Q1 review

The content streaming company managed to post earnings of $0.31 per share compared to a loss of $0.08 a share in the same quarter last year. Earnings came in above analyst estimates of $0.19 per share.

For Q2, Netflix expects earnings to be in the range of $0.23 per share to $0.48 a share, compared to analysts’ estimates of $0.30.

B. Riley upgraded the company from sell to neutral after the announcement. Raising its price target from $90 to $165, suggesting over 20% downside from current levels. S&P maintained its hold rating on stock, moving its price target to $225, suggesting upside of just over 6%.

The negatives

Netflix’s industry has low entry barriers. Netflix, Inc. (NASDAQ:NFLX) will likely face increased competition, including more competitive pressures from the likes of Amazon.com, Inc. (NASDAQ:AMZN) and Google. These rivals, though relatively new, have the infrastructure and capital to continue causing problems for Netflix. As well, Time Warner’s HBO is becoming another popular competitor.

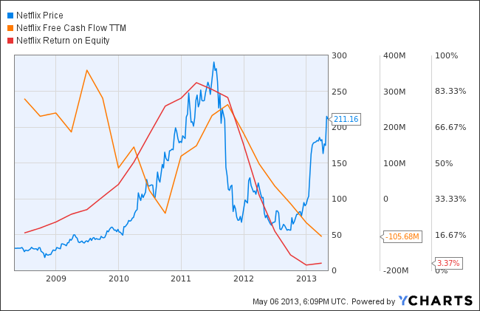

Another concern for investors should be the negative cash flow for three sequential quarters. For the most recent quarter (1Q), the company reported negative free cash flow of $42 million. The primary reason for negative cash flow is payments for original and non-original content.

Another key issue getting less attention is the weak performance in international markets. Netflix, Inc. (NASDAQ:NFLX) has still not been able to post a profit from its international operations, despite spending massive amounts on marketing and content licensing. International expansion and content additions resulted in cost escalations in the form of technology investments, up 27% year over year in 2012. Meanwhile, marketing expenses were up over 20% year over year in 2012.

The loss from Netflix’s international streaming business widened from $103 million in 2011 to $389 million in 2012. This loss was related to rising content licensing costs. Netflix, Inc. (NASDAQ:NFLX) also has a current total of $5.6 billion to be paid for streaming content obligations, out of which $2.29 billion needs to be paid within the next twelve months.

Netflix’s bonds also have a junk rating at double-B minus by Standard & Poor’s. Though, individually this does not look that bad, if one sees the junk rating along with rising content cost, negative cash flow, and increased competition, the rating looks menacing. A recent report from Jefferies downgraded Netflix, citing concerns over high costs associated with securing content and profit margins.

Robust competition

Amazon.com, Inc. (NASDAQ:AMZN) is one of Netflix’s biggest rivals currently. Both companies have a similar P/B ratio, Netflix at 14.8 and Amazon at 13.6, but that’s where the similarities end. Coinstar, Inc. (NASDAQ:CSTR) is a smaller company compared to these two giants and poses less of a threat. Although Amazon’s valuation is very “rich” too, I take solace in the fact that the company has a strong product portfolio and geographical mix.

Amazon started out as a book e-retailer, but now sells a diversified mix of products. Its North America segment generates around 57% of revenue, while international accounts for 43%. Meanwhile, its product mix includes 33% of revenue from media, 63% from electronics and other general merchandise, and other making up 4% of revenue.

As well, unlike Netflix’s struggles with generating strong free cash flow, Amazon.com, Inc. (NASDAQ:AMZN) is performing nicely in this respect. Which is in part thanks to its flexible cost structure, allowing the company to curtail technology and content expenses when margins are impacted by discounts and promotions to boost sales. Amazon’s quarterly revenue has been growing in double-digits. Cash flows grew 6.1% in 2010, 11.7% in 2011, and 7.1% in 2012.

The nice thing about Coinstar, Inc. (NASDAQ:CSTR) is its “hybrid” model, allowing users to either stream movies or pick up the actual disk from any of its many RedBox kiosks. Part of what makes the kiosk system work is its number of locations, allowing for convenience, whereas Netflix’s DVD business was time delayed (mail system). Coinstar, Inc. (NASDAQ:CSTR) also has its coin counting and coffee kiosks. Its coffee kiosks, Rubis, is expected to sell more than 10,000 cups per year per kiosk. Its traditional coin counters are gaining banking capabilities, thanks to a relationship with PayPal, which should be another long-term positive for the company.

Late last month, Coinstar posted Q1 EPS that beat consensus, but was still down year over year. The company posted EPS of $0.93, versus $1.39 for 1Q 2012, but above consensus of $0.86. Coinstar also guided second-quarter revenue between $555 million to $580 million, and core EPS of between $0.90 and $1.05. Meanwhile, analysts expected the company to post Q2 EPS of $0.99, which again, is still below year ago EPS of $1.25 for Q2 2012. However, given the valuation and expected growth (17.7% annualized five-year expected EPS growth rate) the company appears to be a solid growth at a reasonable price with a PEG ratio of 0.59.

Valuation

Netflix, Inc. (NASDAQ:NFLX) trades at an EV/EBITDA multiple of 89.7 times, while the other “expensive” stock, Amazon, trades at only 41.5 times, and Coinstar at 3.8 times. Netflix’s P/E ratio remains high, however, the potential growth doesn’t appear to justify the valuation.

With a P/E ratio of 517 times, Netflix is trading near the top of its five-year P/E range of 15 times to 570 times. Netflix also has a PEG ratio in excess of 8, while Amazon is at 5.15. What’s more is that while Netflix’s price continues to soar, it’s free cash flow generating capabilities and return on equity have been in steady decline.

Netflix has grown EPS at an annualized negative 7% over the last five years, and although the future is brighter, I don’t think it justifies a premium valuation to Amazon, nor a P/E in excess of 500 times.

Hedge fund trade

Going into 2013, there were a total of 58 hedge funds long Amazon. Billionaire Ken Fisher’s Fisher Asset Management had the largest position by market value in the company, worth $613 million (see Fisher’s dividend stocks). While Amazon had the maximum interest from hedge funds going into 2013, Netflix, Inc. (NASDAQ:NFLX) saw some of the best sentiment, having 30 hedge funds long the stock, which was a 30% increase from the third quarter. The largest position held was by billionaire Carl Icahn, with a $514 million position that made up 4% of his 13F portfolio (check out Icahn’s small cap picks).

Of the companies listed, Coinstar had the lowest hedge fund interest, with only 28 hedge funds long the stock at the end of 2012. This includes Marathon Partners and billionaire Jim Simons’ Renaissance Technologies (check out Simons’ high yielding picks).

Conclusion

The current momentum in Netflix, Inc. (NASDAQ:NFLX)’s stock is similar to the January 2010 and July 2011 rally the company experienced, with the stock crossing $250 to reach its all-time high of over $300, but eventually came crashing back to reality. The stock is already up over 125% year to date.

So, currently it looks like the bear case is greater than the bull scenario, with concerns over rising content acquisition costs, negative cash flow, and limited success in international markets should cause concerns for investors.

The article Why Netflix Is Too Rich for My Blood originally appeared on Fool.com and is written by Marshall Hargrave.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.