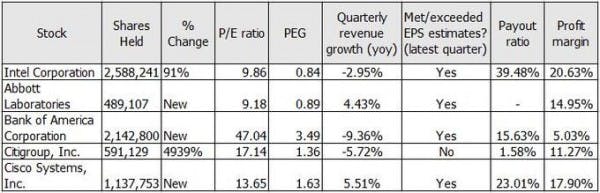

Todd-Veredus Asset Management (TVAM) is an investment adviser based in Louisville, Kentucky with $3.060 billion worth of assets under management as of Dec. 31, 2012. TVAM’s investment strategy hinges on price to intrinsic value being the most effective way to determine a stock’s true valuation. Its growth investment philosophy is to go for investments that have positive earnings surprises or estimate revisions. Let us look at this huge manager’s big buys for some ideas on a possible mix of stocks that we can consider. These are Cisco Systems, Inc. (NASDAQ:CSCO), Citigroup Inc. (NYSE:C), Bank of America Corp (NYSE:BAC), Abbott Laboratories (NYSE:ABT), and Intel Corporation (NASDAQ:INTC).

Sources: whalewisdom.com, finviz.com, and nasdaq.com, as of Feb. 11, 2013

Cisco Systems, Inc. (NASDAQ:CSCO)

![]()

Citigroup Inc. (NYSE:C)

The fund manager bought an additional 579,399 shares of Citigroup, bringing the stake to 0.76 percent of its portfolio. The stock price is going upwards quite robustly, thanks to its good growth prospects for the years ahead and the new plans it has set for cutting costs. It should be noted that Citigroup has failed to meet the consensus estimates in the latest quarter because it has been experiencing negative growth in its revenue. However, its valuation is pretty healthy as the P/E ratio is 17.14 and PEG is 1.36. Also, it is becoming less reliant on debt to finance its operations, which is an added plus. Since Citigroup is well situated within international markets and has a double-digit profit margin (ttm), I believe its growth prospects are huge.

Bank of America Corp (NYSE:BAC)

Todd Veredus initiated a $24.877-million position in Bank of America in the fourth quarter. The stock price is also rallying quite fast. Its recent success in exceeding the consensus estimates in terms of earnings has brought positivity to this company. Potential investors should remember, though, that the bank has been suffering from negative revenue growth recently with its profit margin found at the bottom of its competitors. Meanwhile, Bank of America is able to sustain its dividend payment of 1 cent per share since the company clearly has a bulk of cash, enough to cover this and perhaps more if it decides to increase the payment. Although I believe that BofA can develop momentum soon, I need a little more pushing to get as excited as Todd Veredus has been.

Abbott Laboratories (NYSE:ABT)

Abbott is a highly attractive company for a variety of reasons. It has a double-digit net margin, and the latest quarterly revenue report shows a positive growth of 4.44 percent. It has been exceeding consensus estimates in earnings for the last 4 consecutive quarters already, momentum that is indeed very impressive. Abbott has been relying less on debt for its business operations. It is one of the top dividend stocks with a payout ratio using cash flow of about 23 percent based on the third quarter 2012 data. The stock is undervalued; the P/E ratio is 9.14, while its PEG is only 0.88. Clearly this stock has a great value to it. Its growth prospects are high, with earnings expected to grow at an annual rate of 10.36 percent in the next 5 years. The outcome is for the spin-off of AbbVie is something to watch out for in the future.

Intel Corporation (NASDAQ:INTC)

The fund manager doubled its stake in Intel in the fourth quarter. The holding comprised 0.97 percent of the firm’s total portfolio. This company has a very healthy valuation with its P/E ratio of 9.86 and a PEG of 0.84. Intel has surpassed the consensus estimates in terms of earnings for the last 4 consecutive quarters. The company is really hot for its unwavering 20-something percent net margin. This top dividend stock has grown its annualized payment by an average rate of 12.5 percent in the past 4 years! With a sound financial standing and unparalleled profitability, your dividend income stream is safe and growing with Intel.

The list indeed provides a good mix of stocks to put on top of your grocery list. Most are on the upswing when it comes to value. But frankly speaking, I believe that BAC needs to bring more energy to the table to lure more investors to its side.

The article Consider These Big Buys by Todd-Veredus Asset Management originally appeared on Fool.com and is written by Aubrey Tabuga.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.