Rivals or similar companies tend to report earnings around the same time, making for interesting comparative opportunities. Two of my favorite companies report earnings a day apart, and they just so happen to operate in the same industry. I’m talking about The Home Depot, Inc. (NYSE:HD) and Lowe’s Companies, Inc. (NYSE:LOW), the two largest home-improvement retailers. Before these companies announce how they did in fiscal year 2013 (their fiscal years both end on January 31st), I’d like to take a look to see which looks like the more attractive investment right now.

First, here is a little bit about both companies. Home Depot is the largest home improvement retailer in the world with 2,252 stores and Lowe’s is second, with 1,712 stores of its own.

![]()

I would like to evaluate these companies in three areas, and then we’ll attempt to determine which one should be bought right now.

Past and Future Growth

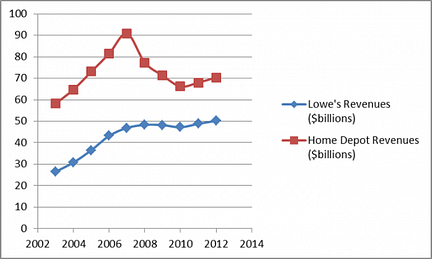

As far as past growth goes, both companies have done an impressive job of growing over the past decade.

So, I have a couple of observations here. Not only did Lowe’s grow more overall during this time period (89% vs. 21%), but it appears Lowe’s was more resistant to the 2008-2010 recession than Home Depot was.

As far as future growth goes, Lowe’s is projected to report that it earned $1.72 per share for FY 2013, which is expected to increase to $2.08 and $2.52 over the next two years, for an average forward growth rate of 21% (wow). Home Depot is expected to report current year earnings of $3.04 per share, which are expected to increase to $3.48 and $3.99 over the next two years, for 14.6% average growth. Not too shabby, but I have to give Lowe’s the advantage in this category.

Shareholder-Friendly Management (dividends, buybacks)

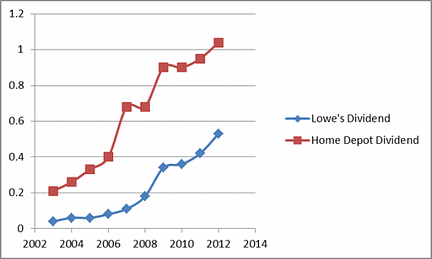

Now let’s see who has done the better job of creating value for its shareholders, and the two best ways to measure this are by looking at dividends and buybacks. Lowe’s pays out a 1.66% dividend yield and has increased this in 9 out of the past 10 years. Home Depot yields a slightly higher 1.72%, which it has raised in 8 of the past 10 years. So far, they are pretty even.

As far as the repurchase of shares goes, over the past five years, Lowe’s has reduced the number of outstanding shares by 23.6%, as opposed to just 10.6% for Home Depot. So, this category too goes to Lowe’s

Current Valuation Analysis

Now, my regular readers know that my rule of thumb for valuation is simple: Double the forward growth rate. The P/E ratio of the stock should be significantly lower than that number.

Lowe’s trades at 23 times earnings with 21% forward growth, which means it trades at just 54.8% of twice the growth rate. Home Depot trades at an even loftier P/E ratio of 24, and I can’t really figure out why, with 14.6% average growth. While doubling the growth rate (29.2) certainly means it is decently valued by my little rule, I don’t see why the company trades at such a premium to its peer.

Conclusion

In the three categories examined here, Lowe’s is by far the more attractive company for a long-term investment. Unless Home Depot has a fantastic quarter, and/or Lowe’s has a particularly terrible one, I think that Lowe’s is clearly the better bet of these two industry leaders.

The article Which Home Improvement Giant Should You Choose? originally appeared on Fool.com and is written by Matthew Frankel.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.