A SWOT analysis is a look at a company’s strengths, weaknesses, opportunities, and threats, and is a tremendous way to gain a detailed and thorough perspective on a company and its future. As 2013 begins, I would like to focus on a diversified financial institution: Wells Fargo & Company (NYSE:WFC).

The Business:

Warren Buffett once said, “Never invest in a business you can’t understand.” This not only allows the investor to purchase a company with conviction, but also allows them to spot trends that may be missed by unfamiliar eyes. With this in mind, investors in any company should fully understand the business model of the company. Wells Fargo operates in three main segments: community banking, wholesale banking, and wealth, brokerage, and retirement. Based on market capitalization, the company is valued at $185.16 billion. Because of the incredible strength of the company’s business model and pricing power, the company possesses a profit margin of 20.97%.

1). Institutional Vote of Confidence: 74.72% of shares outstanding are held by institutional investors, displaying the confidence some of the largest investors in the world have in the company and its future

2). Basement Valuation: Currently, Wells Fargo carries a price to earnings ratio of 10.45, a price to book ratio of 1.28, and a price to sales ratio of 2.15, all of which indicate a company trading with a basement valuation

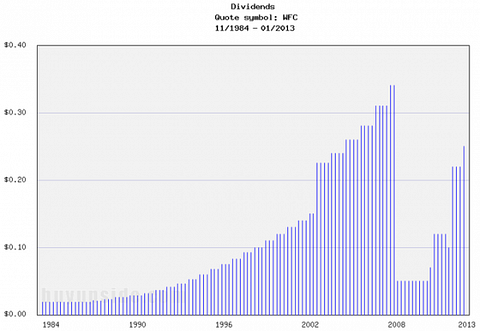

3). Dividend: Presently, the company pays out quarterly dividends of $0.25, which annualized puts the dividend as yielding 2.84%

4). Profit Margin Expansion: Wells Fargo’s profit margin has expanded from 14.64% in 2008 to 20.97% currently, and this trend of profit margin expansion is a major strength

5). Broad Diversity and Established Nature: Wells Fargo operates in several major industries, including mortgages, loans, securities and trading, asset management and brokerage, insurance, and others, and with the company’s established and diversified nature comes an increased level of predictability and security for investors

6). Steady Total Asset Growth: The company’s total assets have grown from $1.31 trillion in 2009 to $1.42 billion currently, and this trend of steady asset growth is a major strength

7). Historic Revenue Growth: Since 2000, Wells Fargo’s revenue has increased from $25 billion to $91.25 billion currently, representing year over year annual growth of 11.39%, a trend that is anticipated to continue, though slow down in the future, with projections placing 2017 revenue at $99.45 billion

Weaknesses:

1). Net Debt: Despite possessing $16.99 billion in cash and cash equivalents on their balance sheets, the company’s debt load of $127.38 billion results in a substantial net debt of $110.39 billion

2). Volatility: At the moment, the company possesses a beta ratio of 1.38, representing a company trading with slightly more volatility than the overall market

3). Negative Free Cash Flow: According to the company’s most recent quarterly report, Wells Fargo holds a negative free cash flow position of $50.19 billion, a major weakness in the company

Opportunities:

1). Dividend Growth: Since implementing their dividend program in 1939, Wells Fargo has consistently raised their dividend payouts and should continue to do so well into the future

2). Growth in Value of Mortgage Loans: 24.77% of overall business is concentrated in the mortgages segment, of which is primarily fueled by the value of mortgage loans the company currently backs, which has grown from $150 billion in 2008 to $322 billion currently, primarily due by the merger with Wachovia and further growth in the value of mortgage loans is projected, with projections placing 2019 mortgages at $419 billion