiSys, Arkansas Best and Coinstar all trade for less than 10 times projected 2013 profits, well less than the broader market multiple of around 13. Also of note is that 2012 earnings per share for all three are expected to be solidly above 2012 results. That’s a key factor to consider when looking for rebound candidates, and it makes all three worth considering.

This article was originally written by David Sterman, and posted on StreetAuthority.