Here’s the list of key investor issues:

Continued Margin Compression

Declining Comparable Earnings

A Perceived Innovation Vacuum

Too Much Balance Sheet Cash

Let’s briefly examine each one.

Margin compression

Gross margin represents net sales less the direct costs associated with producing the goods and services sold by a company. It is commonly expressed as a percentage. Historically, Apple Inc. (NASDAQ:AAPL) has enjoyed very high gross margins.

Here’s a five-year chart showing Apple’s quarterly gross margins:

courtesy of ycharts.com

Since the 47.4% peak captured in the quarter ending March 2012, margins have fallen the last four quarters. Management has forecast a another drop in gross margin to 36.5% in the quarter ending June 30.

Until gross margin (GM) stabilizes, the Street will conclude that underlying operating and net margins will likewise remain under pressure, thereby eroding earnings.

The problem may be fixed in two ways. First, product costs and mix could change thereby rekindling higher margins. Alternatively, higher revenues can overshadow declining GM. The math for this second fix is somewhat challenging, but plausible.

Let me illustrate. Last quarter, Apple Inc. (NASDAQ:AAPL) recorded a dollar-denominated gross margin of $16.35 billion on net sales of $43.6 billion (or a 37.5% margin ratio). A two-and-a-half point GM ratio increase, equating to a 40% margin would have generated $17.44 billion. In order for Apple Inc. (NASDAQ:AAPL) to generate equivalent 40% gross margin dollars, it would have been necessary for the company to net $46.5 billion in sales, an increase of $1.09 billion; or a 6.7% uplift from the actual. Actual sales were up 11% quarter over quarter (QoQ).

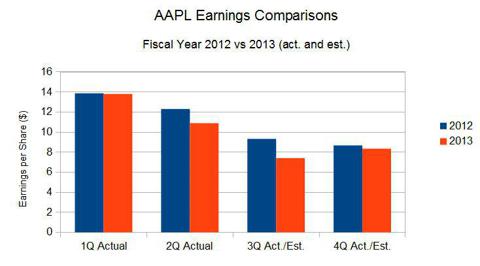

Declining comparable earnings

A close cousin to declining margins are Apple Inc. (NASDAQ:AAPL)’s declining year-over-year earnings per share. I put together the following graph:

(estimates via TDAmeritrade consolidated forecasts)

Indeed, comparable EPS figures have declined the last two quarters, and analysts project the decline to last at least another two. Furthermore, upon the April 23 fiscal year 2013 second quarter earnings conference call, Apple’s management set expectations that the QoQ third quarter decline will accelerate.

Until earnings stabilize and the Street begins to anticipate earnings growth, the stock price is unlikely to step up.

Perceived innovation vacuum

Under the late Steve Jobs, Apple Inc. (NASDAQ:AAPL) rode a wave of customer and investor enthusiasm over his innovative capabilities and demand for perfection. Since his departure, the company’s ability to innovate has been called to question. Whether this is true or false is irrelevant.

In the investment world, sentiment and perception become reality.

I contend that new CEO Tim Cook is being called out by Wall Street. He’s being asked to amplify his role from an outstanding operations man into a visionary leader. I am not yet questioning his ability to do so. However, the results have not materialized.

Apple management must bridge the perceived innovation gap. Otherwise, it is reasonable to believe that Street expectations will remain soft. Soft Wall Street expectations translate into soft share prices until such time that the company can demonstrate the lowered expectations have been overdone to the downside.

Too much balance sheet Cash

Previously, Apple Inc. (NASDAQ:AAPL)’s unusually high balance sheet cash and liquid investments were considered an asset. Steve Jobs’ ferocious defense of the cash hoard was accepted due to his aura and rapidly rising stock price. Sure, some investors murmured about the billions bottled up on the balance sheet, but they largely kept their mouths shut.

The plummet in stock price and weakening associated metrics have changed all of that.

Management and the board of directors got the message. They announced some relief in April: a 15% dividend increase and a 32-month, $60 billion stock buyback program.

My view is that these items created a floor under the stock price. They were not silver bullets.

The dividend increase resulted in an approximate 3% yield on the underlying stock price: admirable, respectable, but not earth-shaking. There are many 3% yielding stocks that have better near-term earnings growth potential.

