Other plans include a possible spinoff of its midstream operations as an MLP. Between its current profitability, the potential for increased net revenue from increased US oil purchases and a planned stock buyback, Phillips 66 looks like another US energy investment success story.

And then there’s SandRidge

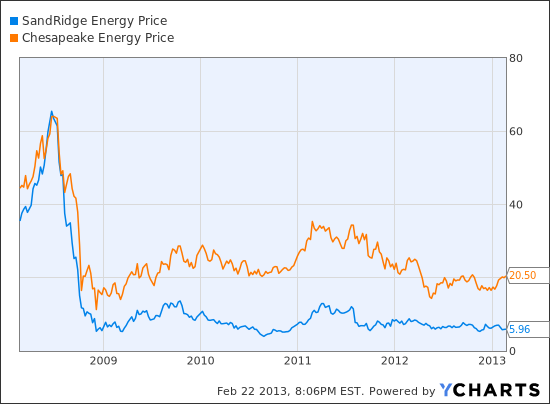

By now, most investors in US energy, particularly natural gas, know all about Aubrey McClendon and his shenanigans at

Chesapeake Energy Corporation (NYSE:CHK). Turns out, his Chesapeake co-founder, Tom Ward, has been doing similar shenanigans at SandRidge Energy Inc. (NYSE:SD).

For example, there’s Ward’s growing compensation, despite the near-80% decline of Sandridge stock since its IPO. The hedge fund firm TPG-Axon has provided more details regarding Sandridge’s recent activities here. Does anyone besides me see a parallel here between Chesapeake and SandRidge stock?

But the big financial stake poised over SandRidge’s heart is its new strategy in Mississippian lime in Oklahoma and Kansas. Simply stated, SandRidge sold known producing assets in the Permian Basin to concentrate on promising but unproven assets in the Mississippian Lime formation.

Two questions rear their ugly heads: First, how will SandRidge replace the significant Permian Basin revenue while exploration of the Mississippian Lime begins? Some believe the Mississippian Lime is a lower oil margin asset than the Permian Basin assets. Selling producing assets when your company suffers from poor earnings, negative cash flow and a heavy debt load strikes me as a bad move. Other analysts seem to agree, and project a loss in Q4 2012 and for 2013.

Second, just what is the Ward family’s interest in this Mississippian play? As the TPG-Axon presentations point out, there are several apparent conflicts of interest connected to this asset play. SandRidge has denied any impropriety. Time will tell whether TPG-Axon’s bid to unseat Ward and the SandRidge board will succeed.

Final Foolish Thoughts

There’s money to be made in US energy production. Ask those who own Enterprise or Phillips. But it’s not failsafe, as investors in Chesapeake or SandRidge will attest.

Ideally, a combination of due diligence on the part of the investor and transparency on the part of the company will lead to good investment decisions. Certainly, a track record, growing dividends and prudent business decisions indicate a good company to invest in. Enterprise and Phillips 66 (NYSE:PSX) fit that bill.

Does SandRidge represent a turnaround story? In my opinion, no — or at least, not yet. Given the poor track record of the company’s earnings, and the questionable wisdom, if not conflict of interest, of Mississippian Lime exploration, SandRidge looks more like a poorly managed company than a good investment. Until Ward goes, there are better companies around.

The article A proven winner, a likely winner and a dud originally appeared on Fool.com.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.