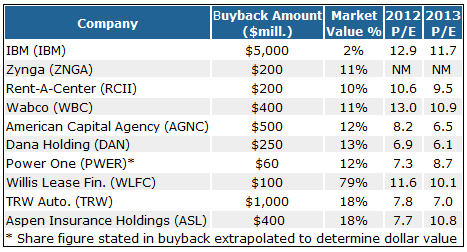

That’s the logic behind International Business Machines Corp. (NYSE:IBM) just-announced plan to buy back $5 billion in company stock. In IBM’s case, the choice was an easy one. With more than $100 billion in annual sales, IBM is so large that acquisitions won’t really move the needle. In addition, much of IBM’s sales base is tied to long-term contracts, which means that a tougher economy won’t lead to a sudden sales plunge — and an ensuing cash shortfall.

For other companies, a hefty buyback isn’t so cut and dry. Companies need to be sure they don’t blow the cash on buybacks, in case they need the cash when tougher days arrive. That was the tough lesson learned by telecom firm Nokia Corporation (NYSE:NOK) between 2004 and 2009 when it bought back 900 millionshares (or more than 20% of the total share count). That buyback continued even as shares approached $40 in late 2007. With shares now below $3, management wishes it could have that money back.

Indeed companies are increasingly tempted to take advantage of share price weakness by buying back stock, but only if two conditions are met. First, the current cash balance and cash flow must be so robust that there will be plenty of money left over even after the buyback is completed. Second, management must remain convinced the economy won’t fall into an abyss in the quarters and years ahead.

As the Nokia poor decision has shown, buybacks can be backfire. That’s why it’s best to focus on companies that are buying back reasonably-priced shares. IBM, trading at 11.7 times projected 2013 profits, is not necessarily a bargain, nor is the size of the buyback (just 2% of shares outstanding) all that impressive. Though there dozens of other firms have announced or extended buyback plans since the start of October, you should be focusing on the group below. Each firm will be able to reduce the share count by more than 10% (assuming little fresh dilution from stock options), and each sports a reasonable 2013 price-to-earnings (P/E) multiple.

Looks can be deceiving when deciphering these numbers. For example, Willis Lease Finance Corporation (NASDAQ:WLFC), which leases and services aircraft engines, intends to buy back $100 million in stock during the next five years. A lot can happen in that time. Still, with shares trading at just 64% of tangiblebook value, the buyback looks like a wise move.

It’s noteworthy that a pair of auto parts suppliers, Dana Holding Corporation (NYSE:DAN) and TRW Automotive Holdings Corp. (NYSE:TRW) are buying back a lot of stock. Each one sports a very low P/E multiple to begin with, and the buybacks should only help the cause. Goldman Sachs, for example, says TRW’s share count will shrink up to 15% by 2014 (after accounting for stock option dilution), and sees earnings approaching $8 a share by then. So the forward multiple drops below six, by that math, leading Goldman to pencil in a $61 price target, or roughly 30% ahead of current levels.

Yet it’s Dana holdings, which makes transmissions and other auto components, that looks like the best bargain, perhaps in the entire auto supplier industry. Against a market value of around $1.9 billion, Dana is expected to generate nearly $800 million in EBITDA this year. The real cash metric — free cash flow — is even more impressive. Thanks to a wind down in capital spending, free cash flow is expected to rise from $100 million this year to $345 million in 2013 and more than $400 million in 2014, according to analysts at Merrill Lynch. This means the 2014 free cash flow yield is above 20%. In that light, a stock buyback makes tremendous sense.

Risks to Consider: If the market rebounds and pushes these stocks back up in price, then their stock buyback programs will have less of an effect on the share count.

Action to Take –> Stock buybacks not only help shrink the share count, but they also provide downside support when the market is falling, as company-made purchases offset outside shareholder sales. If these stocks don’t hold up as expected, then stock buyback will just be that much more effective in terms of reducing the share count.