Surviving as an apparel retailer over the past decade hasn’t been easy. Many struggling companies in the industry have yet to fully recover from the blow of the Great Recession, while others have bounced back, soaring to new heights. “Action apparel” retailer Zumiez Inc. (NASDAQ:ZUMZ) – which specializes in skating, snowboarding and surfing apparel and gear – walks a thin line between those two categories.

After plunging from $51.25 to $6.43 per share between October 2007 and March 2009, the company clawed its way back to current levels, and it may still have room to grow. Is Zumiez a budding growth stock in a tough industry, or is investing in it a risky extreme sport of its own?

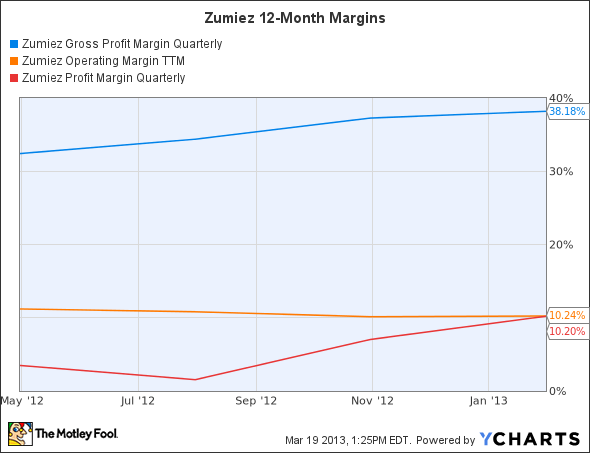

Fourth Quarter

For its fourth quarter, Lynnwood, Washington-based Zumiez earned $0.74 per diluted share, a 22.1% increase from the prior year quarter – beating expectations by a penny. Revenue also rose 22.1% to $224.4 million, beating the consensus estimate of $223.4 million. Revenue growth notably outpaced inventory growth – a positive sign that products are being sold at a brisk pace.

For the full year, Zumiez Inc. (NASDAQ:ZUMZ)’s revenue rose 20.4% to $669.4 million, while its profit rose 12.9% to $42.2 million.

Zumiez attributed it robust growth to the addition of 56 new stores throughout the fiscal year. However, weak same-store sales dampened the optimism sparked by its top and bottom line growth.

Sales and Margin Growth

During the fourth quarter, Zumiez’s same-store sales slid 1.0% – a bleak drop from the growth of 8.7% it reported in the prior year quarter. For the full year, same-store sales rose an average of 5.0%.

The company noted that although its total number of paying customers declined, each customer purchased a higher number or products per transaction. The company was also able to raise its prices, which helped it strengthen margins without adversely impacting existing sales volume – meaning that it has pricing power, thanks to its niche market.

While that factor suggests margin growth, Zumiez Inc. (NASDAQ:ZUMZ)’s operating margin actually declined 8.56% year-on-year as gross and profit margins rose.

Usually a decline in operating margin points to operational inefficiencies, but Zumiez attributed the dip to an increase in its expenses related to the fulfillment of orders at its Blue Tomato online retailer, the European e-commerce business which it acquired last year for $75 million.

I think Zumiez’s hefty payment for Blue Tomato was justified, considering that the company’s e-commerce segment, including Blue Tomato, posted a sales increase of 22% from the prior year quarter. Total e-commerce sales accounted for 8.3% of annual revenue in fiscal 2012, up from 1.0% five years ago.

Most importantly, without the addition of its e-commerce sales, same-store sales growth for the quarter would have been negative.

Rising Expenses

Speaking of expenses, Zumiez Inc. (NASDAQ:ZUMZ)’s SG&A (sales, general and administrative) expenses rose 23.4% year-over-year. As a percentage of total revenue, they increased to 22.1% – slightly up from 21.9% last year.

Again, most of these expenses were attributed to web operation costs for Blue Tomato. During the quarter, charges from the Blue Tomato acquisition cost an estimated $7.3 million. An additional $2.1 million was spent on relocating its corporate offices to Lynnwood, and moving its e-commerce fulfillment center to Edwardsville, Kansas.

