Weight Watchers International, Inc. (NYSE:WTW) has been shedding market cap faster than clients drop pounds. Since the fourth quarter of 2012, it’s been a story of disappearing subscribers and slowing growth for this membership-driven weight loss service.

Weight Watchers International, Inc. (NYSE:WTW) rose from its zombie–like performance in 2008-2010 to dazzle the market with lively growth in 2011 and a subsequent resurrection of its market cap and its price. The growth was short lived, and 2012-2013 numbers show a disappearing membership base, especially in the critical North American market.

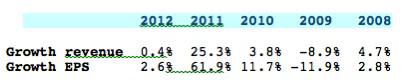

As revenue growth flat lined with lower earnings and guidance, Weight Watchers International, Inc. (NYSE:WTW) has taken a turn for the worse, and the stock is heading toward three-year lows. The measure Weight Watchers International, Inc. (NYSE:WTW) uses to track success is a number known as total paid weeks. The paid week report is the total of monthly and pay-as-you-go member payments for a reported time period, typically annual and quarterly. When members join up either at meetings or online, these numbers go up. When the company loses members, it goes down.

Paid meeting weeks for North America dropped 5.6% in 2012, along with a decrease of 11.5% in the U.K. Together, these two geographic bases account for 84% of meeting paid weeks–North America alone is 67%. When 84% of a business is underperforming, it’s going to get the market’s attention, and not in a positive way.

The company’s reversal of fortune in 2012- 2013 followed its brief recovery during the back half of 2010 and 2011. Paid weeks increased 26.4% and attendance was up 18.8%. A marketing campaign with Jennifer Hudson as spokesperson and ads that focused on member experience succeeded, driving huge membership gains. Unfortunately, enrollment is now dropping fast, and management blames the loss of members partially on the proliferation of nutrition/weight loss apps that are available either for free or at modest prices.

Business continued to deteriorate in Q2 2013, with North American paid weeks down 10% and member attendance off by 14.5%. Volume is expected to drop by the mid-to-high teens, percentage wise, for the second half of 2013. The UK business was worse, with paid weeks down 19% and the expectation of a second half decline in the mid-to-high 20% range. Margins are expected to contract as spending deleverages with flagging top-line growth. The company has even offered guidance for 2014 — the meeting base will start lower than 2013.

There’s an app for that

If you type in “free weight loss apps,” Google will give you 79 million results in 2.3 seconds. The first page has one of the most popular – MyFitnessPal. It has a free calorie counter and an online diet and fitness community, all completely free, and claims to have 40 million members. Consumers can do it for themselves and at no cost. That’s a powerful threat to Weight Watchers International, Inc. (NYSE:WTW)’s monthly charges for membership; the company’s online program costs $18.95 per month. MyFitnessPal just reeled in venture backing to the tune of $18 million, giving it the potential to become an even more pervasive force in the weight loss niche.

Smart phones give consumers dozens of free options that include calorie counters, calorie consumption by activity, and effective workout routines. Weight Watchers International, Inc. (NYSE:WTW) has conceded slow growth with heavy mobile app adoption in the near-term stealing its market, but also expects members will come back to the organized supportive meeting structure it provides.

From the Q2 conference call, according to Nicholas P. Hotchkin, CFO:

Since we last gave guidance, what we’ve seen is a deteriorating trend in recruitments, particularly on our online business and we feel that some of that is driven by the continued sudden explosion of interest in free apps and activity monitors.

One thing I want to stress, Glen, as we look to ’14, we’ve discussed that the issue with free apps is they’re taking trial out of the market. We view that as a temporary phenomenon because we know that our program works. We believe, as Jim has said, in the science behind our program.

Weight Watchers has survived the Atkins diet, The South Beach Diet and the countless fads that come and go in the weight-loss world. Calorie counting apps with online communities that do what Weight Watchers does (and for free) may prove to be more challenging.

What other businesses could fall victim to killer apps?

Garmin Ltd. (NASDAQ:GRMN) is in the global positioning business, using satellites to pinpoint a user’s exact location. Garmin Ltd. (NASDAQ:GRMN)’s biggest market segment is car/mobile, and even with slow erosion of the car/mobile business over several years, it’s still 50% of the company’s business. Between 2010 and 2012, mobile lost 11% of its revenue and in Q2 2013 mobile dropped 12%. This is largely due to the proliferation of mobile devices that all support GPS apps-free and otherwise. Stand-alone GPS can’t compete with the convenience of calling up an app on the phone and getting directions. Consumers can buy a cheap dashboard or windshield mount and plug in the smart phone with plenty of apps providing superior updated traffic info, maps and directions. Smart phone use is now estimated at 47% of navigation app usage.

Garmin’s growth

Let’s eat out

OpenTable Inc (NASDAQ:OPEN) hasn’t suffered much yet from a fast-expanding menu of reservation websites and apps, but it may be next on the hit list. However, the model is different than the Weight Watchers dilemma–it’s paid for by restaurants and not by the diner/consumer. That doesn’t mean the growing universe of mobile devices and apps won’t make life harder and more expensive for the company.

OpenTable Inc (NASDAQ:OPEN) sells reservation management to around 28,000 restaurants worldwide. The company sets a client up for a fee with hardware and software, and charges clients a monthly fee per reservation. In an attempt to stay competitive, OpenTable recently acquired Rezbook to broaden its client base, add mobile apps, and take on the competition.

OpenTable’s Q2 revenue was disappointing — $45.7 reported, compared to $46 million expected by analysts. The company guided to third quarter earnings at $0.38 to $0.42, well below the $0.48 analysts were looking for, and cited spending on mobile marketing and development as partially responsible for the shortfall. It’s eat or be eaten, and OpenTable needs to move fast and spend hard to stay ahead of the competition.OpenTable is investing aggressively in mobile apps for reservations against competition that is equally motivated to win the space.

Yelp Inc (NYSE:YELP) will acquire Internet and mobile reservations service SeatMe, an OpenTable competitor, for around $12.7 million. SeatMe technology provides easy, online reservations directly through Yelp Inc (NYSE:YELP) rather than through current partner OpenTable. It’s a battle in reservation territory for consumers, and ease of use with catchy mobile apps will win the war.

Bigger chains with deeper pockets are apt to develop their own mobile apps. The TGI Fridays app pays your bill, gets you to the closest restaurant, lists specials, and lets you browse the full menu all from a smart phone. While OpenTable and Yelp’s SeatMe will be able to catch business from thousands of small restaurants, the larger chains may go it on their own, siphoning off profits from big accounts.

Mobile apps are changing the way the world does business and has the capability of crippling some businesses or even putting some on the endangered species list.

The article Killer Apps Are Attacking these Companies originally appeared on Fool.com and is written by Jean Graham.

jean graham has no position in any stocks mentioned. The Motley Fool recommends OpenTable. The Motley Fool owns shares of Weight Watchers International (NYSE:WTW).

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.