Netflix, Inc. (NASDAQ:NFLX) announced its fourth quarter fiscal results on Jan. 23, and the very next day its stock price jumped 42%. In the 10 trading days following results, the stock gained almost 80%.

It has been a dream run for Netflix in 2013 — the stock has appreciated almost 100%: from $92.59 on Dec. 31, it closed at $184.41 on Feb. 6. Is it driven by results and the company’s performance and future prospects? Will the company’s earnings be able to justify such high equity valuation? Or is it just news driven? Let’s have a look.

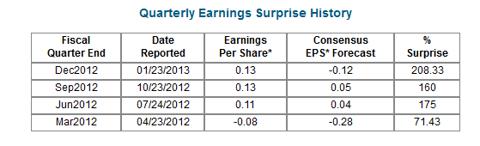

Earnings

Netflix reported quarterly revenue of $945.24 million for the period ended Dec. 31, which was 8% higher than the same quarter last year. However, revenue for the full year ended December 2012 was $3.6 billion, up by almost 13%.

Quarterly EPS for the fourth fiscal quarter fell to $0.14 from the $0.66 reported in the same quarter prior year. The drop in EPS for the full year was even more drastic, and fell from $4.28 to $0.31 per share.

However, quarter-oover-quarter EPS reveals a different picture.

Source: www.nasdaq.com

Netflix has been able to increase its subscriber base due to high spending on popular movies and shows. Streaming subscriptions increased by 9.74 million in 2012, with international subscriptions tripling to 6.12 million.

Netflix has belied theories that streaming will not be able to provide margins as good as those of the DVD business. Fact is that margins for domestic streaming business registered YOY improvement of more than 7%.

The drop in income is more from the drop in DVD business, which was an extremely high-margin business for the company. The increase in subscribers has not been sufficient for compensating losses due to the 26% decline in DVD subscriptions.

Future Prospects and Challenges

The negative cash flow is a big worrying factor. This can potentially lead to further borrowing or issuance of fresh equity if the company is not able to generate sufficient cash from operations to fund its expensive content deals.

The company expects streaming profits in the next quarter to be more than profits from the DVD business. This is something that has not happened before in the history of the company. CEO Reed Hastings said that he does not intend to raise the subscription rate from $7.99 per month, and instead will focus on increasing subscriptions to 50 million.

One of Netflix’s major competitors, Amazon.com, Inc. (NASDAQ:AMZN), has huge cash reserves and may beat it in the race to acquire new content. Amazon has a current cash flow of $4.18 billion cash and cash equivalents amounting to $8.08 billion. Comparable figures for Netflix are only $22.76 million and $290 million, respectively. Netflix, however, has a slightly better operating margin (1.39%) than Amazon (1.11%).

Another threat is presented by Redbox DVD rental machines from Coinstar, Inc. (NASDAQ:CSTR) and its partnership with Verizon Communications Inc. (NYSE:VZ). Coinstar is engaged in the business of providing convenient and automated retail solutions with major revenue coming from Redbox kiosks where customers can order or rent movies and games. Although it’s a smaller company as compared to Netflix in terms of market cap ($1.43 billion, compared to Netflix’s $9.96 billion), Coinstar has a much healthier operating profit of above 12%.

Verizon, on the other hand, is the country’s largest mobile carrier, a much bigger company with an enterprise value of $175.13 billion (against market cap of $127.05 billion). What makes it an even bigger threat to Netflix is that analysts expect it to grow 24% by December 2013. To make matters even more challenging for Netflix, Microsoft Corporation (NASDAQ:MSFT), which has been pushing hard to enter America’s living rooms, announced on Feb. 5 that it was partnering with Verizon for exclusive rights of offering the company’s Redbox Instant Video on its gaming consoles.

What goes in favor of Netflix, though, is that Redbox is still a beta service and Amazon owns only one-third of Netflix’s popular content. When I last checked in October 2012, Amazon required spending something like $1 billion-$2 billion to come at par and compete with Netflix.

There is room for all in this market, which is inherently ever-growing. In addition, the content licensing space is too fragmented and riddled with complex and conflicting rights and licensing. Netflix’s lack of a complete catalog of Hollywood movies is more or less compensated with other popular TV shows and videos.

Conclusion

Netflix’s most recent quarterly results reveal that it is basically a revenue play. If there are inferences to be drawn then, it is that the stock market has responded primarily to the increase in revenues and chosen to ignore the increase in content cost.

With time, content can only become more expensive and will be the biggest drain on profits. From 2008 to 2012, content acquisition and licensing costs have increased by as much as $1.4 billion, whereas gross margin has fallen from 33.3% to 27.3%. On the other hand, as compared to 2011, operating expenses in 2012 are up by 18.4%.

The potential for profit is there, but will take time for it to become a reality — investors need to watch incremental subscriber numbers because an increase in subscription rates is hardly likely. Only recently, Hastings burnt his fingers when he raised rates and was forced to back down after seeing a drop in subscriptions. Incremental increases in subscription rates, if at all, will take some time and are likely to be minimal.

Also of interest is the news that in December The Walt Disney Company (NYSE:DIS) entered into a multi-year licensing agreement granting Netflix exclusive rights for U.S. subscription television service for its first-run live-action and animation feature films.

Despite all this, valuation still remains a matter of concern. At $184.41, the stock is trading at 13.77 times book value and at an unbelievably high P/E ratio of 636.56. In my opinion the market is not considering factors like competition increasing in the future and the hurdles that Netflix will have to face while trying to increase revenues.

Despite analyst recommendations of holding the stock, if I was invested in Netflix I would get out at the first opportunity. At the same time, I would avoid being enamored by the dream run that the stock has had and stay away from it until it comes down and is realistically valued.

The article How High Can This Company Go? originally appeared on Fool.com and is written by Sujata Dutta.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.