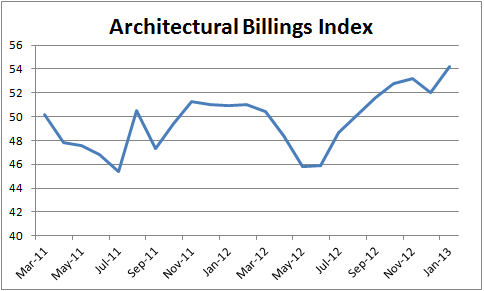

As for the kicker from new housing starts the indicators are that this will indeed kick in for Whirlpool Corporation (NYSE:WHR) in late 2013. Here is the latest Architectural Billings Index and within this index the residential indicator is the highest.

Broadly speaking the industry has been reporting positive news lately. The Home Depot, Inc. (NYSE:HD) has recently reported broad based strength across its categories and importantly, its more discretionary based items are seeing sequential strength. It’s worth noting that Whirlpool distributes products at both The Home Depot, Inc. (NYSE:HD) and Lowe’s and if they are seeing strength then so will Whirlpool. Furthermore much of the background data in this article equally applies to their end demand too.

As for its chief rival in the US, General Electric Company (NYSE:GE) recently reported a solid set of results and expressed positive commentary on North America. Although its home and business based profits don’t make up more than 13% of GE’s total so it less exposed to the sector than Whirlpool Corporation (NYSE:WHR) or Electrolux. Of course this means it can cross subsidize its home goods sales and engage in the kinds of pricing promotions and discounts that hit the industry in 2010-11. On the other hand with conditions improving in the US there may be some opportunity to for price gains across the industry.

And finally the segmental breakdown of profits reveals the importance of Latin America (mainly Brazil) to the company’ profitability.

Indeed for 2013, the company is forecasting 3-5% growth in Latin America and Asia with 2-3% in North America and EMEA as being flat.

Where Next For Whirlpool?

A quick review of the guidance for 2013 shows Whirpool predicting $600-650 million in free cash flow with $950-1bn in ‘ongoing business cash flow’. The latter is adjusted for tax credits, pension contributions and restructurings. Even taking the lower number’s midpoint of $625m, it is still forecast to generate around 6% if its enterprise value in free cash flow this year. Moreover its earnings guidance of $9.25-9.75 of ongoing diluted EPS implies a forward PE of 12.1 at the midpoint.

In conclusion, the stock doesn’t look expensive and provided the US housing market is doing okay I think it is worth picking up. As for Brazil, a large part of its prospects depend on servicing China with raw materials so this makes Whirlpool the kind of stock to avoid should China disappoint with growth. For now things look okay.

The article The Real Earnings Potential of This Stock originally appeared on Fool.com and is written by Lee Samaha.

Copyright © 1995 – 2013 The Motley Fool, LLC. All rights reserved. The Motley Fool has a disclosure policy.