The buyback plan is somewhat impressive if for no other reason than its sheer magnitude. However, it’s spread out until the end of 2015. This diluted its effect.

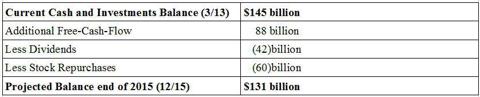

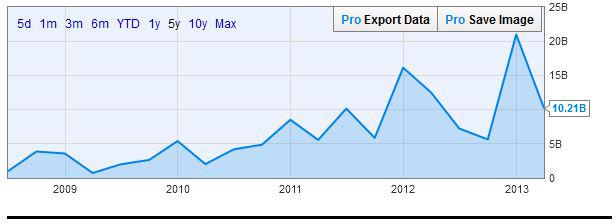

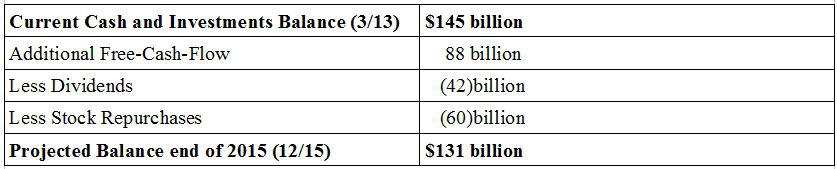

Let’s assume that Apple generates an average of $8 billion in Free-Cash-Flow (FCF) per quarter, or $88 billion through the 11 quarters of the 2013 to 2015 period. FCF is defined as operating cash flow less capital expenditures. This is an important metric since it represents what cash the company has left over after all expenses and routine capital requirements have been made.

Here’s a chart of Apple Inc. (NASDAQ:AAPL)’s FCF over the past five years, outlining why I suggest this figure is defensible:

courtesy of ycharts.com

Now let’s premise that the 2014 and 2015 annual dividend is raised by 10% each year. Therefore, the total cash dividends paid will be approximately $42 billion between now and the end of 2015.

Here’s the all-in math:

Apple Balance Sheet Cash / Investments 2013 – 2015

While a step in the right direction, Apple management appears intent on retaining the bulk of the current cash hoard. The company compounded this perception by recently borrowing $17 billion in debt with the stated intent of using much of it for future dividend payments. Indeed, it should be noted that while Apple holds a majority of its cash overseas, over $42.4 billion is here in the U.S.; equivalent to pay all the projected dividends through 2015. Of course, more than a third of Apple Inc. (NASDAQ:AAPL)’s ongoing operating cash is expected to be generated here, too.

Indeed, Apple investors understand there are tax consequences if the overseas fund are repatriated. Nonetheless, Apple management needs to explain what they plan to do with it. And while the stock buyback will retire up to 4 or 5% a year of shares outstanding, additional shares will be issued to management and employees in the form of options and restricted stock, thereby diluting the effort.

While corporate leadership has begun to address the issue of excess cash, I do not believe it’s a closed case.

In addition, Apple management could do itself a favor by taking a page from the Intel Corporation (NASDAQ:INTC) playbook: invest the cash in a way that provides a better return. Apple FY2012 10-K filings indicated an annual return on cash and investments of only 1.03 percent.

On the other hand, Intel 2012 10-K filings provide detail showing cash and marketable investments have generated three-year, average annualized capital and income returns of $332 million, or approximately 2%; plus marketable investments recorded a 2012 gross unrealized gain of over $1 billion, or 7%. Intel Corporation (NASDAQ:INTC) outlines a breakdown of cash equivalents, fixed income, and marketable securities within the SEC filings. Management line-items “gains and losses on equity investments,” as well as “interest” on their income statement. Apple management rolls it all up into “other income (expense).

The bottom line

Apple management faces four key investor issues: margin compression, declining comparable earnings, an innovation vacuum, and excessive balance sheet cash / investments. These issues underpin underlying business performance. I suggest that until these items show improvement, the share price will remain range-bound.

The article What Apple Management Must Do To Levitate Your Shares originally appeared on Fool.com and is written by Raymond Merola.

Author is long AAPL and INTC. Raymond is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.

{kind=link}

{kind=link}

{kind=link}

{kind=link}