![]()

Back on track

The company really messed up during the credit bubble. American International Group Inc (NYSE:AIG) was insuring banks and other investors against potential losses in subprime real estate assets, which was probably the worst kind of bet it could possibly make at the time.

When the crisis exploded, American International Group Inc (NYSE:AIG) found itself in a position of insolvency, so the company was declared “too big to fail” and received a $182 billion bailout from the federal government in order to backstop a crisis that was producing ripple effects all over the global financial system.

But that´s ancient history, and under the leadership of Robert Benmosche the company has gone through a long and painful restructuring process, including big reductions in its workforce and the sale of valuable assets like its Asian life insurance business. Perhaps more important, AIG has now liquidated 93% of the complex derivatives it had in its balance sheet at the end of 2008.

American International Group Inc (NYSE:AIG) has completely repaid the government, so the company is free to focus its energy and financial resources in reigniting growth and profitability, and it seems to be moving in the right direction judging by financial results.

The company reported earnings figures well above analysts’ expectations for the last quarter: overall insurance operating income was up 28% from the same quarter last year, and book value per share, excluding accumulated other comprehensive income (AOCI), increased by 12% in comparison to the first quarter of 2012.

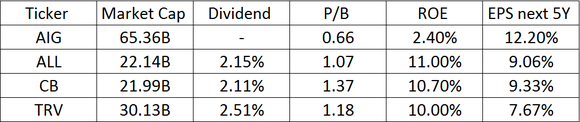

Attractive valuation

In spite of this noteworthy recovery, American International Group Inc (NYSE:AIG) is trading well below average valuation levels for the industry. When comparing price to book value ratios for AIG versus other insurance companies like The Allstate Corporation (NYSE:ALL), The Chubb Corporation (NYSE:CB) and Travelers Companies Inc (NYSE:TRV), the company is looking deeply undervalued. AIG has a price to book value ratio of 0.66, while is competitors are in the range of 1.07 to 1.37.

One possible explanation for this undervaluation may be that investors are not yet giving the company the credit it deserves for its improved financial position; however, we still need to consider that AIG has much lower profitability than its competitors.

When looking at return on equity – ROE – ratios, AIG´s profitability is clearly below that of its peers: it’s in the area of 2.4% versus levels in the range of 10% to 11% for other companies in the business. The higher the ROE, the more profitable each dollar of equity, hence the price to book value ratio should be higher. With lower profitability, American International Group Inc (NYSE:AIG) may actually deserve a lower price to book value ratio.

But here comes good news for AIG investors: management has stated its goal of reaching a 10% ROE in the middle term, and they seem to be making progress in that area. If – or when – AIG gets its profitability rations in line with that of its competitors, investors should enjoy some big fat returns as the company´s valuation multiples expand to average industry levels.

Improving industry conditions

AIG benefited from improving pricing conditions in the last quarter, and other companies are confirming the trend towards better times for insurance underwriters in the middle term.

The Allstate Corporation (NYSE:ALL) managed to report better than expected earnings for the last quarter in spite of increased losses from catastrophic events, higher premiums and an improved combined ratio – the tally of losses and costs per $100 of written premiums – were the main reasons for the better than expected results. All of the company´s insurance arms reported higher premiums, with property and casualty premiums growing 2.5% year over year.

The same goes for Travelers Companies Inc (NYSE:TRV); the company has faced two seriously damaging hurricanes in the last two years, yet increased premiums have produced earnings well above analyst´s expectations for the last quarter. The company reported an increase of 11% in both net and operating income for the quarter, and management attributed this performance to “continued improvement in underlying underwriting margins in all segments.”

The Chubb Corporation (NYSE:CB) did even better than its competitors. Since it’s not very exposed to Property Casualty, it managed to report lower catastrophe losses for the last quarter. But that didn´t stop Chubb from rising insurance premiums, so earnings were strong both from the point of view of income and losses. The Chubb Corporation (NYSE:CB) reported a big increase of 36% in earnings per share for the March quarter.

After years of lackluster industry returns due to falling premiums, high catastrophe losses and low returns on fixed income investments due to rock bottom interest rates, it looks like insurers are finally starting to raise their premiums and increase profitability. This should provide a welcome tailwind for American International Group Inc (NYSE:AIG) on its way to higher profitability and accelerating growth.

Bottom Line

AIG is leaving its problems behind, and the company is now ready to focus on increasing profitability and expanding its business. Signs of progress are quite clear at this stage, and improving industry conditions bode well in terms of future possibilities. In spite of that, the stock is trading at bargain valuation levels, so this insurance powerhouse looks like a compelling opportunity.

The article Three Reasons to Buy AIG originally appeared on Fool.com and is written by Andrés Cardenal.

Andrés Cardenal owns shares of American International Group (NYSE:AIG).The Motley Fool recommends American International Group. The Motley Fool owns shares of American International Group and has the following options: Long Jan 2014 $25 Calls on American International Group. Andrés is a member of The Motley Fool Blog Network — entries represent the personal opinion of the blogger and are not formally edited.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.