So far The Ultimate Dividend Growth Portfolio contains 11 stocks, but none them except The Western Union Company (NYSE:WU) are financial companies. Some degree of diversification is a good idea in a portfolio like this, so today I’ll add three banks stocks that have promising dividend growth potential. Many banks were forced to cut or suspend the dividend during the financial crisis and some have yet to reinstate a reasonable dividend. But there are a few bank stocks that meet the criteria to be included in the portfolio.

![]()

A bank is an entirely different animal than a normal company, and valuing one can be a lot more difficult. People sometimes use the book value as a proxy for how cheap the stock is, arguing that a bank selling for below the book value is undervalued. But it’s not quite this simple. Recently Warren Buffett was on CNBC and responded to a question regarding banks:

Well, a bank that earns 1.3% or 1.4% on assets is going to end up selling above tangible book value. If it’s earning 0.6% or 0.5% on asset it’s not going to sell. Book value is not key to valuing banks. Earnings are key to valuing banks. Now, it translates to book value to some extent because you’re required to hold a certain amount of tangible equity compared to the assets you have. But you’ve got banks like Wells Fargo and (NYSE:WFC) USB that earn very high returns on assets, and they at a good price to tangible book. You’ve got other banks … that are earning lower returns on tangible assets, and they’re going to sell — they’re going to sell [for less].

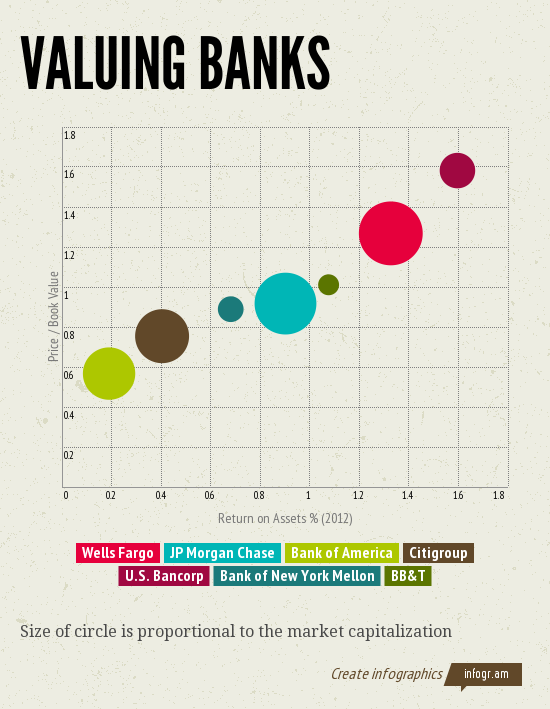

So earnings are the key, and the return on assets is a useful gauge of the quality of the bank. A sub-par bank in terms of earnings deserves a low P/B ratio, and an exceptional bank deserves a high P/B ratio.

Data from Morningstar

The general trend in the chart above shows that the higher return on assets that a bank earns the higher the P/B ratio. So simply buying banks with low P/B ratios means that you’re buying lower quality banks, not that the banks are necessarily undervalued.

Of course, since I’m looking for stocks to add to The Ultimate Dividend Growth Portfolio the dividends paid by these banks is the main factor. The bank with the highest ROA, U.S. Bancorp (NYSE:USB), pays a respectable dividend with a 2.35% yield, but the yield is too low compared to the other choices. Bank of America Corp (NYSE:BAC) and Citigroup Inc (NYSE:C) both pay only token $0.01 dividends, so they’re obviously out of consideration. And The Bank of New York Mellon Corporation (NYSE:BK), like U.S. Bancorp (NYSE:USB), has too low a yield at just 2.15%. So we’re left with the remaining three: Wells Fargo & Co (NYSE:WFC), JPMorgan Chase & Co. (NYSE:JPM), and BB&T Corporation (NYSE:BBT).

Wells Fargo & Co (NYSE:WFC)

Wells Fargo & Co (NYSE:WFC) is Warren Buffett’s favorite bank, and for good reason. Of the four largest banks, Wells Fargo & Co (NYSE:WFC) enjoys the highest return on assets and only trades for around 11 times earnings. The dividend, which has been raised twice within the last six months, now yields 3.17%. The next ex-div date is May 8, so I’m adding Wells Fargo & Co (NYSE:WFC) just in time to receive that dividend.