However, most of these costs were offset by lower fixed costs, such as a slight decline in occupancy costs for its brick and mortar business.

But a look back at the past three years reveals that Zumiez’s rising expenses are a continuation of a longer-term trend, which is worrisome due to its decreased cash and short term investments position. At the end of the fourth quarter, Zumiez’s cash position plunged 40.3% from $172.8 million to $103.2 million, as a result of Blue Tomato, increased capital expenditures and stock repurchases.

Zumiez Inc. (NASDAQ:ZUMZ) bought back 1.3 million shares of stock for approximately $25.8 million. I firmly believe that the company could have scaled back on stock buybacks to beef up its cash reserves. However, its free cash flow remained at a healthy $66.2 million, which means that its cash won’t dry up anytime soon.

A Soft Outlook

For the current quarter, Zumiez expects to earn 4 to 7 cents per diluted share, on revenue of $141 million to $144 million. Additional costs from Blue Tomato are expected to reduce diluted earnings by $1.5 million, or 4 cents per share. The company’s forecast missed the analyst consensus of 13 cents per share on $145 million in revenue.

Aggressive Expansion

At the start of March, Zumiez operated 472 stores in the United States, with 21 in Canada and eight locations in Europe, for a total store count of 501.

Despite its soft guidance for the current quarter, Zumiez Inc. (NASDAQ:ZUMZ) intends to add 60 new stores in fiscal 2013, including ten namesake stores in Canada and six brick and mortar Blue Tomato locations in Europe.

Although new locations will boost revenue growth going into fiscal 2013, expenses will continue to rise as cash reserves decline. Costs from maintaining and expanding Blue Tomato will also weigh on its bottom line, especially if same-store sales growth trends into negative territory.

The company has a lofty goal of 600 to 700 global locations, which means that expenses and capital expenditures will keep increasing over the next several quarters.

Crushing the Competitors

Zumiez Inc. (NASDAQ:ZUMZ) competes with Quiksilver, Inc. (NYSE:ZQK) in the surfing department, Pacific Sunwear of California, Inc. (NASDAQ:PSUN) in surf and skate apparel, and Australian company Billabong, which offers snow, surfing and skating apparel.

The chart below simply shows that Zumiez is crushing these market rivals.

| Forward P/E | Price to Sales (ttm) | Return on Equity (ttm) | Debt to Equity | Profit Margin | Qty. Revenue Growth (Y-O-Y) | Qty. Earnings Growth (Y-O-Y) | |

| Zumiez | 13.09 | 1.12 | 14.65% | 1.98 | 6.30% | 22.10% | 22.10% |

| Quiksilver | 19.48 | 0.54 | -3.29% | 133.55 | -0.97% | -4.10% | N/A |

| Pacific Sunwear | N/A | 0.20 | -53.67% | 89.58 | -8.30% | 0.70% | N/A |

| Billabong | 12.00 | 0.29 | -117.03% | 49.97 | -59.94% | -8.10% | N/A |

| Advantage | Billabong | Pacific Sunwear | Zumiez | Zumiez | Zumiez | Zumiez | Zumiez |

Source: Yahoo Finance, 3/20/2013

Zumiez is the only one of these “action sports” apparel retailers that is even profitable. Its top and bottom line growth is well ahead of its peers, and it has the lowest debt and best past performance of the bunch. Zumiez’s P/E ratio is also far lower than the industry average of 17.40 – making it fit my three favorite words in the stock market: an

undervalued growth stock

.

The Bottom Line

Although Zumiez’s fundamentals are strong, let’s not get ahead of ourselves. While rapid expansion could fuel equally rapid revenue growth, expenses must stay in check.

First, the company should cool it with the stock buybacks – that’s what mature companies, not growing ones, do.

Second, it should reevaluate the need for a brick and mortar expansion, especially into debt-straddled Europe, considering the robust growth of its online business. Plenty of retail companies, such as Lululemon Athletica inc. (NASDAQ:LULU), have flourished on a large online presence complemented by a limited brick and mortar footprint. Yet make no mistake – Zumiez is growing, and it could still be a long-term winner.

The article Is Zumiez Ready to Zoom? originally appeared on Fool.com and is written by Leo Sun.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.