Like many companies Wells Fargo & Co (NYSE:WFC) was forced to cut the dividend due to the financial crisis. The cut was drastic, but since then the dividend has grown from $0.05 per share quarterly to $0.30 per share quarterly. With an EPS of $3.36 in 2012 the projected payout ratio is just 35% – before the financial crisis this number was closer to 50%. This suggest that the company has room to grow the dividend independent of earnings growth, and that the dividend should grow at an accelerated rate over the next few years.

The company’s first quarter results were positive, with EPS growing 22.7% year-over year on slightly lower revenue. The upcoming quarterly dividend was boosted by 20% over the previous dividend, which itself was boosted 13.6% over the dividend before that. The average analyst estimate for 5-year annual earnings growth is about 8%, so I expect the dividend to grow at least that quickly and very likely faster due to the low payout ratio.

Based on the current market price I will add 132 shares of Wells Fargo & Co (NYSE:WFC) to The Ultimate Dividend Growth Portfolio with a total cost basis of $5,000.16. The projected annual dividend payment for this position is $158.40.

JPMorgan Chase & Co. (NYSE:JPM)

JPMorgan Chase & Co. (NYSE:JPM) is a bit lower down on the chart than Wells Fargo but still leaves both Bank of America Corp (NYSE:BAC) and Citigroup Inc (NYSE:C) in the dust. Although the London Whale incident, which caused multi-billion dollar losses last year on derivative bets, may have given reason for pause, the bank recorded over $21 billion in net income in 2012, growth of 12% from 2011. And the first quarter of this year saw further earnings growth of 21% year-over-year.

Like Wells Fargo, JPMorgan Chase & Co. (NYSE:JPM) was also forced to cut the dividend during the financial crisis. Since then the quarterly dividend has grown from $0.05 to $0.30, and the dividend payment going ex-div in July has been boosted by another 26.7% to $0.38 per share. This puts the projected dividend yield at 3.11%. It seems like we’ve reached a point in the recovery where the best performing big banks are comfortable raising there dividends significantly.

With an EPS of $5.20 in 2012 the projected payout ratio is just 29%, even lower than that of Wells Fargo. And with analysts predicting 7% annual earnings growth I think that we will see some serious dividend hikes in the near future.

Based on the current market price I will add 102 shares of JPMorgan Chase & Co. (NYSE:JPM) to The Ultimate Dividend Growth Portfolio with a total cost basis of $4,983.72. The projected annual dividend payment for this position is $155.04.

BB&T Corporation (NYSE:BBT)

With the big banks tapped out in terms of dividend growth prospects, I’ll now turn to a much smaller bank, BB&T Corporation (NYSE:BBT). BB&T Corporation (NYSE:BBT) has only $184 billion in assets compared to the $2 trillion or more held by the larger banks, but its return on assets is higher than all but Wells Fargo. BB&T Corporation (NYSE:BBT) operates about 1,800 locations in 12 states and has grown its asset base by roughly 21% since 2008.

While BB&T Corporation (NYSE:BBT) saw earnings growth of 53% in 2012 the first quarter of 2013 was disappointing, with net income shrinking by 44%. However, this decline was due to a one-time charge involving a disputed tax liability, and without this charge EPS actually grew by about 13%.

BB&T Corporation (NYSE:BBT) currently pays a dividend yielding 3.01% after a dividend hike of 15% earlier this year. The payout ratio, based on 2012 EPS, is 34%, about the same as Wells Fargo. Pre-financial crisis the payout ratio was around 50%, so BB&T Corporation (NYSE:BBT) has room to grow the payout ratio. Analysts expect 8.3% annual earnings growth going forward, so dividend growth should be significant.

Based on the current market price I will add 163 shares of BB&T to The Ultimate Dividend Growth Portfolio with a total cost basis of $4,982.91. The projected annual dividend payment for this position is $149.96.

14 down, 6 to go

With these three banks The Ultimate Dividend Growth Portfolio now has 14 positions and about $30,000 in cash left. You can track the state of the portfolio at any time by going here. The portfolio has already seen two dividend increases since its inception from Apple Inc. (NASDAQ:AAPL) and Corning Incorporated (NYSE:GLW), and I expect to see many more as time goes on. Until next time, here’s what the portfolio looks like as of this writing.

The article 3 Banks for the Ultimate Dividend Growth Portfolio originally appeared on Fool.com and is written by Timothy Green.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.